|

시장보고서

상품코드

1998834

스포츠 의학 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Sports Medicine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

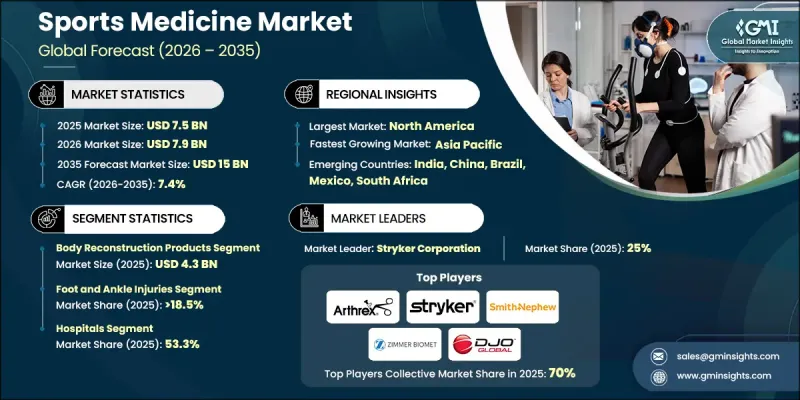

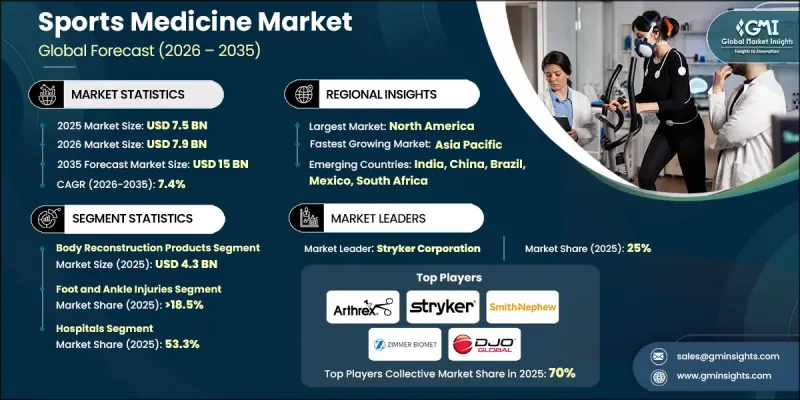

세계의 스포츠 의학 시장은 2025년에 75억 달러로 평가되며, CAGR 7.4%로 성장하며, 2035년까지 150억 달러에 달할 것으로 추정되고 있습니다.

이 시장의 성장은 전 세계 스포츠 부상 증가와 더불어 임플란트, 웨어러블 기기, 최소침습 수술의 기술 발전에 힘입어 성장세를 보이고 있습니다. 의료진은 기존 수술에 비해 빠른 회복, 통증 감소, 낮은 합병증 발생률 등의 장점으로 인해 관절경 수술 및 기타 최소 침습적 기술을 점점 더 많이 채택하고 있습니다. 스포츠 의학은 의료기기, 임플란트, 재활 장비, 성능 모니터링 툴 등 스포츠 관련 부상의 예방, 진단, 치료를 목적으로 하는 제품 및 서비스를 포괄합니다. 이 시장은 스포츠 참여자 증가, 피트니스에 대한 인식 증가, 부상 관리 기술의 혁신으로 인해 더욱 성장하고 있습니다. 생체적합성 소재, 3D 프린팅, 스마트 코팅을 적용한 첨단 임플란트는 치유를 촉진하는 동시에 감염 위험을 최소화합니다. 센서와 스마트 밴드와 같은 웨어러블 기기는 근육 활동, 생체역학, 스트레스 수준을 실시간으로 모니터링하여 개인별 맞춤 치료와 회복 결과를 개선할 수 있도록 돕습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 75억 달러 |

