|

시장보고서

상품코드

1998838

인플루엔자 백신 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Influenza Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

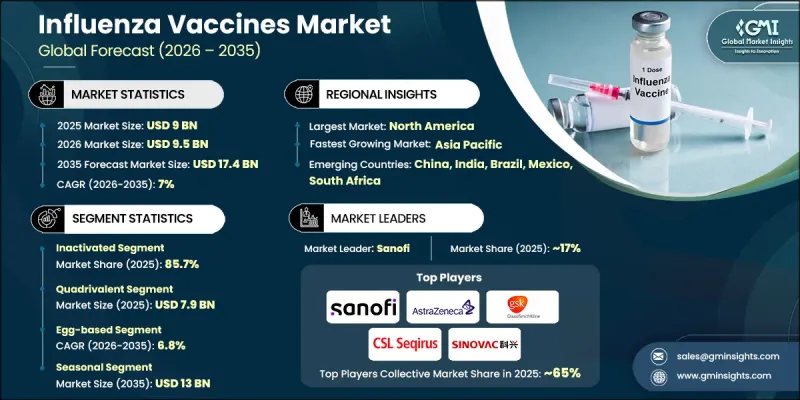

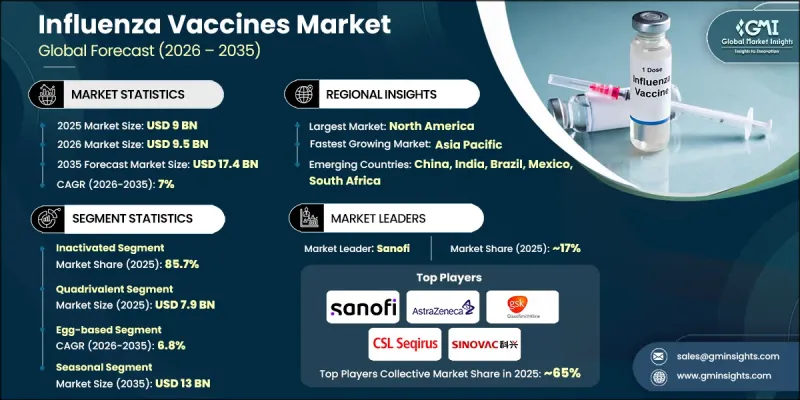

세계의 인플루엔자 백신 시장은 2025년에 90억 달러로 평가되며, CAGR 7%로 성장하며, 2035년까지 174억 달러에 달할 것으로 추정되고 있습니다.

독감 백신 시장이란 유행하는 독감 바이러스로부터 사람들을 보호하기 위한 백신의 개발, 제조, 유통에 특화된 세계 생태계를 말합니다. 이 백신은 감염률 감소, 질병의 중증도 감소, 특히 합병증 위험이 높은 사람들을 중심으로 지역사회 차원의 면역력을 강화하는 것을 목표로 하고 있습니다. 업계 전반에 걸쳐 면역 보호 기능을 향상시키고 변이하는 바이러스 균주에 대응하기 위해 개발된 여러 면역화 플랫폼을 포함한 다양한 백신 기술이 활용되고 있습니다. 주목할 만한 업계 동향으로는 생산 효율성과 면역원성 향상을 위한 첨단 백신 개발 기술로의 전환을 들 수 있습니다. 전통적 생산 방식은 항원 적합성 향상, 생산량 증가, 생산 일정의 유연성을 가능하게 하는 최신 제조 플랫폼에 의해 점점 더 많이 지원되고 있습니다. 정부 주도의 예방접종 구상과 기관별 조달 프로그램도 장기적인 수요 증가를 지원하고 있습니다. 연례 예방접종을 장려하는 공중보건 정책은 국가 비축 프로그램 및 의료보험 적용 범위 확대와 함께 지속적인 예방접종을 장려하고 있습니다. 이러한 정책 프레임워크는 백신의 효능과 생산 일정에 대한 오랜 숙제를 해결하면서 R&D 및 제조 역량에 대한 투자를 지속적으로 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 90억 달러 |

