|

시장보고서

상품코드

1998774

펩타이드 항생제 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Peptide Antibiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

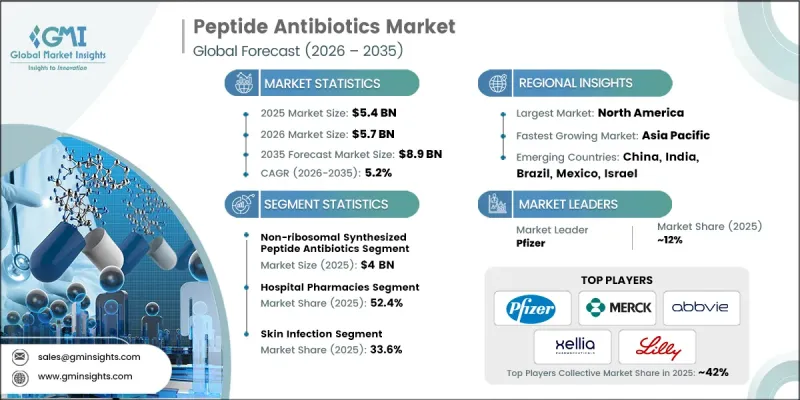

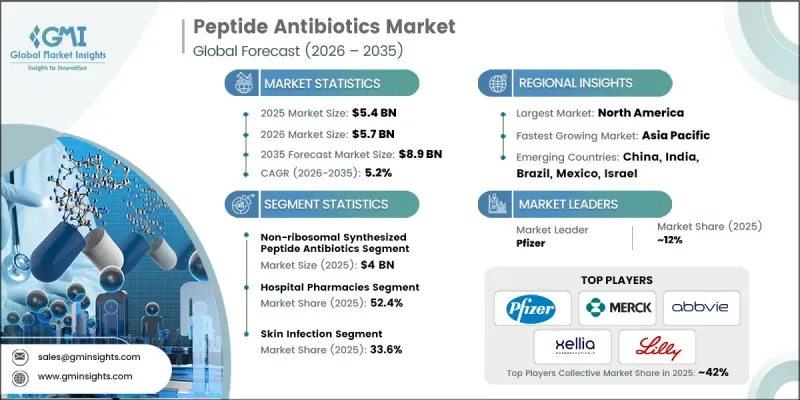

세계의 펩타이드 항생제 시장은 2025년에 54억 달러 규모로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.2%로 성장하여 89억 달러에 달할 것으로 예측됩니다.

펩타이드 항생제 산업 전반의 성장은 약제 내성에 대한 우려 증가와 약제 내성 감염을 퇴치할 수 있는 새로운 치료법의 시급한 필요성에 의해 크게 영향을 받고 있습니다. 공공 기관과 민간 조직의 자금 지원은 이 분야의 혁신을 가속화하는 데 중요한 역할을 하고 있습니다. 첨단 항균 솔루션 발굴을 위한 투자 프로그램은 새로운 펩타이드 기반 치료법 개발을 촉진하고 있습니다. 동시에 펩타이드 합성 기술과 최신 약물 전달 플랫폼의 급속한 발전으로 펩타이드 항생제 개발 파이프라인이 확대되고 있습니다. 이러한 발전으로 연구자들은 새로운 내성 문제를 해결할 수 있는 보다 효과적인 항균제를 설계할 수 있게 되었습니다. 의료진들이 확실한 결과를 가져다주는 표적 치료제를 계속 찾고 있는 가운데, 펩타이드 항생제는 제약 연구 개발 및 임상 치료 프로그램에서 점점 더 많은 관심을 받고 있으며, 이는 펩타이드 항생제 시장의 장기적인 성장 전망을 더욱 확고히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 54억 달러 |

