|

시장보고서

상품코드

1998791

육상 원격 무기 스테이션 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Land-Based Remote Weapon Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

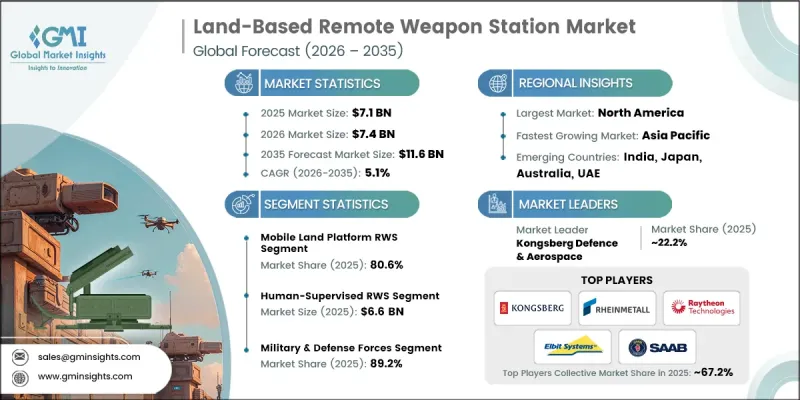

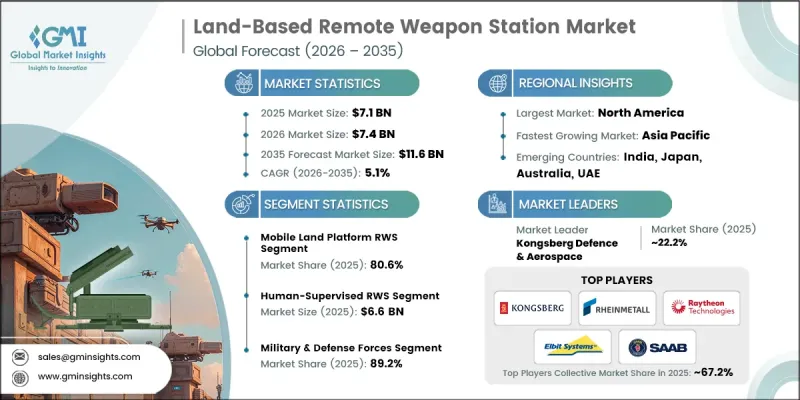

세계의 육상 원격 무기 스테이션 시장은 2025년에 71억 달러로 평가되었고, CAGR 5.1%로 성장하여 2035년에는 116억 달러에 달할 것으로 예측됩니다.

시장 확대는 NATO 및 인도 태평양 지역의 장갑차 현대화 프로그램 증가, 비대칭 전쟁에서 승무원 생존성에 대한 관심 증가, 전술 차량 수준의 대 무인항공기(UAS) 솔루션의 통합으로 인한 시장 확대에 힘입은 바 큽니다. 또한, 군는 네트워크화된 전장 아키텍처에 첨단 원격 살상 시스템을 통합하고 있으며, 국경 보안 및 기동 작전을 위해 가볍고 신속하게 배치할 수 있는 무기 스테이션을 점점 더 많이 조달하고 있습니다. NATO 동부전선 현대화 프로그램이 주요 촉진요인으로 작용하고 있으며, 회원국들은 지역 내 위협의 변화에 대응하기 위해 차량의 생존성을 향상시키고 있습니다. 각국 정부가 최전방 차량에 첨단 원격 사격 시스템을 도입함에 따라 무인 포탑의 채택도 확대되고 있습니다. 2022년 이후 고도의 분쟁과 비대칭 분쟁에서 대(對)드론 능력은 매우 중요하며, 차량 수준의 통합은 2032년까지 지속될 것으로 예측됩니다. 이러한 혁신은 인원의 전술적 방어를 향상시키는 동시에 원격 무기 시스템의 운영 다양성을 기존의 직접 사격 기능을 넘어 확장할 수 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 71억 달러 |

