|

시장보고서

상품코드

1998801

항공기 연료 탱크 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aircraft Fuel Tanks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

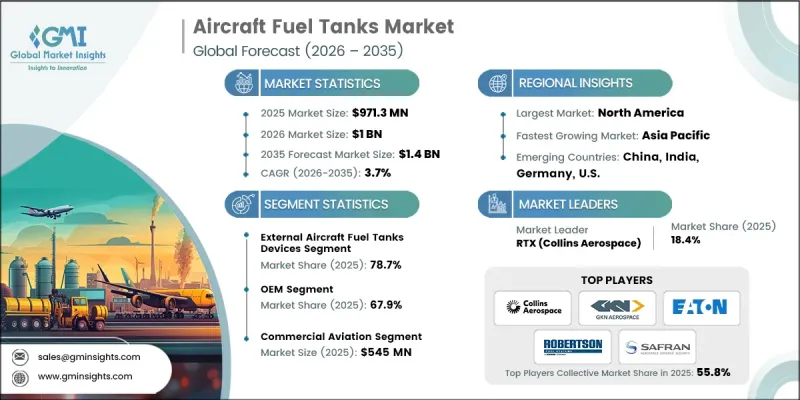

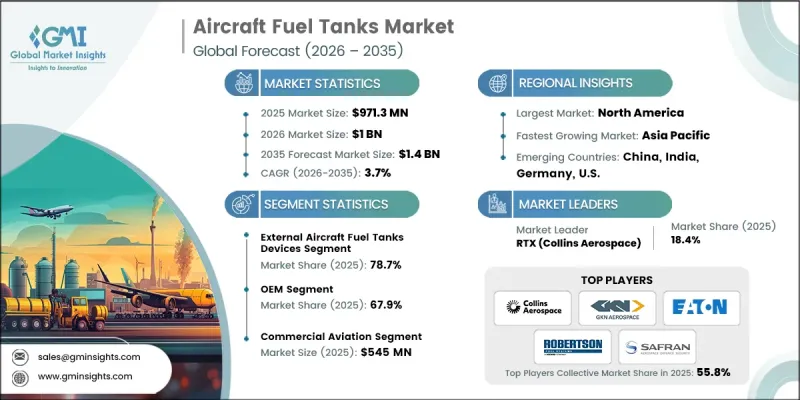

세계의 항공기 연료 탱크 시장은 2025년에 9억 7,130만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.7%로 성장하여 14억 달러에 달할 것으로 예측됩니다.

항공기 연료탱크 산업의 성장은 항공 생태계 내의 몇 가지 구조적 추세에 의해 주도되고 있습니다. 지역 항공 네트워크의 확대와 비즈니스 항공기에 대한 수요 증가로 인해 효율적인 기내 연료 저장 솔루션에 대한 수요가 지속적으로 발생하고 있습니다. 또한, 국방 항공군 전체의 현대화 프로그램으로 인해 작전 능력의 확장을 지원하는 첨단 연료 탱크 기술에 대한 요구가 증가하고 있습니다. 민간 항공기 생산량 증가도 통합형 연료탱크 시스템에 대한 수요 증가에 기여하고 있습니다. 각 제조업체들은 항공기 전체 성능을 향상시키고, 더 가볍고 효율적인 설계에 점점 더 집중하고 있습니다. 복합재 구조와 같은 첨단 소재와 개선된 연료 저장 기술의 통합으로 항공 산업 전반의 설계 기준이 재편되고 있습니다. 항공기 제조업체와 운항사가 연료 효율성, 운항 유연성, 장기적인 성능 향상을 우선시하는 가운데, 항공기 연료탱크 시장은 전 세계 항공우주 산업 전반에서 안정적인 성장을 유지할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 9억 7,130만 달러 |

| 예측액 | 14억 달러 |

| CAGR | 3.7% |

항공기 연료탱크 시장의 성장을 뒷받침하는 중요한 요인 중 하나는 민간 항공기의 생산량 증가입니다. 승객 수 증가와 항공사의 항공기 증설 계획으로 인해 항공기 제조업체들은 생산에 박차를 가하고 있으며, 이는 연료 저장 시스템에 대한 수요를 직접적으로 견인하고 있습니다. 항공사들이 운항 효율을 높이기 위해 노력하는 가운데, 경량 구조 부품과 최적화된 연료 용량 솔루션에 대한 관심이 높아지고 있습니다. 지역 간 항공 네트워크의 확대와 단거리 노선망의 정비도 소형 항공기 카테고리에 대한 수요를 자극하고 있으며, 이로 인해 신뢰할 수 있는 연료 탱크 시스템에 대한 요구가 더욱 높아지고 있습니다. 항공기 운항사는 서비스 범위 확대와 운항 효율성 향상을 위해 지속적으로 기재를 확충하고 있습니다. 동시에, 연료 탱크 설계의 기술 발전은 업계를 변화시키고 있습니다. 제조업체들은 기존 금속 부품을 대체할 수 있는 복합재료와 첨단 합금 구조로 전환하고 있으며, 이를 통해 경량화 및 연비 효율을 향상시킬 수 있습니다.

