|

시장보고서

상품코드

1998829

실험 장비 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Laboratory Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

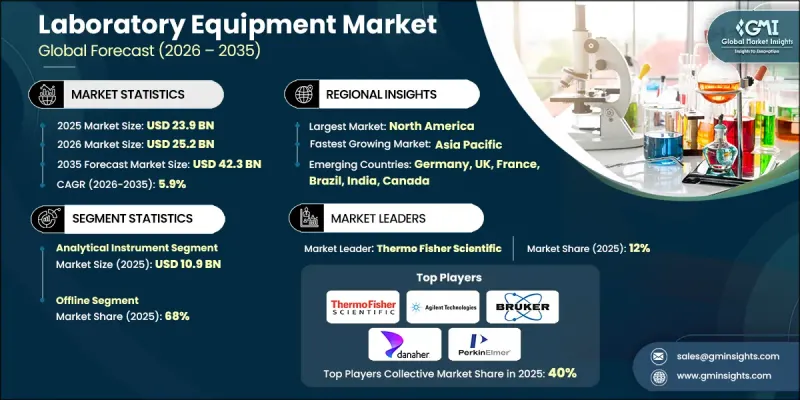

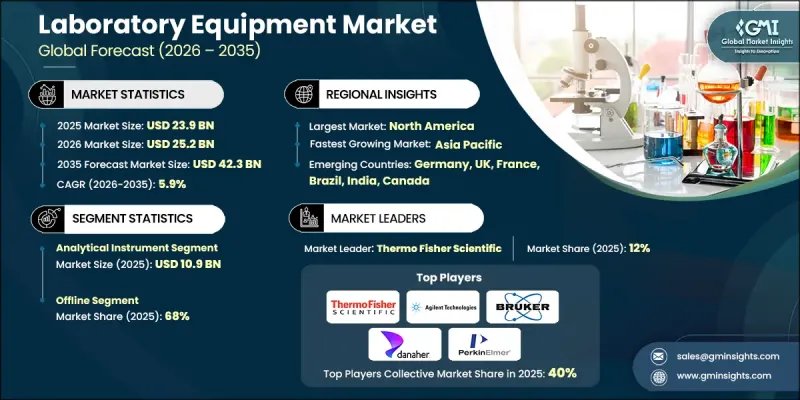

세계의 실험 장비 시장은 2025년에 239억 달러로 평가되며, CAGR 5.9%로 성장하며, 2035년까지 423억 달러에 달할 것으로 추정되고 있습니다.

과학 연구, 특히 의약품 개발, 생명공학 혁신 및 생명과학 탐구에 대한 투자가 증가함에 따라 첨단 실험 장비에 대한 수요가 크게 증가하고 있습니다. 공공 및 민간 기관은 과학적 발견, 치료법 연구 및 생물의학 발전을 위해 막대한 자원을 투입하고 있으며, 이를 위해서는 매우 정확한 분석 결과를 제공할 수 있는 첨단 툴이 필요합니다. 또한 개발도상국의 실험 인프라 확충도 각국이 혁신 주도형 경제 전략을 우선시하는 가운데 장비 수요 증가에 기여하고 있습니다. 동시에 급속한 기술 발전으로 자동화, 로봇 공학 및 인공지능을 활용한 진단 시스템 도입을 통해 실험실의 업무 형태가 재편되고 있습니다. 이러한 기술은 실험실의 업무 효율성 향상, 확장성 개선, 수작업 프로세스에 따른 위험 감소를 실현하는 데 도움을 주고 있습니다. 또한 디지털 모니터링 기술과 커넥티드 디바이스의 통합을 통해 실험실은 여러 연구 환경에서 원격 모니터링, 예지보전 및 고급 데이터 관리를 수행할 수 있습니다. 과학적 혁신에 대한 관심 증가, 실험실 기술의 지속적인 개선, 의료 연구 활동의 활성화가 결합되어 세계 검사 장비 시장을 변화시키고 있으며, 임상, 학술 및 산업 분야의 실험실 수요를 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 239억 달러 |

| 예측액 | 423억 달러 |

| CAGR | 5.9% |

분석 기기 부문은 2025년 109억 달러의 시장 규모를 차지했습니다. 분석 장비는 정확한 측정을 실현하고 첨단 과학 연구를 지원하는 데 매우 중요한 역할을 하므로 이 부문은 계속해서 업계를 주도하고 있습니다. 고정밀 기기는 다양한 과학 분야의 실험실 분석, 실험적 검증 및 규제 준수에 필수적인 요소입니다. 신뢰할 수 있는 분석 데이터를 생성할 수 있는 능력으로 인해 현대 실험실 환경에서 필수적인 툴이 되었습니다. 연구의 정확성과 품질관리에 대한 규제적 기대가 계속 높아지는 가운데, 고급 분석 장비의 중요성은 실험실 장비 시장의 성장에 있으며, 여전히 중심적인 위치를 차지하고 있습니다.