| 예측액 | 116억 달러 |

| CAGR | 5.1% |

고정식 육상 설치형 원격 무기 스테이션 시장은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.3%를 나타낼 것으로 예측됩니다. 이러한 성장은 요새화된 국경, 중요 인프라 및 전방 작전 기지에 배치된 배치에 의해 뒷받침되고 있습니다. 국경 간 긴장이 고조되고 드론의 보급이 확산됨에 따라 주변 경비를 위한 원격 조종식 방어 시스템에 대한 수요가 증가하고 있습니다. 이러한 장비는 지속적인 모니터링, 자동 표적 추적 및 운영자의 위험 노출 감소를 제공하여 정적 방어 네트워크의 효율성을 향상시키고 지속적인 투자를 촉진합니다.

유인 모니터링 RWS 부문은 2025년 66억 달러에 달했습니다. OITL(Operator in the Loop) 시스템이 선호되는 배경에는 민간 영역에서의 책임과 위험 감소를 요구하는 국제 교전규칙과 규제 프레임워크가 있습니다. 군은 기존 장갑차 군단 및 기존 지휘망과의 호환성 때문에 감시형 시스템을 선호하고 있습니다. 이를 통해 안전 및 인도주의적 기준을 준수하면서 작전상 우위를 유지할 수 있습니다.

2025년 북미 육상 원격 무기 스테이션 시장은 33.8%의 점유율을 차지했습니다. 이 지역의 성장은 진행 중인 국방 현대화 프로그램, 국방 예산 확대, 첨단 RWS 기술 조달에 의해 주도되고 있습니다. 이 시장은 미 육군과 국방부의 현대화 이니셔티브, 국경을 따라 국토 안보 요건, 그리고 군과 치안 부대 전반에 걸쳐 원격 무기 시스템의 통합을 지원하는 기존 산업 기반으로부터 혜택을 받고 있습니다. 북미의 네트워크화된 무기, 자율 교전 시스템 및 국경 방어 능력에 대한 집중은 2035년까지 꾸준한 성장을 유지할 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 플랫폼 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 무기 유형별, 2022년-2035년

제7장 시장 추산 및 예측 : 자율 레벨별, 2022년-2035년

제8장 시장 추산 및 예측 : 최종사용자별, 2022년-2035년

제9장 시장 추산 및 예측 : 지역별, 2022년-2035년

제10장 기업 개요

LSH 26.04.23The Global Land-Based Remote Weapon Station Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 11.6 billion in 2035.

Market expansion is fueled by increasing armored vehicle modernization programs across NATO and Indo-Pacific regions, the growing emphasis on crew survivability in asymmetric warfare, and the rising integration of counter-UAS solutions at the tactical vehicle level. Military forces are also incorporating advanced remote lethality systems into networked battlefield architectures, while lightweight, rapidly deployable weapon stations are increasingly being procured for border security and mobile operations. NATO Eastern flank modernization programs are a key driver, with member states enhancing vehicle survivability to address evolving regional threats. The adoption of unmanned turrets is gaining traction as governments implement advanced remote fire systems for frontline vehicles. Counter-drone capabilities have become critical in high-intensity and asymmetric conflicts post-2022, and their integration at the vehicle level is expected to continue until 2032. These innovations improve tactical protection for personnel while expanding the operational versatility of remote weapon systems beyond traditional direct-fire functions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 5.1% |

The fixed land installation remote weapon stations segment is expected to grow at a CAGR of 7.3% during 2026-2035. This growth is supported by deployments across fortified borders, critical infrastructure, and forward operating bases. Heightened cross-border tensions and the proliferation of drones are driving demand for remotely operated defense systems for perimeter security. These installations offer persistent surveillance, automated target tracking, and reduced operator exposure, which enhances the effectiveness of static defense networks and encourages continued investment.

The human-supervised RWS segment reached USD 6.6 billion in 2025. Preference for operator-in-the-loop systems is driven by international rules of engagement and regulatory frameworks that demand accountability and risk reduction in civilian areas. Military forces favor supervised systems for their compatibility with existing armored vehicle fleets and legacy command networks, which allows them to maintain operational dominance while adhering to safety and humanitarian standards.