| 예측액 | 89억 달러 |

| CAGR | 5.2% |

생명공학 및 제제 기술의 발전으로 펩타이드계 항생제의 안정성, 생체이용률 및 치료 효율이 향상되어 치료 효과가 크게 향상되었습니다. 표적 의료에 대한 관심이 높아지면서 펩타이드 항균 치료제의 개발이 가속화되고 있습니다. 이러한 화합물은 내성균주를 공격하도록 설계할 수 있는 반면, 원치 않는 전신에 미치는 영향을 최소화할 수 있기 때문입니다. 일반적으로 항균 펩타이드(항균 펩타이드)라고 불리는 펩타이드계 항생제는 미생물의 생존 과정을 억제하는 능력을 가진 짧은 아미노산 사슬로 구성되어 있습니다. 이 분자들은 미생물의 필수적인 세포 메커니즘과 구조적 구성요소를 간섭하여 미생물의 증식을 억제합니다. 이러한 펩타이드는 생물체 내에서 자연적으로 생성되는 경우도 있고, 실험실에서 개발 기법을 통해 합성되는 경우도 있습니다.

비리보솜 합성 펩타이드계 항생제 부문은 2025년 40억 달러 시장 규모를 기록했습니다. 이 부문은 광범위한 항균 활성과 효소 분해에 대한 강한 내성으로 인해 선도적인 위치를 유지하고 있습니다. 비리보솜성 펩타이드계 항생제는 고도의 구조적 다양성과 일반적으로 사용되지 않는 아미노산 성분의 통합을 가능하게 하는 특수한 효소 복합체를 통해 생성됩니다. 이러한 구조적 유연성은 이러한 항생제의 치료 효과와 내구성을 향상시켜 다제내성균주에 의한 감염 치료에 특히 유용하게 사용되고 있습니다.

2025년 피부감염증 부문은 33.6%의 점유율을 차지했습니다. 펩타이드 항생제 산업에서 이 부문의 강력한 존재감은 세균성 피부 질환의 발생률 증가와 효과적인 치료법에 대한 수요 증가와 관련이 있습니다. 또한, 의료 시술 후 치유가 어려운 상처 및 감염 관련 합병증 발생률 증가도 펩타이드계 항생제에 대한 수요 증가에 기여하고 있습니다. 이러한 약물은 광범위한 전신 부작용의 위험을 줄이면서 표적화된 항균 작용을 발휘하기 때문에 종종 선택되는 경우가 많습니다.

2025년 북미 펩타이드 항생제 시장은 40.5%의 점유율을 차지했습니다. 이 지역이 세계 펩타이드 항생제 산업에서 선도적인 위치를 차지하고 있는 배경에는 높은 수준의 의약품 연구 능력, 엄격한 규제 감독, 그리고 막대한 의료비 지출이 있습니다. 기존의 생명공학 및 제약 부문은 항생제 개발의 혁신을 더욱 촉진하고 있습니다. 또한, 새로운 항균 치료법의 발견을 촉진하기 위해 고안된 정부 지원 연구 자금 프로그램과 정책 이니셔티브는 지역 전체에서 개발 및 상업화 활동을 가속화하는 데 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035

제6장 시장 추산 및 예측 : 적응별, 2022-2035

제7장 시장 추산 및 예측 : 투여 경로별, 2022-2035

제8장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.23The Global Peptide Antibiotics Market generated USD 5.4 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 8.9 billion by 2035.

Growth across the peptide antibiotic industry is strongly influenced by increasing concerns regarding antimicrobial resistance and the urgent need for new treatment approaches capable of combating drug-resistant infections. Financial support from public institutions as well as independent organizations is playing a significant role in accelerating innovation within this field. Investment programs aimed at discovering advanced antimicrobial solutions are encouraging the development of new peptide-based therapeutic options. At the same time, rapid progress in peptide synthesis technologies and modern drug delivery platforms is expanding the development pipeline for peptide antibiotics. These advancements are enabling researchers to design more effective antimicrobial agents that can address emerging resistance challenges. As healthcare providers continue seeking targeted therapies capable of delivering reliable outcomes, peptide antibiotics are gaining greater attention within pharmaceutical research and clinical treatment programs, strengthening the long-term growth outlook for the peptide antibiotics market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.4 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 5.2% |

Technological progress in bioengineering and pharmaceutical formulation has significantly enhanced the therapeutic performance of peptide antibiotics by improving their stability, bioavailability, and treatment efficiency. The increasing focus on targeted medical treatments is also encouraging the development of peptide-based antimicrobial therapies, as these compounds can be engineered to attack resistant microbial strains while minimizing unwanted systemic effects. Peptide antibiotics, commonly referred to as antimicrobial peptides, consist of short chains of amino acids capable of disrupting microbial survival processes. These molecules inhibit microbial growth by interfering with essential cellular mechanisms and structural components. Such peptides may originate naturally within biological systems or be produced synthetically through laboratory-based development methods.

