|

시장보고서

상품코드

1998817

열차 통신 게이트웨이 시스템 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Train Communication Gateways System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

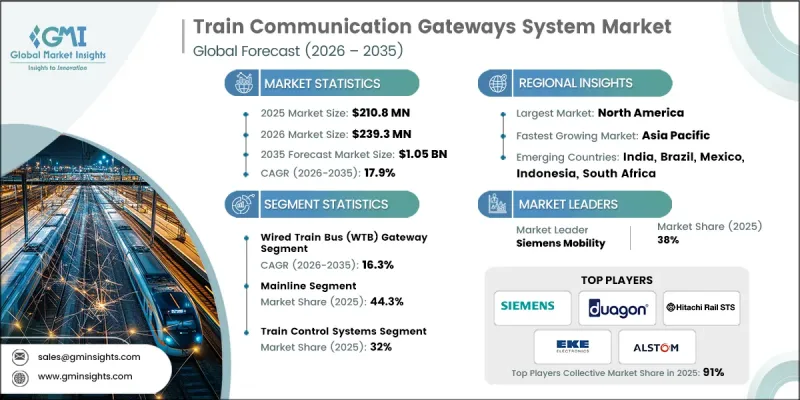

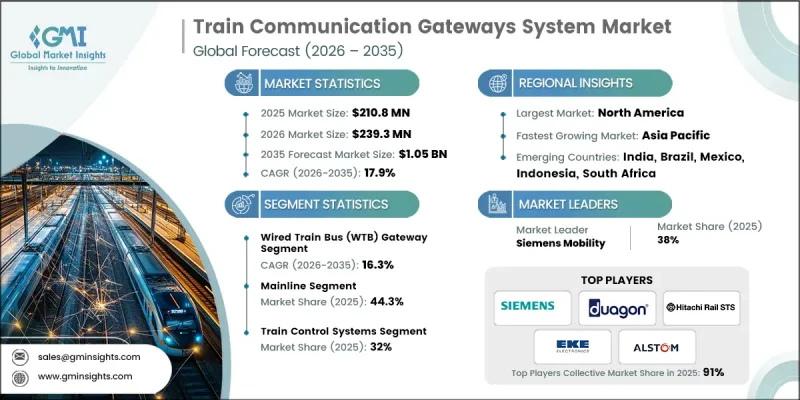

세계의 열차 통신 게이트웨이 시스템 시장은 2025년에 2억 1,080만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 17.9%로 성장하여 10억 5,000만 달러에 달할 것으로 예측됩니다.

철도 사업자가 차량 시스템과 선로 측 시스템 간의 원활한 데이터 교환을 점점 더 중요시함에 따라 열차 통신 게이트웨이 시스템 시장은 강력한 성장세를 보이고 있습니다. 현대의 철도 네트워크는 여러 서브시스템이 상호 연동하고 운영 데이터를 즉시 공유할 수 있는 신뢰할 수 있는 통신 프레임워크를 요구하고 있습니다. 게이트웨이는 제어 시스템, 모니터링 플랫폼 및 차량 탑재 장비 간의 통신을 가능하게 하는 중요한 인터페이스 역할을 합니다. 철도 인프라가 고도화됨에 따라 성능, 안전 및 시스템 진단에 대한 실시간 정보 교환 능력은 서비스의 신뢰성과 운영 효율성을 향상시키는 데 필수적인 요소로 자리 잡았습니다. 교통 당국과 철도 사업자들도 철도 인프라 현대화와 시스템 간 연결성 향상을 위한 디지털 전환(DX) 프로그램에 투자하고 있습니다. 이러한 노력은 자산 관리의 최적화, 운용 계획의 개선, 기술적 문제에 대한 신속한 대응을 지원합니다. 전 세계 철도 네트워크가 지속적으로 확장되고 현대화되는 가운데, 통신 게이트웨이 기술은 차세대 철도 운영을 지원하고 점점 더 복잡해지는 철도 생태계 전반의 원활한 연계를 보장하는 데 있어 핵심적인 역할을 할 것으로 기대됩니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 2억 1,080만 달러 |