2025년 기준 오프라인 유통 부문은 68%의 점유율을 차지했습니다. 전통적 유통 네트워크는 연구소에 기술 전문 지식과 전문적인 고객 지원을 직접 제공하므로 여전히 매우 중요한 역할을 하고 있습니다. 공급업체와 유통업체는 장비의 납품, 설치 프로세스 관리 및 복잡한 실험실 장비의 유지보수 서비스 제공에 있으며, 매우 중요한 역할을 담당하고 있습니다. 과학 장비는 고도로 전문적이고 고비용이기 때문에 연구기관, 의료기관 및 산업 실험실에서는 신뢰할 수 있는 서비스 계약과 기술 지원이 보장되는 오프라인 채널을 통한 구매를 선호하는 경향이 있습니다. 이러한 접근 방식을 통해 고객은 설치, 교정, 수리 서비스 및 맞춤형 장비 구성에 대한 전문적인 안내를 받을 수 있습니다.

미국 실험실 장비 시장은 탄탄한 연구 생태계, 디지털 실험실 기술의 광범위한 도입, 효율적인 실험실 워크플로우에 대한 강력한 수요에 힘입어 2025년 69.3%의 점유율을 차지했습니다. 미국의 실험실 장비 산업은 첨단 자동화, 정밀도를 중시하는 계측 장비, 엄격한 규정 준수 기준이 특징입니다. 생명공학, 제약, 진단 연구 분야의 지속적인 수요는 실험실 기술 및 워크플로우 최적화 시스템의 끊임없는 혁신을 촉진하고 있습니다. 또한 이 지역은 첨단 물류 네트워크, 전문 기술 지원 서비스, 복잡한 실험실 업무를 관리할 수 있는 고도로 숙련된 인력을 포함한 탄탄한 인프라의 혜택을 누리고 있습니다. 이러한 요인들로 인해 민관 연구시설은 실험실의 기능을 신속하게 도입, 유지, 확장할 수 있게 되었습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 장비 유형별, 2021-2034

제6장 시장 추산·예측 : 자동화 레벨별, 2021-2034

제7장 시장 추산·예측 : 용도별, 2021-2034

제8장 시장 추산·예측 : 최종 용도 산업별, 2021-2034

제9장 시장 추산·예측 : 유통 채널별, 2021-2034

제10장 시장 추산·예측 : 지역별, 2021-2034

제11장 기업 개요

KSA 26.04.20The Global Laboratory Equipment Market was valued at USD 23.9 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 42.3 billion by 2035.

Increasing investment in scientific research, particularly in pharmaceutical development, biotechnology innovation, and life science exploration, is creating significant demand for advanced laboratory equipment. Public institutions and private organizations are allocating substantial resources toward scientific discovery, therapeutic research, and biomedical advancements, which require sophisticated tools capable of delivering highly accurate analytical results. The expansion of laboratory infrastructure in developing regions is also contributing to rising equipment demand as countries prioritize innovation-driven economic strategies. At the same time, rapid technological advancements are reshaping laboratory operations through the adoption of automation, robotics, and artificial intelligence-enabled diagnostic systems. These technologies are helping laboratories achieve greater operational efficiency, improved scalability, and reduced risks associated with manual processes. Additionally, the integration of digital monitoring technologies and connected devices allows laboratories to perform remote monitoring, predictive maintenance, and advanced data management across multiple research environments. Growing attention toward scientific innovation, continuous improvements in laboratory technology, and increasing healthcare research activities are collectively transforming the global laboratory equipment market while strengthening demand across clinical, academic, and industrial laboratories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.9 Billion |

| Forecast Value | $42.3 Billion |

| CAGR | 5.9% |

The analytical instrument segment accounted for USD 10.9 billion in 2025. This segment continues to dominate the industry because analytical instruments play a critical role in delivering accurate measurements and supporting advanced scientific research. High-precision instruments are essential for laboratory analysis, experimental validation, and regulatory compliance across numerous scientific fields. Their ability to produce reliable analytical data makes them fundamental tools in modern laboratory environments. As regulatory expectations surrounding research accuracy and quality control continue to increase, the importance of advanced analytical instruments remains central to the growth of the laboratory equipment market.

