|

시장보고서

상품코드

1998825

해군 함정 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Naval Vessels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

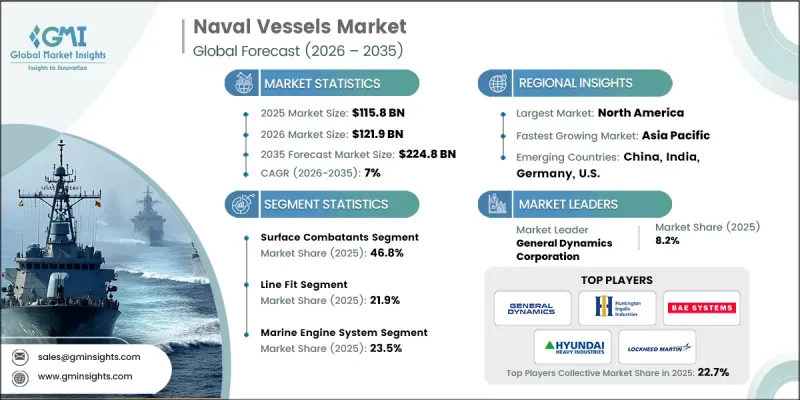

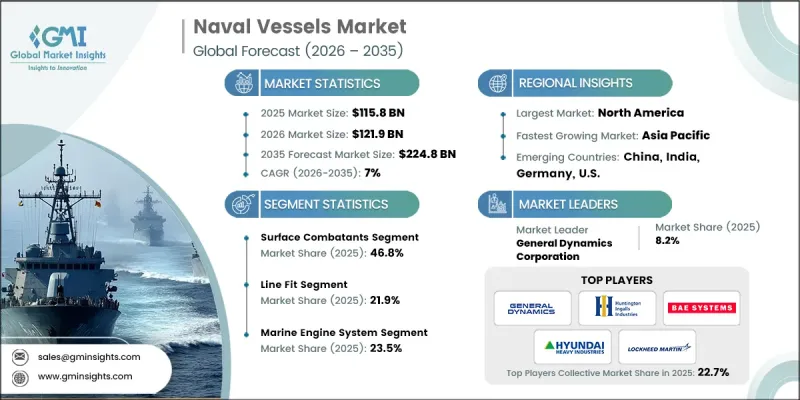

세계의 해군 함정 시장은 2025년에 1,158억 달러로 평가되었고, CAGR 7%로 성장하여 2035년까지 2,248억 달러에 달할 것으로 예측됩니다.

지정학적 긴장의 고조와 해양 안보에 대한 관심 증가가 이러한 성장의 주요 요인으로 작용하고 있습니다. 각국은 영해, 배타적 경제수역 및 국제 무역에 필수적인 중요한 해상 교통로를 보호하기 위해 해군력을 강화하고 있습니다. 해군 작전에 극초음속 무기가 도입됨에 따라 속도, 정확성, 다목적 임무 수행 능력이 향상된 현대식 함대의 필요성이 증가하고 있습니다. 선박 건조 계획에서는 미사일 요격, 감시, 정보 수집 등 다양한 역할을 수행할 수 있도록 모듈식 설계가 점점 더 중요시되고 있습니다. AI, 자율시스템, 무인선박의 도입으로 승무원에 대한 의존도를 낮추면서 운영 효율을 높이고 있습니다. 첨단 능동형 소나 및 소음 감소 시스템을 갖춘 현대식 잠수함을 통해 해군은 경쟁이 치열한 해역 환경에서도 효과적으로 작전을 수행할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 1,158억 달러 |

| 예측 금액 | 2,248억 달러 |

| CAGR | 7% |

2025년 기준, 수상 전투함 부문은 46.8%의 점유율을 차지했습니다. 이러한 성장은 방공, 대잠 작전 및 다목적 전투 능력을 강화하기 위해 설계된 구축함, 호위함, 코르벳함의 조달에 의해 주도되고 있습니다. 이 함정들은 통합 미사일 시스템, 첨단 레이더 및 전투 관리 솔루션을 갖추고 있어 현대 함대의 핵심을 구성하고 있습니다. 함대의 지속적인 현대화와 원양 해군 역량에 대한 투자는 이러한 첨단 플랫폼에 대한 수요를 더욱 촉진하고 있습니다.