제품 카테고리별로는 항공기용 외부 연료탱크 장치 부문이 2025년 78.7%의 점유율을 차지할 것으로 예측됩니다. 이 부문의 강력한 입지는 운영 성능 향상을 위해 연료 저장 용량을 늘려야 하는 특수 항공 플랫폼에서 광범위하게 사용되는 것과 관련이 있습니다. 이러한 시스템은 운영의 유연성을 제공하고, 더 긴 항속거리가 필요한 경우 항공기가 추가 연료를 탑재할 수 있도록 해줍니다. 항공기 플랫폼에 통합하거나 개조할 수 있다는 점도 다양한 항공 분야에 폭넓게 적용될 수 있도록 돕고 있습니다. 항공사가 항속거리와 임무 지속시간 향상에 계속 집중하고 있는 가운데, 항공기 외부 연료탱크 시스템에 대한 수요는 OEM(1차 제조) 및 애프터마켓 채널 모두에서 견조한 성장세를 보이고 있습니다.

비즈니스 및 일반 항공 부문은 2035년까지 연평균 복합 성장률(CAGR) 3.8%를 나타낼 것으로 예측됩니다. 민간 항공, 소형 고정익 및 회전익 플랫폼에 대한 수요 증가는 신규 항공기 생산과 애프터마켓 서비스 모두에서 연료탱크 시스템 탑재 증가에 기여하고 있습니다. 지속적인 기체 업데이트 및 현대화 노력은 첨단 연료 저장 기술의 도입을 촉진하고 있습니다. 경량 복합재 탱크 구조의 채택과 디지털 연료 모니터링 및 관리 시스템 개선이 결합되어 운영 효율성과 항공기 성능 향상에 기여하고 있습니다. 이러한 추세는 기존 항공 분야뿐만 아니라 발전 중인 항공우주 시장에서도 항공기용 연료탱크 시장의 꾸준한 확대를 뒷받침하고 있습니다.

2025년 북미 항공기 연료 탱크 시장은 35.9%의 점유율을 차지했습니다. 이 지역은 활발한 항공기 제조 활동과 항공사의 항공기 보유량 증가로 인해 주요 항공 허브의 지위를 유지하고 있습니다. 미국 및 캐나다의 항공기 인도량 증가는 항공기 제조 시 연료탱크 설치 수요 증가에 기여하고 있습니다. 이 지역 항공사들은 증가하는 국내 및 국제선 항공 수요에 대응하기 위해 지속적으로 항공기 보유 능력을 확대되고 있습니다. 동시에 항공업계의 이해관계자들은 첨단 연료 저장 기술을 통해 연비 효율을 개선하고 운항 안전성을 강화하는 것을 우선순위로 삼고 있습니다. 복합재 연료탱크와 첨단 연료 관리 시스템의 도입은 항공기 연료탱크 산업에서 이 지역의 선도적 지위를 강화하는 동시에 장기적인 항공 산업의 성장을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035

제6장 시장 추산 및 예측 : 플랫폼별, 2022-2035

제7장 시장 추산 및 예측 : 재료별, 2022-2035

제8장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.23The Global Aircraft Fuel Tanks Market was valued at USD 971.3 million in 2025 and is estimated to grow at a CAGR of 3.7% to reach USD 1.4 billion by 2035.

Growth in the aircraft fuel tanks industry is driven by several structural trends within the aviation ecosystem. Expanding regional aviation networks and increasing demand for business aircraft are creating consistent requirements for efficient onboard fuel storage solutions. In addition, modernization programs across defense aviation fleets are increasing the need for advanced fuel tank technologies that support extended operational capabilities. Rising production volumes of commercial aircraft are also contributing to higher demand for integrated fuel tank systems. Manufacturers are increasingly focusing on lighter and more efficient designs that improve overall aircraft performance. The integration of advanced materials such as composite structures and improved fuel storage technologies is reshaping design standards across the aviation sector. As aircraft manufacturers and operators prioritize fuel efficiency, operational flexibility, and long-term performance improvements, the aircraft fuel tanks market is expected to maintain stable growth across the global aerospace industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $971.3 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 3.7% |

A significant factor supporting the growth of the aircraft fuel tanks market is the rising manufacturing output of commercial aircraft. Increasing passenger traffic and airline fleet expansion programs are encouraging aircraft manufacturers to accelerate production, which directly drives demand for fuel storage systems. As aviation companies work to improve operational efficiency, greater emphasis is being placed on lightweight structural components and optimized fuel capacity solutions. The expansion of regional air connectivity and shorter route networks is also stimulating demand for smaller aircraft categories, which further strengthens the need for reliable fuel tank systems. Aircraft operators are continuing to expand fleets to improve service reach and operational efficiency. At the same time, technological advancements in fuel tank design are transforming the industry. Manufacturers are transitioning toward composite materials and advanced alloy structures to replace conventional metal components, enabling weight reduction and enhanced fuel efficiency.