The offline distribution segment held 68% share in 2025. Traditional distribution networks remain highly relevant because they provide laboratories with direct access to technical expertise and specialized customer support. Suppliers and distributors play a vital role in delivering equipment, managing installation processes, and providing maintenance services for complex laboratory instruments. Due to the sophisticated nature and high cost associated with scientific equipment, research institutions, healthcare organizations, and industrial laboratories often prefer purchasing through offline channels that ensure dependable service agreements and technical assistance. This approach allows customers to access professional guidance for installation, calibration, repair services, and customized equipment configuration.

United States Laboratory Equipment Market held 69.3% share in 2025, supported by a well-established research ecosystem, extensive adoption of digital laboratory technologies, and strong demand for efficient laboratory workflows. The laboratory equipment industry in the United States is characterized by a high level of automation, precision-driven instrumentation, and strict compliance standards. Continuous demand from the biotechnology, pharmaceutical, and diagnostic research sectors is encouraging ongoing innovation in laboratory technologies and workflow optimization systems. Additionally, the region benefits from a robust infrastructure that includes advanced logistics networks, specialized technical support services, and a highly skilled workforce capable of managing complex laboratory operations. These factors enable research facilities across both public and private sectors to rapidly deploy, maintain, and scale laboratory capabilities.

Major companies operating in the Global Laboratory Equipment Market include 3M, Abbott Laboratories, Agilent Technologies, Atom Scientific Industries, Beckton Dickinson, Bruker Corporation, Danaher Corporation, GEA, Labman Scientific Instruments, PerkinElmer, Roche, Sartorius, Siemens Healthineers, Thermo Fisher Scientific, and Waters Corporation. Companies competing in the Global Laboratory Equipment Market are focusing on several strategic initiatives to strengthen their competitive position and expand their global reach. Many organizations are investing heavily in research and development to introduce advanced laboratory technologies that enhance precision, automation, and data integration capabilities. Product innovation centered on intelligent laboratory systems, connected instruments, and digital workflow management tools is becoming a key competitive differentiator. Leading companies are also expanding manufacturing capacity and strengthening global distribution networks to improve product accessibility across emerging and established markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation (Driven by Primary Research)

- 1.7.1 Primary sources

- 1.7.2 Expert Validation Protocol

- 1.7.3 Region-Specific Primary Interviews

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.1.1 North America

- 2.2.1.2 Europe

- 2.2.1.3 Asia-Pacific

- 2.2.1.4 Middle East and Africa

- 2.2.1.5 Latin America

- 2.2.2 Equipment type

- 2.2.3 Automation level

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Distribution channel

- 2.2.1 Regional

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising R&D activities

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing prevalence of chronic diseases

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital investment

- 3.2.2.2 Regulatory and compliance challenges

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.6.3 By region

- 3.6.4 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Patent Landscape (Driven by Primary Research)

- 3.8.1 Patent Filing Trends by Technology Area

- 3.8.2 Geographic Distribution of Patents

- 3.8.3 Key Patent Holders & IP Strategy Analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade Data Analysis (Driven by Primary Research)

- 3.11.1 Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.11.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11.3 Trade Policy Implications & Localization Trends

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Analytical instruments

- 5.2.1 Spectrometers (UV-Vis, IR, NMR, mass spectrometers)

- 5.2.2 Chromatography equipment (HPLC, GC)

- 5.2.3 Microscopes (optical, electron)

- 5.2.4 pH meters & conductivity meters

- 5.2.5 Balances & weighing equipment

- 5.3 Laboratory instruments

- 5.3.1 Incubators & ovens

- 5.3.2 Centrifuges

- 5.3.3 Water purification systems

- 5.3.4 Autoclaves & sterilizers

- 5.3.5 Refrigerators & freezers

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Automation Level, 2021 - 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Automatic

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Medical & clinical laboratories

- 7.3 Pharmaceutical & biotechnology laboratories

- 7.4 Food & beverage testing

- 7.5 Chemical & material testing

- 7.6 Academic & educational laboratories

- 7.7 Others (academic/research institutions, environmental)

Chapter 8 Market Estimates and Forecast, By End-Use Industry, 2021 - 2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Healthcare

- 8.3 Food and beverages

- 8.4 Pharmaceuticals

- 8.5 Academic/research institutions

- 8.6 Chemicals

- 8.7 Others (Veterinary, etc.)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Abbott Laboratories

- 11.3 Agilent Technologies

- 11.4 Atom Scientific Industries

- 11.5 Beckton Dickinson

- 11.6 Bruker Corporation

- 11.7 Danaher Corporation

- 11.8 GEA

- 11.9 Labman Scientific Instruments

- 11.10 PerkinElmer

- 11.11 Roche

- 11.12 Sartorius

- 11.13 Siemens Healthineers

- 11.14 Thermo Fisher Scientific

- 11.15 Waters Corporation