리노베이션 부문은 2035년까지 연평균 복합 성장률(CAGR) 7.3%를 나타낼 것으로 예측됩니다. 이러한 확장은 기존 함정을 첨단 레이더 시스템, 미사일 방어 기술, 개선된 추진 시스템, 통신 네트워크로 업그레이드하는 함대 현대화 이니셔티브에 의해 주도되고 있습니다. 개조 프로그램을 통해 해군은 예산을 최적화하고, 함정의 운영 수명을 연장하며, 전면적인 교체 없이도 비용 효율적인 솔루션을 도입할 수 있습니다.

2025년 기준 북미 해군 함정 시장은 43.3%의 점유율을 차지했습니다. 이 지역의 성장은 국방 예산 증가, 전략적 억지력 목표, 차세대 수상 전투함과 잠수함에 대한 투자로 뒷받침되고 있습니다. 미 해군의 모듈식 다목적 플랫폼, 첨단 통합 전투 시스템 및 함대 확장에 대한 강조는 기술적으로 진보된 해군 함정에 대한 수요를 주도하고 있습니다. 항공모함, 구축함, 핵잠수함의 조달 증가와 더불어 기존 함대의 현대화가 진행되면서 세계 시장에서 북미의 입지가 강화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 함정 유형별, 2022-2035

제6장 시장 추산 및 예측 : 시스템별, 2022-2035

제7장 시장 추산 및 예측 : 솔루션별, 2022-2035

제8장 시장 추산 및 예측 : 용도별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.24The Global Naval Vessels Market was valued at USD 115.8 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 224.8 billion by 2035.

Rising geopolitical tensions and increasing focus on maritime security are major drivers of this growth. Nations are strengthening their naval capabilities to safeguard territorial waters, exclusive economic zones, and critical sea lanes essential for international trade. The integration of hypersonic weapons into naval operations has elevated the need for modernized fleets with improved speed, precision, and multi-mission capabilities. Shipbuilding programs are increasingly emphasizing modular designs that allow vessels to perform multiple roles such as missile interception, surveillance, and information collection. AI, autonomous systems, and unmanned vessels are reducing crew dependency while enhancing operational efficiency. Contemporary submarines equipped with advanced active sonar and noise reduction systems enable navies to operate effectively in highly contested maritime environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $115.8 Billion |

| Forecast Value | $224.8 Billion |

| CAGR | 7% |

The surface combatants segment held a 46.8% share in 2025. This growth is fueled by the procurement of destroyers, frigates, and corvettes designed to enhance air defense, anti-submarine operations, and multi-mission combat capabilities. These vessels form the backbone of modern fleets due to their integrated missile systems, advanced radar, and combat management solutions. Continued fleet modernization and investment in blue-water naval capabilities are further driving demand for these advanced platforms.

The retrofit segment is expected to grow at a CAGR of 7.3% during 2035. This expansion is driven by fleet modernization initiatives that upgrade existing vessels with enhanced radar systems, missile defense technologies, improved propulsion, and communication networks. Retrofit programs allow navies to optimize budgets, extend the operational lifespan of ships, and adopt cost-effective solutions without full replacement.

North America Naval Vessels Market held 43.3% share in 2025. Growth in this region is supported by rising defense budgets, strategic deterrence objectives, and investments in next-generation surface combatants and submarines. The U.S. Navy's emphasis on modular multi-mission platforms, advanced integrated combat systems, and fleet expansion is driving demand for technologically advanced naval vessels. Increased procurement of aircraft carriers, destroyers, and nuclear-powered submarines, along with the modernization of existing fleets, is strengthening North America's position in the global market.