North America Land-Based Remote Weapon Station Market held a 33.8% share in 2025. Growth in this region is driven by ongoing defense modernization programs, elevated defense budgets, and procurement of advanced RWS technologies. The market benefits from U.S. Army and Department of Defense modernization initiatives, homeland security requirements along borders, and a well-established industrial base that supports integration of remote weapon systems across military and security forces. North America's focus on networked weapons, autonomous engagement systems, and border defense capabilities is expected to sustain steady growth through 2035.

Key players in the Global Land-Based Remote Weapon Station Market include Kongsberg Defence & Aerospace, Electro Optic Systems, ASELSAN A.S, General Dynamics Corporation, Thales Group, FN Herstal, Elbit Systems Ltd., Rafael Advanced Defense Systems, BAE Systems plc, Leonardo S.p.A, Rheinmetall AG, Saab AB, ST Engineering, and RTX Corporation. Companies operating in the Global Land-Based Remote Weapon Station Market are employing multiple strategies to strengthen their position and expand market share. They are investing in R&D to develop autonomous engagement systems, counter-UAS technologies, and lightweight modular weapon stations. Strategic alliances with defense agencies and technology firms allow integration of advanced systems into existing fleets. Manufacturers are also expanding production capacity, establishing regional service centers, and offering operator training programs. Emphasis on interoperability, networked battlefield solutions, and modular designs enables rapid upgrades and multi-platform deployment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Weapon type trends

- 2.2.3 Autonomy level trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 NATO Eastern flank vehicle survivability upgrades

- 3.2.1.2 U.S. Army CROWS modernization programs

- 3.2.1.3 Rising demand for unmanned turret integration

- 3.2.1.4 Infantry fighting vehicle fleet digitization

- 3.2.1.5 Lightweight RWS adoption on tactical vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Export restrictions under ITAR regulations

- 3.2.2.2 Integration complexity with legacy armored fleets

- 3.2.3 Market opportunities

- 3.2.3.1 AI-enabled autonomous target recognition upgrades

- 3.2.3.2 Hybrid electric combat vehicle integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Mobile land platform RWS

- 5.2.1 Combat vehicles (armored fighting vehicles)

- 5.2.1.1 Infantry fighting vehicles (IFVs)

- 5.2.1.2 Armored personnel carriers (APCs)

- 5.2.1.3 Main battle tanks (MBTs)-secondary armament

- 5.2.2 Tactical Vehicles

- 5.2.2.1 Joint light tactical vehicles (JLTV)

- 5.2.2.2 Mine-resistant ambush protected (MRAP) vehicles

- 5.2.2.3 Tactical trucks & logistics vehicles

- 5.2.3 Unmanned ground vehicles (UGVs)

- 5.2.1 Combat vehicles (armored fighting vehicles)

- 5.3 Fixed land installation RWS

- 5.3.1 Permanent installations

- 5.3.2 Deployable / containerized systems

Chapter 6 Market Estimates and Forecast, By Weapon Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Light (5.56mm - 7.62mm)

- 6.3 Medium (12.7mm - 14.5mm)

- 6.4 Heavy (20mm - 40mm+)

Chapter 7 Market Estimates and Forecast, By Autonomy Level, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Human-supervised RWS

- 7.3 Autonomous engagement RWS

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Military & defense forces

- 8.3 Law enforcement & border security forces

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Rheinmetall AG

- 10.1.2 BAE Systems plc

- 10.1.3 Kongsberg Defence & Aerospace

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 General Dynamics Corporation

- 10.2.1.2 RTX Corporation

- 10.2.2 Asia Pacific

- 10.2.2.1 ASELSAN A.S

- 10.2.2.2 Electro Optic Systems

- 10.2.2.3 ST Engineering

- 10.2.3 Europe

- 10.2.3.1 Saab AB

- 10.2.3.2 Leonardo S.p.A

- 10.2.3.3 FN Herstal

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Elbit Systems Ltd.

- 10.3.2 Rafael Advanced Defense Systems

- 10.3.3 Thales Group