| 예측액 | 150억 달러 |

| CAGR | 7.4% |

2025년 신체 재건 제품 부문은 43억 달러의 시장 규모를 기록했습니다. 이러한 제품에는 스포츠 부상 후 손상된 뼈, 관절 및 조직을 복구, 대체 또는 재건하도록 설계된 의료기기 및 생물제제가 포함됩니다. 이는 이동성, 안정성, 기능성을 회복하는 데 매우 중요한 역할을 하며, 운동선수가 더 빨리 활동으로 복귀할 수 있도록 도와줍니다. 스포츠 관련 부상 증가와 첨단 치료법에 대한 수요 증가는 신체 재건 제품의 보급을 촉진하고 있습니다. 3D 프린팅 임플란트, 생체흡수성 재료, 재생의료용 바이오로직스 등의 혁신 기술은 수술의 성과를 높이고 회복 기간을 단축하며 환자의 만족도를 높입니다.

2025년 발 및 발목 손상 부문은 18.5%의 점유율을 차지했습니다. 이러한 부위의 손상에는 골절, 염좌, 힘줄 파열, 피로 골절 등이 포함되며, 이는 이동성과 운동 능력에 심각한 영향을 미칩니다. 고부하 활동, 과도한 사용, 부적절한 신발 착용 등이 이러한 손상의 다발적 요인으로 작용합니다. 환자와 의료진이 조기 개입과 효과적인 회복 전략을 우선시하는 가운데, 손상 예방, 진단 및 재활 기술의 지속적인 발전이 이 부문 시장 성장을 지원하고 있습니다.

2025년 북미 스포츠 의학 시장은 36.4%의 점유율을 차지했습니다. 이 지역 시장 성장은 첨단 의료 인프라, 기술 혁신, 스포츠 참여자 증가에 의해 주도되고 있습니다. 청소년과 성인의 골절, 인대파열, 뇌진탕, 과사용 증후군 등의 부상 발생률이 증가함에 따라 고급 치료법, 재활 서비스, 예방 의료에 대한 수요가 증가하고 있습니다. 이 지역은 우수한 의료시설, 숙련된 의료진, 그리고 안전한 스포츠 실천을 장려하는 인식 개선 캠페인이 결합되어 그 혜택을 누리고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035

제6장 시장 추산·예측 : 부상 유형별, 2022-2035

제7장 시장 추산·예측 : 최종 용도별, 2022-2035

제8장 시장 추산·예측 : 지역별, 2022-2035

제9장 기업 개요

KSA 26.04.20The Global Sports Medicine Market was valued at USD 7.5 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 15 billion by 2035.

The market's growth is fueled by the rising prevalence of sports injuries worldwide, coupled with technological advancements in implants, wearable devices, and minimally invasive surgical procedures. Healthcare providers are increasingly adopting arthroscopic and other minimally invasive techniques due to their advantages, including faster recovery, reduced pain, and lower complication rates compared to traditional surgeries. Sports medicine encompasses products and services designed to prevent, diagnose, and treat sports-related injuries, including medical devices, implants, rehabilitation equipment, and performance monitoring tools. The market is further driven by growing sports participation, heightened fitness awareness, and innovations in injury management technologies. Advanced implants using biocompatible materials, 3D printing, and smart coatings accelerate healing while minimizing infection risks. Wearable devices such as sensors and smart bands provide real-time monitoring of muscle activity, biomechanics, and stress levels, supporting personalized treatment and enhanced recovery outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.5 Billion |

| Forecast Value | $15 Billion |

| CAGR | 7.4% |

The body reconstruction products segment generated USD 4.3 billion in 2025. These products include medical devices and biologics designed to repair, replace, or reconstruct damaged bones, joints, and tissues following sports injuries. They play a vital role in restoring mobility, stability, and functionality, enabling athletes to return to their activities faster. Growing sports-related injuries and demand for advanced treatment options drive the adoption of body reconstruction products. Innovations like 3D-printed implants, bioresorbable materials, and regenerative biologics enhance surgical outcomes, reduce recovery time, and improve patient satisfaction.