| 예측액 | 10억 5,000만 달러 |

| CAGR | 17.9% |

열차 통신 게이트웨이 시스템 시장은 첨단 네트워크 기술 및 연결 장치를 점점 더 많이 도입하는 철도 인프라의 디지털화 진전에 의해 더욱 촉진되고 있습니다. 철도 사업자들은 열차 시스템 전반에 걸쳐 실시간 데이터 모니터링, 예지보전 및 운영 프로세스 자동화를 가능하게 하는 최신 게이트웨이 플랫폼을 도입하고 있습니다. 철도 네트워크 내 연결 기술의 통합으로 사업자는 성능 데이터를 지속적으로 수집하고 분석하여 유지보수 계획을 개선하고 예기치 못한 시스템 장애를 줄일 수 있게 되었습니다. 또한 일부 교통 현대화 이니셔티브는 보다 지능적이고 반응성이 높은 교통 시스템을 구축하기 위해 기존 철도 네트워크 내 통신 능력을 업그레이드하는 데 중점을 두고 있습니다. 최신 게이트웨이 기술은 구식 통신 아키텍처에서 보다 빠른 데이터 전송과 서로 다른 벤더의 장비 간 상호 운용성을 향상시킬 수 있는 첨단 디지털 네트워크 프레임워크로의 전환을 돕습니다.

간선 구간은 2025년 44.3%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 16.6%로 성장할 것으로 전망됩니다. 차량 탑재 장비와 중앙 제어 플랫폼 간의 효율적인 데이터 교환을 지원하기 위해 간선 철도 시스템에서 통신 게이트웨이의 도입이 점점 더 많이 이루어지고 있습니다. 이러한 기술을 통해 운영 파라미터의 실시간 모니터링이 가능하여 시스템의 신뢰성 향상과 서비스 중단을 최소화하는 데 기여합니다. 통신 게이트웨이는 지속적인 진단과 성능 모니터링을 통해 다운타임을 줄이는 예지보전 전략을 지원합니다. 또한, 여러 통신 프로토콜을 통합할 수 있는 능력은 기존 철도 장비와 새로 도입되는 기술과의 호환성을 향상시켜 사업자가 인프라의 전체 구성 요소를 교체하지 않고도 시스템을 업그레이드할 수 있도록 해줍니다.

TCP/IP 부문은 2025년 34%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 15.9%로 성장할 것으로 전망됩니다. TCP/IP 네트워크 프레임워크를 지원하는 통신 게이트웨이는 차량 내 서브시스템 간의 고속 데이터 전송을 가능하게 하고, 사업자가 장비의 성능과 시스템 상태를 실시간으로 모니터링할 수 있도록 합니다. 또한, 이러한 네트워크 기술을 통해 원격 진단, 시스템 업데이트 및 중앙 집중식 데이터 분석을 지원하는 클라우드 기반 플랫폼과의 통합도 가능합니다. TCP/IP 기반 네트워크의 유연성을 통해 철도 사업자는 향후 기술 업그레이드에 대응하면서 여러 벤더의 장비를 쉽게 통합할 수 있습니다. 철도 시스템에서 생성되는 운영 데이터의 양이 증가함에 따라, 이러한 고대역폭 통신 네트워크는 첨단 디지털 철도 용도를 지원하는 데 필요한 확장성을 제공합니다.

미국의 열차 통신 게이트웨이 시스템 시장은 철도 인프라 현대화에 대한 지속적인 투자와 통신 기술 향상에 힘입어 2025년 5,240만 달러에 달했습니다. 이 나라 교통 당국은 운영 효율성과 안전성을 높이는 첨단 디지털 통신 시스템을 통해 철도 네트워크를 업그레이드하는 데 주력하고 있습니다. 최신 게이트웨이 플랫폼이 철도 시스템에 통합되어 차량 내 장비와 제어 센터 간의 연결성을 향상시키기 위해 최신 게이트웨이 플랫폼이 철도 시스템에 통합되어 있습니다. 이러한 시스템은 철도 자산의 수명을 연장하는 데 도움이 되는 실시간 모니터링 및 고급 유지보수 전략도 지원합니다. 또한, 중요 인프라의 사이버 보안에 대한 관심이 높아짐에 따라 기밀성이 높은 운영 데이터를 보호하면서 안정적인 시스템 연결을 보장할 수 있는 보안 통신 게이트웨이 플랫폼의 도입이 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제공별, 2022-2035

제6장 시장 추산 및 예측 : 프로토콜별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 철도별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.24The Global Train Communication Gateways System Market was valued at USD 210.8 million in 2025 and is estimated to grow at a CAGR of 17.9% to reach USD 1.05 billion by 2035.

