|

시장보고서

상품코드

1998780

수의용 스텐트 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Veterinary Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

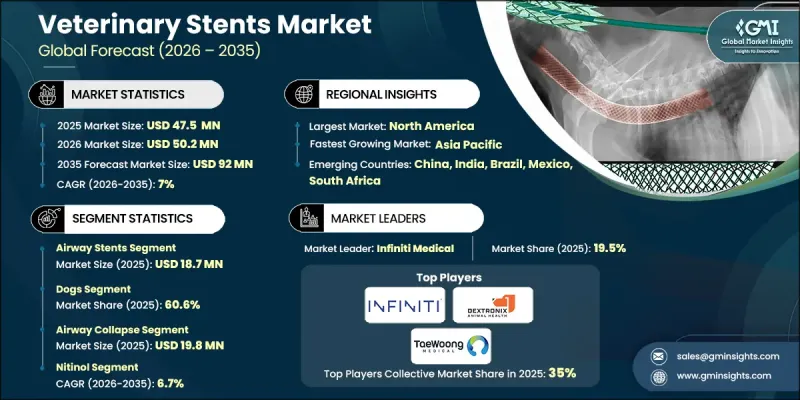

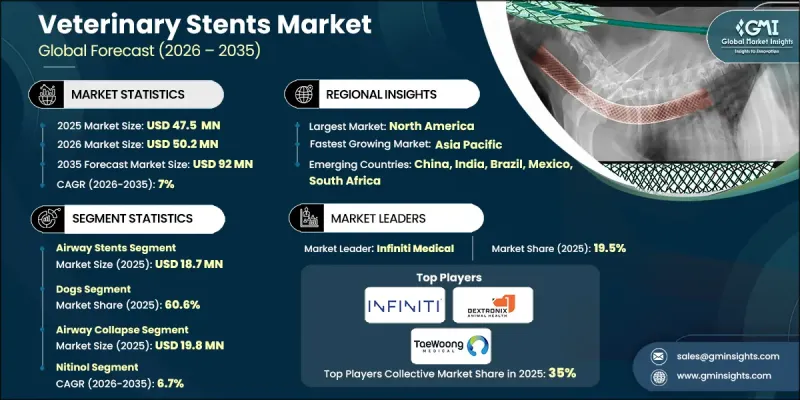

세계의 수의용 스텐트 시장은 2025년에 4,750만 달러로 평가되었고, CAGR 7%로 성장하여 2035년까지 9,200만 달러에 달할 것으로 예측됩니다.

수의용 스텐트 시장의 성장은 동물의 건강 개선과 수의학 분야의 치료 기준 향상에 대한 관심이 높아짐에 따라 크게 영향을 받고 있습니다. 전 세계적으로 반려동물 사육두수가 지속적으로 증가함에 따라 수의사와 반려동물 보호자들은 반려동물의 삶의 질을 향상시킬 수 있는 효과적인 의료적 개입을 더욱 중요하게 여기고 있습니다. 수의용 스텐트는 생명 유지에 필수적인 체내 통로에 구조적 협착이나 막힘이 발생한 동물에게 중요한 치료 옵션으로 점점 더 많이 인식되고 있습니다. 동시에 급속한 기술 발전으로 인해 이러한 장치의 성능과 신뢰성이 크게 향상되었습니다. 저침습적 수의학적 시술의 개발과 더불어 스텐트 설계의 개선과 첨단 생체 재료의 도입으로 이식 시술의 성공률이 향상되었습니다. 또한, 영상진단 기술 및 시술 기술의 발전으로 수의사들은 보다 정확하고 효율적인 치료를 제공할 수 있게 되었습니다. 이러한 발전은 임상 결과의 개선, 동물의 회복 가속화, 합병증 발생률 감소에 기여하고 있습니다. 그 결과, 수의학 스텐트는 수의학 전문가들 사이에서 널리 받아들여지고 있으며, 동시에 첨단 치료법을 원하는 반려동물 보호자들의 신뢰도도 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 4,750만 달러 |

| 예측액 | 9,200만 달러 |

| CAGR | 7% |

수의용 스텐트는 질병, 외상 또는 발육부진으로 인해 특정 체내 통로가 막히거나 좁아진 동물을 치료하기 위해 고안된 특수 임플란트 역할을 합니다. 이러한 원통형 장치는 일반적으로 내구성이 강한 금속 합금 또는 고분자 재료를 사용하여 제조되며, 관형 해부학적 구조에 삽입되어 적절한 통로를 유지하고 정상적인 생리 기능을 회복시킵니다. 수의용 스텐트는 환부에 구조적 지지대를 제공함으로써 설치 위치에 따라 공기 흐름, 순환 또는 체액 이동을 개선하는 데 도움이 됩니다.