In terms of product category, the external aircraft fuel tanks devices segment accounted for 78.7% share in 2025. The strong position of this segment is associated with its extensive utilization in specialized aviation platforms that require increased fuel storage capacity for extended operational performance. These systems provide operational flexibility and enable aircraft to carry additional fuel when longer operational ranges are required. Their ability to be integrated or retrofitted into aircraft platforms further supports their widespread adoption across multiple aviation applications. As aviation operators continue to focus on enhancing operational range and mission endurance, demand for external aircraft fuel tank systems remains strong across both original equipment manufacturing and aftermarket channels.

The business and general aviation segment is projected to grow at a CAGR of 3.8% during 2035. Expanding demand for private aviation, smaller fixed-wing aircraft, and rotary-wing platforms is contributing to increased installations of fuel tank systems in both new aircraft production and aftermarket services. Continuous fleet upgrades and modernization initiatives are encouraging the integration of advanced fuel storage technologies. The adoption of lightweight composite tank structures, combined with improvements in digital fuel monitoring and management systems, is helping enhance operational efficiency and aircraft performance. These developments are supporting the steady expansion of the aircraft fuel tanks market across established aviation regions as well as developing aerospace markets.

North America Aircraft Fuel Tanks Market accounted for 35.9% share in 2025. The region continues to represent a major aviation hub due to strong aircraft manufacturing activity and expanding airline fleets. Increasing aircraft deliveries across the United States and Canada are contributing to rising demand for fuel tank installations during aircraft production. Airlines in the region are continuing to expand fleet capacity to accommodate growing domestic and international air travel demand. At the same time, aviation stakeholders are prioritizing improved fuel efficiency and enhanced operational safety through advanced fuel storage technologies. The adoption of composite fuel tanks and sophisticated fuel management systems is strengthening the region's leadership position in the aircraft fuel tanks industry while supporting long-term aviation growth.

Major companies operating in the Global Aircraft Fuel Tanks Market include Aerospace Fuel Systems Inc., RTX (Collins Aerospace), Eaton Corporation, Elbit Systems, General Dynamics Corporation, GKN Aerospace, Honeywell International Inc., Lockheed Martin Corporation, Marshall Aerospace and Defence Group, Northstar, Parker Hannifin Corporation, Robertson Fuel Systems LLC, Safran S.A., UTC Aerospace Systems, Continental AG, and Applied Aerospace Structures Corporation. Companies participating in the Aircraft Fuel Tanks Market are adopting several strategic initiatives to strengthen their competitive position and expand global market presence. Leading manufacturers are prioritizing investments in research and development to design lightweight, high-performance fuel tank systems that enhance aircraft efficiency and reliability. Strategic collaborations with aircraft manufacturers and aerospace suppliers are helping companies integrate fuel tank technologies into new aircraft platforms during early design stages. Market participants are also focusing on advanced material development, particularly composite structures, to improve durability and reduce system weight.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Platform trends

- 2.2.3 Material trends

- 2.2.4 End Use trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of regional aviation and business jets

- 3.2.1.2 Growth of military aircraft modernization programs requiring advanced fuel storage

- 3.2.1.3 Increasing production of commercial aircraft

- 3.2.1.4 Rising demand for fuel-efficient and lightweight tank designs using composites

- 3.2.1.5 Technological innovation in fuel management systems and monitoring solutions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and certification costs for advanced tank systems

- 3.2.2.2 Stringent regulatory and safety compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growing retrofit and replacement cycle

- 3.2.3.2 Rising demand from emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 External tanks

- 5.2.1 Conformal tanks

- 5.2.2 Drop tanks

- 5.2.3 Internal

- 5.3 Integral tanks

- 5.3.1 Rigid removable tanks

- 5.3.2 Bladder tanks

- 5.3.3 Tip tanks

- 5.3.4 Auxiliary tanks

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow body aircraft

- 6.2.2 Wide body aircraft

- 6.2.3 Regional jets

- 6.2.4 Commercial helicopters

- 6.3 Military aviation

- 6.3.1 Fighter aircraft

- 6.3.2 Transport aircraft

- 6.3.3 Military helicopters

- 6.3.4 Unmanned Aerial Vehicles (UAVs)

- 6.3.5 Others

- 6.3.6 Business & general aviation

Chapter 7 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Aluminum

- 7.3 Composites

- 7.4 Titanium

- 7.5 Advanced alloys

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Aftermarket

- 8.2.1 Parts replacement

- 8.2.2 MRO

- 8.3 OEM

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 RTX (Collins Aerospace)

- 10.1.2 Eaton Corporation

- 10.1.3 Safran S.A.

- 10.1.4 GKN Aerospace

- 10.1.5 Robertson Fuel Systems LLC

- 10.2 Regional key players

- 10.2.1 Aerospace Fuel Systems Inc.

- 10.2.2 Elbit Systems

- 10.2.3 General Dynamics Corporation

- 10.2.4 Honeywell International Inc.

- 10.2.5 Lockheed Martin Corporation

- 10.2.6 Marshall Aerospace and Defence Group

- 10.2.7 Northstar

- 10.2.8 Parker Hannifin Corporation

- 10.2.9 UTC Aerospace Systems

- 10.3 Niche Players/Disruptors

- 10.3.1 Continental AG

- 10.3.2 Applied Aerospace Structures Corporation