The train communication gateways system market is experiencing strong growth as railway operators increasingly prioritize seamless data exchange across various onboard and trackside systems. Modern rail networks require reliable communication frameworks that allow multiple subsystems to interact and share operational data instantly. Gateways act as critical interfaces that enable communication between control systems, monitoring platforms, and onboard equipment. As railway infrastructure becomes more advanced, the ability to exchange real-time information related to performance, safety, and system diagnostics has become essential for improving service reliability and operational efficiency. Transportation authorities and railway operators are also investing in digital transformation programs aimed at modernizing rail infrastructure and improving connectivity between systems. These initiatives support better asset management, improved operational planning, and faster response to technical issues. As global rail networks continue to expand and modernize, communication gateway technologies are expected to play a central role in supporting next-generation rail operations and ensuring smooth coordination across increasingly complex rail ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $210.8 Million |

| Forecast Value | $1.05 Billion |

| CAGR | 17.9% |

The train communication gateways system market is further supported by the ongoing digitalization of railway infrastructure, which increasingly incorporates advanced networking technologies and connected devices. Rail operators are adopting modern gateway platforms that enable real-time data monitoring, predictive maintenance, and automated operational processes across train systems. The integration of connected technologies within railway networks allows operators to collect and analyze performance data continuously, improving maintenance planning and reducing unexpected system failures. In addition, several transportation modernization initiatives are focusing on upgrading communication capabilities within existing railway networks to create more intelligent and responsive transportation systems. Modern gateway technologies also support the transition from older communication architectures to advanced digital networking frameworks that allow faster data transmission and improved interoperability between equipment supplied by different vendors.

The mainline segment accounted for 44.3% share in 2025 and is expected to grow at a CAGR of 16.6% between 2026 and 2035. Communication gateways are increasingly deployed in mainline railway systems to support efficient data exchange between onboard equipment and centralized control platforms. These technologies enable real-time monitoring of operational parameters, which helps improve system reliability and minimize service disruptions. By enabling continuous diagnostics and performance monitoring, communication gateways support predictive maintenance strategies that reduce operational downtime. The ability to integrate multiple communication protocols also improves compatibility between existing railway equipment and newly deployed technologies, allowing operators to upgrade their systems without replacing entire infrastructure components.

The TCP/IP segment held a 34% share in 2025 and is projected to grow at a CAGR of 15.9% during 2026-2035. Communication gateways that support TCP/IP networking frameworks enable high-speed data transfer between onboard subsystems, allowing operators to monitor equipment performance and system status in real time. These networking technologies also allow integration with cloud-based platforms that support remote diagnostics, system updates, and centralized data analysis. The flexibility of TCP/IP-based networks makes it easier for railway operators to integrate equipment from multiple vendors while supporting future technology upgrades. As rail systems generate increasing volumes of operational data, these high-bandwidth communication networks provide the scalability needed to support advanced digital railway applications.

United States Train Communication Gateways System Market reached USD 52.4 million in 2025, supported by ongoing investment in railway infrastructure modernization and improved communication technologies. Transportation authorities in the country are focusing on upgrading rail networks with advanced digital communication systems that enhance operational efficiency and safety. Modern gateway platforms are being integrated into rail systems to improve connectivity between onboard equipment and control centers. These systems also support real-time monitoring and advanced maintenance strategies that help extend the lifespan of railway assets. Additionally, growing emphasis on cybersecurity within critical infrastructure has encouraged the deployment of secure communication gateway platforms capable of protecting sensitive operational data while ensuring reliable system connectivity.