The non-ribosomal synthesized peptide antibiotics segment generated USD 4 billion in 2025. This segment maintains a leading position because of its broad antimicrobial activity and strong resistance to enzymatic degradation. Non-ribosomal peptide antibiotics are generated through specialized enzyme complexes that allow extensive structural diversity and the incorporation of uncommon amino acid components. This structural flexibility improves the therapeutic strength and durability of these antibiotics, making them particularly valuable for addressing infections caused by multidrug-resistant bacterial strains.

The skin infection segment held 33.6% share in 2025. The segment's strong presence within the peptide antibiotics industry is associated with the growing occurrence of bacterial skin-related conditions and the rising need for effective therapeutic solutions. The increasing incidence of persistent wounds and infection-related complications following medical procedures has also contributed to higher demand for peptide-based antibiotics. These medications are often selected because they provide targeted antimicrobial activity while reducing the likelihood of broader systemic side effects.

North America Peptide Antibiotics Market accounted for 40.5% share in 2025. The region's leadership within the global peptide antibiotics industry is supported by advanced pharmaceutical research capabilities, strong regulatory oversight, and significant healthcare spending. A well-established biotechnology and pharmaceutical sector further encourages innovation in antibiotic drug development. In addition, government-backed research funding programs and policy initiatives designed to promote the discovery of new antimicrobial therapies are helping accelerate development and commercialization activities across the region.

Key companies operating in the Global Peptide Antibiotics Market include Pfizer, Merck, Sanofi, GSK plc, Eli Lilly and Company, AbbVie, Teva Pharmaceuticals, Sandoz, The Menarini Group, ANI Pharmaceuticals, Cumberland Pharmaceuticals, Melinta Therapeutics, Monarch Pharmachem, JHP Pharmaceuticals, NPS Pharmaceuticals, and Xellia Pharmaceuticals. Companies in the Global Peptide Antibiotics Market are adopting several strategic approaches to strengthen their market position and support long-term growth. Major pharmaceutical manufacturers are prioritizing investment in research and development to create advanced antimicrobial compounds capable of addressing drug-resistant infections. Strategic collaborations with biotechnology firms, academic institutions, and research organizations are also helping accelerate drug discovery and clinical development programs. Many companies are expanding their product pipelines by focusing on innovative peptide synthesis technologies and advanced drug delivery systems. In addition, organizations are pursuing regulatory approvals across multiple regions to broaden global market access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Route of administration trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of multi-drug resistant (MDR) bacteria

- 3.2.1.2 Increasing incidence of acute and chronic infectious diseases

- 3.2.1.3 Technological advancements in peptide synthesis

- 3.2.1.4 Rising investments in next-generation antimicrobial R&D

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Limited oral bioavailability

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of peptide-engineered drug delivery systems

- 3.2.3.2 Growing demand for novel antimicrobial classes for AMR prevention

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.5 Pipeline analysis

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Impact of AI and generative AI on the market

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Ribosomal synthesized peptide antibiotics

- 5.3 Non-ribosomal synthesized peptide antibiotics

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Skin infection

- 6.3 Hospital-acquired bacterial pneumonia and ventilator-associated bacterial pneumonia (HABP/VABP)

- 6.4 Blood stream infections

- 6.5 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Injectable

- 7.3 Oral

- 7.4 Topical

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 ANI Pharmaceuticals

- 10.3 Cumberland Pharmaceuticals

- 10.4 Eli Lilly and Company

- 10.5 GSK plc

- 10.6 JHP Pharmaceuticals

- 10.7 Merck

- 10.8 Monarch Pharmachem

- 10.9 Melinta Therapeutics

- 10.10 NPS Pharmaceuticals

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sandoz

- 10.14 Teva Pharmaceuticals

- 10.15 The Menarini Group

- 10.16 Xellia Pharmaceutical