기도 스텐트 부문은 2025년 1,870만 달러 시장 규모를 기록했습니다. 이 부문의 성장은 주로 호흡기 계통에서 장기적인 구조적 지원이 필요한 반려동물의 호흡기 관련 질환 발생률 증가와 관련이 있습니다. 이러한 질환은 심각한 호흡 장애를 유발할 수 있으며, 적절한 기류를 회복하기 위해 즉각적인 의료적 개입이 필요합니다. 수의사와 반려동물 보호자들 사이에서 저침습적 치료법에 대한 선호도가 높아진 것도 기도 스텐트 사용 증가에 기여하고 있습니다. 또한, 자기 확장형 금속 합금과 최신 생분해성 재료 등 스텐트 재료 공학의 발전으로 장치의 성능이 향상되어 수의학 현장에서의 임상적 용도가 확대되고 있습니다.

2025년에는 개 부문이 60.6%의 점유율을 차지했습니다. 이 부문 시장 확대는 개군에서 스텐트 치료를 필요로 하는 질환이 증가하고 있기 때문입니다. 호흡기, 비뇨기계, 혈관계에 영향을 미치는 다양한 구조적 합병증에서는 정상적인 생리기능을 회복하기 위해 스텐트 삽입을 통한 개입이 필요할 수 있습니다. 전 세계적으로 반려견의 수가 많고 수의학에 대한 지출이 증가하고 있는 것도 이 부문의 성장을 더욱 촉진하고 있습니다. 수의사들은 중요한 체내 경로에서 구조적 협착이나 막힘이 발생한 개에 대한 효과적인 치료법으로 스텐트 시술을 점점 더 많이 활용하고 있습니다.

2025년 북미 수의학 스텐트 시장은 41.5%의 점유율을 차지했습니다. 이 지역이 선도적인 위치에 있는 것은 고도로 발달된 수의학 인프라와 반려동물을 위한 첨단 치료 옵션이 광범위하게 이용 가능한 것이 주요 요인입니다. 북미 전역에는 스텐트 삽입을 포함한 복잡한 최소침습 수술을 수행할 수 있는 시설을 갖춘 수많은 전문 동물병원, 진료 의뢰 센터 및 첨단 임상 시설이 있습니다. 또한, 반려동물 의료에 대한 소비자의 지출이 견조하고, 반려동물 보험 프로그램의 이용 가능성은 고급 수의학 치료에 대한 비용 부담을 줄이는 데 기여하고 있습니다. 이러한 요인들이 결합되어 혁신적인 수의학 솔루션의 도입을 촉진하고 지역 내 수의학 스텐트 시장의 지속적인 성장을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022-2035

제6장 시장 추산 및 예측 : 동물별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 재료별, 2022-2035

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.04.23The Global Veterinary Stents Market was valued at USD 47.5 million in 2025 and is estimated to grow at a CAGR of 7% to reach USD 92 million by 2035.

Growth in the veterinary stents market is strongly influenced by the increasing focus on improving animal health and advancing treatment standards within veterinary medicine. As pet ownership continues to rise globally, veterinarians and pet owners are placing greater emphasis on effective medical interventions that enhance the quality of life for companion animals. Veterinary stents are increasingly recognized as an important treatment option for animals experiencing structural narrowing or blockages in vital body passages. At the same time, rapid technological advancements have significantly improved the performance and reliability of these devices. The development of minimally invasive veterinary procedures, along with improved stent designs and advanced biomaterials, has enhanced the success rate of implantation procedures. In addition, improvements in imaging and placement technologies are enabling veterinarians to deliver more precise and efficient treatments. These advancements are contributing to better clinical outcomes, faster recovery for animals, and reduced complication rates. As a result, veterinary stents are gaining wider acceptance among veterinary professionals while also receiving greater trust from pet owners seeking advanced treatment options.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $47.5 Million |

| Forecast Value | $92 Million |

| CAGR | 7% |

Veterinary stents function as specialized implants designed to treat animals experiencing blockages or narrowing within certain internal pathways caused by disease, injury, or developmental abnormalities. These cylindrical devices are typically manufactured using durable metal alloys or polymer-based materials and are inserted into tubular anatomical structures to maintain proper passage and restore normal physiological function. By providing structural support within affected areas, veterinary stents help improve airflow, circulation, or fluid movement, depending on the location of placement.

