|

시장보고서

상품코드

1998788

운전자 경고 시스템 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Driver Alert System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

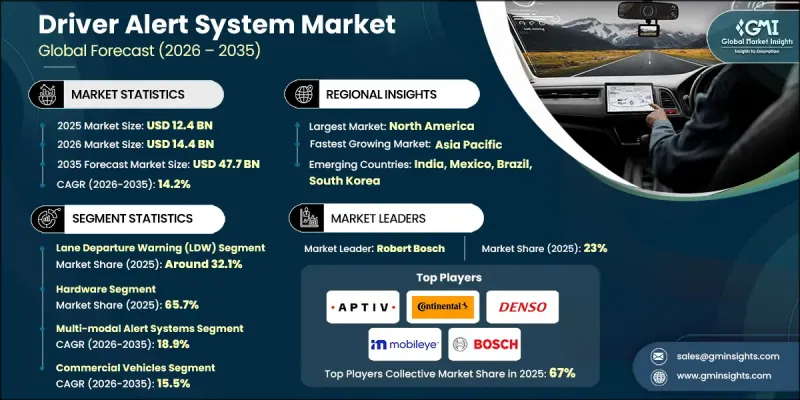

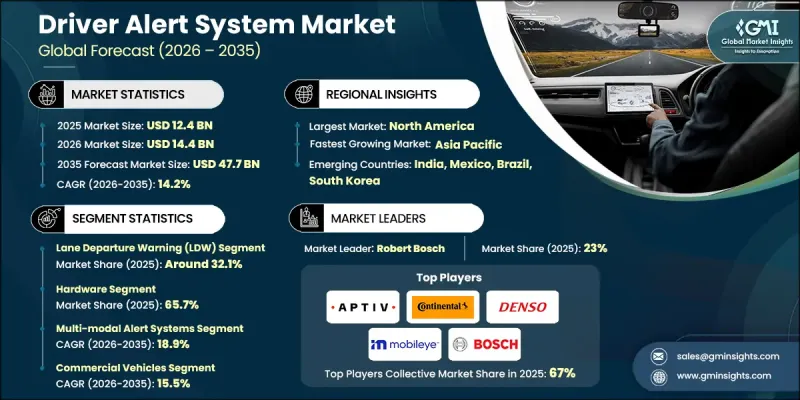

세계의 운전자 경고 시스템 시장은 2025년에 124억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 14.2%로 성장하여 477억 달러에 달할 것으로 예측됩니다.

인위적인 실수는 여전히 전 세계 교통사고의 주요 원인으로 작용하고 있으며, 각국 정부는 차량에 첨단 안전 기술 탑재를 의무화하는 규제를 도입하고 있습니다. 자동차 제조업체들은 첨단운전자보조시스템(ADAS)의 일환으로 승용차 및 상용차에 운전자 경고 시스템을 점점 더 많이 탑재하고 있습니다. 이 시스템은 AI, 카메라, 적외선 센서, 조향 입력 모니터링을 통해 눈꺼풀의 움직임, 시선 방향, 머리 위치를 추적하고 운전자의 피로와 주의 산만함을 감지합니다. 경고는 시각적, 청각적 또는 촉각적 신호를 통해 전달되어 사고가 발생하기 전에 미연에 방지할 수 있도록 도와줍니다. AI를 활용한 인식 기술, 다중 센서 융합 및 딥러닝 모델 채택 확대로 감지 정확도가 향상되고, 오경보가 감소하며, 다양한 환경 조건에서 시스템의 신뢰성이 향상되고 있습니다. 증가하는 규제 압력과 도로 안전 향상에 대한 수요는 전 세계 여러 차량 부문에서 시장 확대를 주도하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 124억 달러 |

| 예측액 | 477억 달러 |

| CAGR | 14.2% |

차선이탈경보(LDW) 부문은 32.1%의 점유율을 차지하며 2025년 40억 달러 시장 규모를 형성했습니다. LDW 시스템은 차량이 차선을 이탈하는 것을 방지하여 교통사고의 주요 원인 중 하나인 차선 이탈을 방지합니다. 이러한 시스템은 차선 이탈 전에 운전자에게 경고함으로써 안전성을 높이고 사고 관련 비용을 절감하여 소비자와 규제 당국의 기대에 부응하고 있습니다. LDW 기술의 보급으로 시장 침투율과 수익이 확대되어 현대 자동차의 주요 안전 솔루션으로 자리매김하고 있습니다. ADAS 패키지의 채택이 증가함에 따라 승용차와 상용차 모두에서 이 부문의 지속적인 성장이 예상됩니다.