Key companies operating in the Global Train Communication Gateways System Market include Siemens Mobility, Alstom, Hitachi Rail, Duagon, EKE-Electronics, SYS TEC Electronic, Quester Tangent, AMIT Transportation, Hasler Rail, and Ingeteam. Companies active in the Train Communication Gateways System Market are adopting several strategies to strengthen their competitive position and expand their technological capabilities. Many organizations are investing heavily in research and development to create advanced gateway platforms capable of supporting higher data throughput, improved cybersecurity, and enhanced system interoperability. Strategic collaborations with railway operators and infrastructure developers help technology providers deliver customized communication solutions tailored to specific rail network requirements. Companies are also expanding their product portfolios by introducing modular gateway architectures that allow easier system upgrades and scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Protocol

- 2.2.4 Application

- 2.2.5 Train

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Real-time train communication demand

- 3.2.1.2 Smart railway system adoption

- 3.2.1.3 Government infrastructure investment

- 3.2.1.4 Integration of IoT/Advanced digital technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation & integration costs

- 3.2.2.2 Cybersecurity & interoperability risks

- 3.2.3 Market opportunities

- 3.2.3.1 High-speed rail expansion projects

- 3.2.3.2 Smart infrastructure & transit networks

- 3.2.3.3 5G-enabled rail communication rollout

- 3.2.3.4 Retrofit & modernization of legacy fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Railroad Administration (FRA)

- 3.4.1.2 Association of American Railroads (AAR) Standards

- 3.4.2 Europe

- 3.4.2.1 European Rail Traffic Management System (ERTMS) / European Train Control System (ETCS)

- 3.4.2.2 IEC 61375

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Industrial Standards (JIS) - Rail

- 3.4.3.2 Chinese Railway Standards (CRS)

- 3.4.4 Latin America

- 3.4.4.1 ABNT NBR (Brazilian Association of Technical Standards - Rail)

- 3.4.4.2 ANTF Standards (Brazilian National Association of Rail Transport)

- 3.4.5 Middle East & Africa

- 3.4.5.1 ESMA Rail Standards (UAE - Emirates Authority for Standardization & Metrology)

- 3.4.5.2 SABS Rail Standards (South African Bureau of Standards - Rail)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by primary research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Trade data analysis (Driven by paid database)

- 3.14.1 Import/export volume & value trends

- 3.14.2 Key trade corridors & tariff impact

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 WTB (Wire Train Bus) Gateways

- 5.2.1 Standard WTB Gateways

- 5.2.2 Safety-Critical WTB Gateways (SIL 2/4)

- 5.3 MVB (Multifunction Vehicle Bus) Gateways

- 5.3.1 Standard MVB Gateways

- 5.3.2 Enhanced MVB Gateways with Ethernet Integration

- 5.4 ECN (Ethernet Consist Network) Gateways

- 5.4.1 Gigabit Ethernet Gateways

- 5.4.2 Industrial Ethernet Gateways

Chapter 6 Market Estimates & Forecast, By Protocol, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 IEC 61375 6.1.1. IEC 61375-1 (WTB & MVB)

- 6.3 TCP/IP 6.2.1. IPv4-Based Gateways

- 6.4 Profinet 6.3.1. Profinet IO Gateways

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger information systems

- 7.3 Security & surveillance systems

- 7.4 Train control systems

- 7.5 Data transfer & communication systems

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Train, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Mainline trains

- 8.2.1 Inter-city trains

- 8.2.2 Long-distance trains

- 8.2.3 High-speed rail

- 8.3 Urban/rapid transit trains

- 8.3.1 Metro systems

- 8.3.2 Subway systems

- 8.3.3 Light rail

- 8.3.4 Commuter rail

- 8.4 Freight trains

- 8.4.1 Bulk freight

- 8.4.2 Intermodal freight

- 8.4.3 Specialized cargo trains

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Advantech

- 10.1.2 Alstom

- 10.1.3 Belden

- 10.1.4 Ericsson

- 10.1.5 GE (Wabtec/GE Transportation)

- 10.1.6 Hitachi Rail

- 10.1.7 Moxa

- 10.1.8 Rockwell Automation

- 10.1.9 Siemens Mobility

- 10.1.10 TTTech

- 10.2 Regional players

- 10.2.1 Duagon

- 10.2.2 EKE-Electronics

- 10.2.3 HaslerRail

- 10.2.4 HollySys

- 10.2.5 Ingeteam

- 10.2.6 Quester Tangent

- 10.3 Emerging players

- 10.3.1 AMiT Transportation

- 10.3.2 ELTEC Elektronik

- 10.3.3 SYS TEC Electronic

- 10.3.4 UniControls