The airway stents segment generated USD 18.7 million in 2025. Segment growth is primarily associated with the rising incidence of airway-related disorders among companion animals that require long-term structural support within the respiratory tract. Such conditions can lead to severe breathing complications and require immediate medical intervention to restore proper airflow. The growing preference among veterinarians and pet owners for minimally invasive treatment approaches has contributed to the increased use of airway stents. Additionally, advancements in stent material engineering, including self-expanding metal alloys and modern biodegradable materials, have improved device performance and expanded their clinical use within veterinary practices.

The dogs segment held 60.6% share in 2025. Market expansion within this segment is driven by the rising occurrence of medical conditions in canine populations that require stent-based treatment. Various structural complications affecting the respiratory, urinary, and vascular systems can require intervention through stent placement to restore normal physiological function. The high global population of companion dogs and increasing spending on veterinary healthcare further support the growth of this segment. Veterinarians are increasingly utilizing stent procedures as an effective treatment solution for dogs experiencing structural narrowing or obstructions within critical internal pathways.

North America Veterinary Stents Market accounted for 41.5% share in 2025. The region's leadership position is largely supported by its highly developed veterinary healthcare infrastructure and widespread availability of advanced treatment options for companion animals. Numerous specialized veterinary hospitals, referral centers, and advanced clinical facilities across North America are equipped to perform complex minimally invasive procedures, including stent implantation. In addition, strong consumer spending on pet healthcare and the availability of pet insurance programs contribute to greater affordability for advanced veterinary procedures. These factors collectively encourage the adoption of innovative veterinary treatment solutions and support the continued growth of the veterinary stents market across the region.

Key companies operating in the Global Veterinary Stents Market include Infiniti Medical, Dextronix, TaeWoong Medical, UltraVet Medical Devices, Create Medic, M.I. Tech, AbtVet (Stening Group), and EpiicVet. Companies competing in the Veterinary Stents Market are implementing several strategic initiatives to strengthen their market presence and expand global reach. Leading manufacturers are focusing heavily on research and development to introduce advanced stent designs with improved durability, flexibility, and biocompatibility. Many companies are also investing in the development of innovative materials and minimally invasive delivery systems to enhance treatment effectiveness and simplify clinical procedures for veterinarians. Strategic collaborations with veterinary hospitals, specialty clinics, and research institutions are helping companies improve product adoption and clinical validation. Additionally, market participants are expanding their distribution networks and strengthening regional partnerships to increase accessibility to veterinary stent technologies across emerging markets while maintaining strong competitiveness in established veterinary healthcare sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Animal trends

- 2.2.4 Application trends

- 2.2.5 Material trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership

- 3.2.1.2 Prevalence of respiratory and urological disorders

- 3.2.1.3 Growing awareness of pet health and healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary stents and procedures

- 3.2.2.2 Risk of stent-related complications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of veterinary specialty hospitals and referral centers

- 3.2.3.2 Technological advancements in veterinary interventional devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.7 Impact of AI on the market

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Airway stents

- 5.3 Vascular stents

- 5.4 Urethral stents

- 5.5 Other stents

Chapter 6 Market Estimates and Forecast, By Animal, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Other animals

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Airway collapse

- 7.3 Vascular obstructions

- 7.4 Urinary tract obstructions

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Nitinol

- 8.3 Biodegradable polymer

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals and clinics

- 9.3 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbtVet (Stening group)

- 11.2 Create Medic

- 11.3 Dextronix

- 11.4 EpiicVet

- 11.5 Infiniti Medical

- 11.6 M.I. Tech

- 11.7 TaeWoong Medical

- 11.8 UltraVet Medical Devices