하드웨어 부문은 2025년 65.7%의 점유율을 차지했으며, 2035년까지 300억 달러에 달할 것으로 전망됩니다. 고해상도 카메라, 레이더, LiDAR 센서, 초음파 장치 등의 핵심 구성요소를 통해 차선 변경, 충돌, 운전자 주의력 등을 실시간으로 모니터링할 수 있습니다. 8-12메가픽셀 카메라, 각도 분해능이 향상된 레이더, 처리 속도가 10-100배 빠른 AI 프로세서 등의 기술 발전으로 악천후에서도 감지 정확도가 크게 향상되었습니다. 이러한 개선을 통해 운전자 경고 시스템은 에너지 효율과 열 관리를 유지하면서 피로, 산만함, 운전자의 의도를 효과적으로 식별할 수 있게 되었습니다.

미국의 운전자 경고 시스템 시장은 2025년 42억 달러에 달했습니다. 탄탄한 자동차 생산, 안전에 대한 소비자의 선호도, 엄격한 규제가 이 지역의 성장을 견인하고 있습니다. 미국 도로교통안전국(NHTSA), 신차평가프로그램(NCAP) 등 규제기관이 주도하는 프로그램은 사각지대 감지, 차선 유지 지원, 자동 긴급 제동 등 첨단 안전 기능의 통합을 촉진하고 있습니다. 이러한 노력은 자동차 제조업체들이 운전자 경고 기술을 보다 광범위하게 도입하도록 장려하고, 시장 확대를 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 시스템별, 2022-2035

제6장 시장 추산 및 예측 : 솔루션별, 2022-2035

제7장 시장 추산 및 예측 : 경계체제별, 2022-2035

제8장 시장 추산 및 예측 : 차량별, 2022-2035

제9장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.04.23The Global Driver Alert System Market was valued at USD 12.4 billion in 2025 and is estimated to grow at a CAGR of 14.2% to reach USD 47.7 billion by 2035.

Human error remains the leading cause of road accidents worldwide, prompting governments to implement regulations mandating advanced safety technologies in vehicles. Automakers are increasingly integrating driver alert systems into passenger and commercial vehicles as part of Advanced Driver Assistance Systems (ADAS). These systems utilize AI, cameras, infrared sensors, and steering input monitoring to track eyelid movement, gaze direction, and head position, allowing them to detect driver fatigue or distraction. Alerts are delivered through visual, auditory, or tactile signals, helping prevent accidents before they occur. The growing adoption of AI-powered perception, multi-sensor fusion, and deep learning models is enhancing detection accuracy, reducing false alarms, and improving system reliability under varying environmental conditions. Rising regulatory pressure and the demand for improved road safety are driving market expansion across multiple vehicle segments globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $47.7 Billion |

| CAGR | 14.2% |

The lane departure warning (LDW) segment held a 32.1% share, generating USD 4 billion in 2025. LDW systems help prevent vehicles from drifting out of lanes, addressing one of the primary causes of traffic accidents. By alerting drivers before lane departures, these systems enhance safety, reduce accident-related costs, and meet both consumer and regulatory expectations. Widespread adoption of LDW technology has boosted market penetration and revenue, solidifying its position as a key safety solution in modern vehicles. Increasing inclusion in ADAS packages ensures continued growth for this segment across both passenger and commercial vehicles.

The hardware segment accounted for 65.7% share in 2025 and is expected to reach USD 30 billion by 2035. Critical components such as high-resolution cameras, radar, LiDAR sensors, and ultrasonic devices enable real-time monitoring of lane changes, collisions, and driver alertness. Technological advances, including 8-12 MP cameras, radar with improved angular resolution, and AI processors offering 10-100X faster performance, have significantly enhanced detection accuracy even in adverse weather. These improvements allow driver alert systems to effectively identify fatigue, distraction, and driver intentions while maintaining energy efficiency and thermal management.

United States Driver Alert System Market reached USD 4.2 billion in 2025. Strong automotive manufacturing, consumer preference for safety, and stringent regulations are driving growth in the region. Programs led by regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) and New Car Assessment Program (NCAP) encourage the integration of advanced safety features, including blind-spot detection, lane-keeping assist, and automatic emergency braking. These initiatives incentivize automakers to incorporate driver alert technologies more broadly, reinforcing market expansion.