The foot and ankle injuries segment generated 18.5% share in 2025. Injuries in these areas include fractures, sprains, tendon tears, and stress fractures, which significantly impact mobility and athletic performance. High-impact activities, overuse, and improper footwear contribute to their prevalence. Continuous advancements in injury prevention, diagnostics, and rehabilitation technologies support market growth in this segment, as patients and healthcare providers prioritize early intervention and effective recovery strategies.

North America Sports Medicine Market held a 36.4% share in 2025. Market growth in the region is driven by advanced healthcare infrastructure, technological innovation, and rising sports participation. Increasing incidences of injuries such as fractures, ligament tears, concussions, and overuse conditions among youth and adults have created a strong demand for advanced treatment options, rehabilitation services, and preventive care. The region benefits from a combination of highly equipped medical facilities, skilled healthcare professionals, and awareness campaigns promoting safe athletic practices.

Key companies operating in the Global Sports Medicine Market include Wright Medical Technology, DJO Global, Arthrex, Inc., Johnson & Johnson, Performance Health International Limited, Zimmer Biomet, Stryker, CONMED Corporation, Anika Therapeutics, Inc., Otto Bock Healthcare, Smith & Nephew Plc, Muller Sports, Inc., Creamer Product, Inc., KARL STORZ, Breg, Inc., and Bauerfeind AG. Companies in the Sports Medicine Market are expanding their presence by investing in research and development of innovative implants, wearable devices, and regenerative biologics. Manufacturers are forming strategic partnerships with hospitals, clinics, and sports organizations to integrate products into treatment and rehabilitation programs. Geographic expansion into emerging markets allows access to a growing base of athletes and recreational participants. Firms are also focusing on minimally invasive solutions to improve recovery outcomes and patient satisfaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Injury type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of sports injuries globally

- 3.2.1.2 Technological advancements in implants and wearable devices

- 3.2.1.3 Growing demand for minimal invasive surgeries and rising number of sports medical centres

- 3.2.1.4 Increasing awareness regarding physical fitness and sports activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of trained healthcare professional in developing countries

- 3.2.2.2 Inflated cost of sports medicine

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in telehealth and remote rehabilitation services, enabling hybrid care models.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2025

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Body reconstruction products

- 5.2.1 Orthopedic implants

- 5.2.2 Fracture and ligament repair products

- 5.2.3 Arthroscopy devices

- 5.2.4 Soft tissue repair products

- 5.2.5 Prosthetics

- 5.2.6 Orthobiologics

- 5.3 Body support & recovery

- 5.3.1 Braces and supports

- 5.3.2 Compression clothing

- 5.3.3 Physiotherapy equipment

- 5.3.4 Thermal therapy

- 5.3.5 Electrostimulation

- 5.3.6 Other body support & recovery products

- 5.4 Accessories

- 5.4.1 Bandages

- 5.4.2 Tapes

- 5.4.3 Disinfectants

- 5.4.4 Wraps

- 5.4.5 Other accessories

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Injury Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Knee injuries

- 6.3 Shoulder injuries

- 6.4 Foot and ankle injuries

- 6.5 Back and spine injuries

- 6.6 Hip and groin injuries

- 6.7 Other injuries

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Physiotherapy centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Stryker

- 9.2 Arthrex, Inc.

- 9.3 Wright Medical Technology

- 9.4 Otto Bock Healthcare

- 9.5 Zimmer Biomet

- 9.6 Smith & Nephew Plc

- 9.7 Breg, Inc.

- 9.8 Muller Sports, Inc.

- 9.9 RTI Surgical

- 9.10 Performance Health International Limited

- 9.11 KARL STORZ

- 9.12 Bauerfeind AG

- 9.13 CONMED Corporation

- 9.14 Johnson & Johnson

- 9.15 Ossur Corporate

- 9.16 Creamer Product, Inc.

- 9.17 DJO Global

- 9.18 Anika Therapeutics, Inc.