Key players operating in the Global Naval Vessels Market include Austal, BAE Systems, Damen Shipyards Group, China State Shipbuilding Corporation, Elbit Systems, Fincantieri S.p.A., General Dynamics Corporation, Huntington Ingalls Industries, Hyundai Heavy Industries, L3Harris Technologies, Lockheed Martin Corporation, Mazagon Dock Shipbuilders, Mitsubishi Heavy Industries, Naval Group, Navantia, Saab AB, Sea Machines Robotics, and Thyssenkrupp Marine Systems. Key strategies adopted by companies in the Global Naval Vessels Market include investing heavily in R&D to develop modular and multi-mission platforms capable of integrating advanced weapons, AI systems, and unmanned technologies. Firms are focusing on retrofitting and upgrading existing fleets to optimize costs while meeting operational requirements. Strategic partnerships with governments, defense agencies, and technology providers help enhance product portfolios and accelerate the adoption of new platforms. Companies are also emphasizing sustainable and energy-efficient ship designs, advanced propulsion systems, and automation technologies to improve operational efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Vessel type trends

- 2.2.2 System trends

- 2.2.3 Solution trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geopolitical tensions and military modernization

- 3.2.1.2 Increasing defense budgets

- 3.2.1.3 Growing demand for submarine-based strategic defense

- 3.2.1.4 Rising focus on maritime security

- 3.2.1.5 Increased focus on naval fleet diversification

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and maintenance costs

- 3.2.2.2 Geopolitical instability and regulatory constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Autonomous and Unmanned Naval Platforms

- 3.2.3.2 Development of Green and Next-Generation Propulsion Technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Vessel Type, 2022 - 2035 (USD Billion & Million Units)

- 5.1 Key trends

- 5.2 Surface Combatants

- 5.2.1 Aircraft Carriers

- 5.2.2 Destroyers

- 5.2.3 Frigates

- 5.2.4 Corvettes

- 5.3 Submarines

- 5.3.1 Attack Submarines (SSN)

- 5.3.2 Ballistic Missile Submarines (SSBN)

- 5.4 Patrol & Support Vessels

- 5.4.1 Offshore Patrol Vessels (OPV)

- 5.4.2 Mine Countermeasure Vessels (MCMV)

- 5.4.3 Amphibious Assault Ships (LHD, LPD)

- 5.4.4 Auxiliary & Support Vessels

Chapter 6 Market Estimates and Forecast, By System, 2022 - 2035 (USD Billion & Million Units)

- 6.1 Key trends

- 6.2 Marine Engine System

- 6.3 Weapon Launch System

- 6.4 Control System

- 6.5 Electrical System

- 6.6 Communication System

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Solution, 2022 - 2035 (USD Billion & Million Units)

- 7.1 Key trends

- 7.2 Line Fit

- 7.3 Retro Fit

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion & Million Units)

- 8.1 Key trends

- 8.2 Combat Operations

- 8.3 Surveillance & Reconnaissance

- 8.4 Coastal Defense & Border Security

- 8.5 Amphibious Operations

- 8.6 Logistics & Support

- 8.7 Humanitarian Assistance & Disaster Relief (HADR)

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Leaders

- 10.1.1 BAE Systems

- 10.1.2 Lockheed Martin Corporation

- 10.1.3 General Dynamics Corporation

- 10.1.4 Huntington Ingalls Industries

- 10.1.5 Naval Group

- 10.1.6 Thyssenkrupp Marine Systems

- 10.1.7 Fincantieri S.p.A.

- 10.1.8 Navantia

- 10.1.9 Damen Shipyards Group

- 10.2 Regional Players

- 10.2.1 Mazagon Dock Shipbuilders

- 10.2.2 Hyundai Heavy Industries

- 10.2.3 Mitsubishi Heavy Industries

- 10.2.4 China State Shipbuilding Corporation

- 10.2.5 Austal

- 10.3 Emerging Players/Disruptors

- 10.3.1 Sea Machines Robotics

- 10.3.2 L3Harris Technologies

- 10.3.3 Saab AB

- 10.3.4 Elbit Systems