Key companies operating in the Global Driver Alert System Market include Mobileye, Autoliv, Aptiv, Robert Bosch, ZF, Valeo, Hyundai Mobis, Magna, DENSO, and Continental. Companies in the Global Driver Alert System Market are strengthening their position through strategic investments in AI and sensor technology, enhancing detection accuracy and system reliability. Leading manufacturers are expanding partnerships with automakers to integrate driver alert systems into new models and ADAS packages. Firms are investing in research and development for multi-sensor fusion and machine learning algorithms to reduce false alerts and improve performance in diverse conditions. Geographic expansion into emerging automotive markets supports broader adoption. Companies are also focusing on compliance with evolving safety regulations, offering tailored solutions for passenger and commercial vehicles.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System

- 2.2.3 Solution

- 2.2.4 Alert

- 2.2.5 Vehicle

- 2.2.6 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent government safety regulations & mandates

- 3.2.1.2 Rising consumer awareness on road safety

- 3.2.1.3 Fleet operator demand for driver monitoring

- 3.2.1.4 Integration with autonomous driving systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced DAS components

- 3.2.2.2 Lack of standardization across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets with growing vehicle sales

- 3.2.3.2 Aftermarket retrofit solutions for existing fleets

- 3.2.3.3 AI-powered personalized alert systems

- 3.2.3.4 Commercial vehicle & logistics sector growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Federal Motor Vehicle Safety Standards (FMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 UNECE WP.29

- 3.4.2.3 EU General Safety Regulation (GSR) 2019/2144

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan NCAP

- 3.4.3.2 China NCAP

- 3.4.3.3 AIS (Automotive Industry Standards)

- 3.4.4 Latin America

- 3.4.4.1 Brazil National Traffic Council (CONTRAN)

- 3.4.4.2 INMETRO

- 3.4.4.3 ANSV

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Standardization Organization (GSO)

- 3.4.5.2 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.1 North America

- 3.5 Investment & Funding Analysis

- 3.5.1 Venture Capital & Private Equity Activity

- 3.5.2 Corporate Investment Trends

- 3.5.3 Government Funding & Incentives

- 3.5.4 M&A Deal Flow Analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 AI-based driver monitoring systems (DMS)

- 3.8.1.2 Sensor fusion integration

- 3.8.1.3 Infrared (IR) camera deployment

- 3.8.1.4 Integration with ADAS platforms

- 3.8.2 Emerging technologies

- 3.8.2.1 Radar-based in-cabin monitoring

- 3.8.2.2 AI-powered behavioral prediction models

- 3.8.2.3 Generative AI-assisted adaptive alert systems

- 3.8.1 Current technological trends

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus)

- 3.9.3 OEM vs Aftermarket Price Differentiation

- 3.9.4 Regional Price Variation Analysis

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Integration with autonomous & ADAS ecosystem

- 3.12.1 Sensor data sharing & fusion architectures

- 3.12.2 V2X communication integration

- 3.12.3 Handover protocols between automated & manual driving

- 3.12.4 Redundancy & fail-safe mechanisms

- 3.13 Cybersecurity & functional safety analysis

- 3.13.1 Cybersecurity threats & attack vectors

- 3.13.2 Encryption & data protection protocols

- 3.13.3 Safety-critical system validation

- 3.13.4 Over-the-Air (OTA) update security

- 3.14 Capacity & production landscape (Driven by Primary Research)

- 3.14.1 Installed capacity by region & key producer

- 3.14.2 Capacity utilization rates & expansion pipelines

- 3.15 Case studies

- 3.16 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By System, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Lane Departure Warning (LDW)

- 5.3 Forward Collision Warning (FCW)

- 5.4 Blind Spot Detection (BSD)

- 5.5 Driver Fatigue Monitor (DFM)

- 5.6 Driver Distraction Detection

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Sensors

- 6.2.2 Cameras

- 6.2.3 Others

- 6.3 Software

- 6.3.1 In-vehicle software

- 6.3.2 Mobile app based

Chapter 7 Market Estimates & Forecast, By Alert, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Visual Alert Systems

- 7.3 Audio Alert Systems

- 7.4 Tactile Alert Systems

- 7.5 Multi-Modal Alert Systems

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Russia

- 10.3.8 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Vietnam

- 10.4.9 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Robert Bosch

- 11.1.2 Continental

- 11.1.3 DENSO

- 11.1.4 ZF

- 11.1.5 Aptiv

- 11.1.6 Magna

- 11.1.7 Autoliv

- 11.1.8 Mobileye

- 11.1.9 Valeo

- 11.1.10 Hyundai Mobis

- 11.2 Regional players

- 11.2.1 Smart Eye

- 11.2.2 Seeing Machines

- 11.2.3 Ficosa

- 11.2.4 Visteon

- 11.2.5 Harman

- 11.2.6 Faurecia

- 11.3 Emerging players

- 11.3.1 Jungo Connectivity

- 11.3.2 Affectiva

- 11.3.3 Xperi/Perceive

- 11.3.4 Neonode