| 예측액 | 174억 달러 |

| CAGR | 7% |

불활화 백신 부문은 2025년 85.7%의 점유율을 차지하며, 2026-2035년 연평균 복합 성장률(CAGR) 6.9%를 나타낼 것으로 예측됩니다. 이 부문은 안전성이 입증된 실적과 다양한 인구층에 대한 폭넓은 적용 가능성으로 선도적인 위치를 유지하고 있습니다. 불활성화 독감 백신은 복제 가능한 바이러스 입자를 도입하지 않고 방어 면역 반응을 유도하므로 예방접종 프로그램에 널리 사용되고 있습니다. 안전성 프로파일로 인해 다양한 건강 상태를 가진 개인을 포함한 광범위한 계층에서 사용하기에 적합하며, 이는 각국의 백신 접종 전략에서 광범위한 채택을 촉진하고 있습니다.

4가 백신 부문은 2025년 79억 달러의 시장 규모를 기록했습니다. 이 백신은 단일 제형으로 여러 유행성 독감 바이러스 균주에 대한 광범위한 방어력을 제공하므로 이 부문을 지배하고 있습니다. 더 광범위한 균주 커버리지는 백신 구성과 계절적 바이러스 패턴의 불일치로 인한 위험을 줄이고 예방 접종 캠페인의 전반적인 효과를 향상시킵니다. 이러한 확장된 방어 능력으로 인해 4가 백신은 대규모 예방접종 구상에서 우선적으로 선택되는 백신으로 자리 잡았습니다. 또한 계절적 변동에 대응할 수 있는 백신의 특성은 독감 유행 기간 중 임상 결과 개선, 입원율 감소, 공중보건 보호 강화에 기여하고 있습니다.

2025년 북미 독감 백신 시장은 44.9%의 점유율을 차지했습니다. 이 지역은 첨단인 의료 인프라, 지원적인 규제 프레임워크, 예방 의료에 대한 높은 시민의식을 바탕으로 탄탄한 입지를 유지하고 있습니다. 지역 시장에서 미국의 선도적 지위는 확립된 질병 감시 시스템과 정기적인 백신 접종을 장려하는 의료 정책으로 더욱 강화되고 있습니다. 다양한 인구집단을 대상으로 매년 독감 백신 접종을 장려하는 공중보건 프로그램은 지속적으로 견고한 수요를 지원하고 있으며, 소아, 성인 및 고위험군 시장에서의 지속적인 시장 확대에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 백신 유형별, 2022-2035

제6장 시장 추산·예측 : 적응증별, 2022-2035

제7장 시장 추산·예측 : 기술별, 2022-2035

제8장 시장 추산·예측 : 인플루엔자 유형별, 2022-2035

제9장 시장 추산·예측 : 연령층별, 2022-2035

제10장 시장 추산·예측 : 투여 경로별, 2022-2035

제11장 시장 추산·예측 : 최종 용도별, 2022-2035

제12장 시장 추산·예측 : 지역별, 2022-2035

제13장 기업 개요

KSA 26.04.20The Global Influenza Vaccines Market was valued at USD 9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 17.4 billion by 2035.

The influenza vaccines market represents the global ecosystem dedicated to the development, production, and distribution of vaccines that help protect populations from circulating influenza viruses. These vaccines are designed to lower infection rates, minimize the severity of illness, and strengthen community-level immunity, particularly among individuals who are more vulnerable to complications. Various vaccine technologies are utilized across the industry, including multiple immunization platforms developed to improve immune protection and respond to evolving viral strains. A notable industry trend involves the transition toward advanced vaccine development technologies aimed at improving production efficiency and immunogenic performance. Traditional production methods are increasingly supported by modern manufacturing platforms that enable improved antigen matching, higher output levels, and more flexible production timelines. Government-backed immunization initiatives and institutional procurement programs are also supporting long-term demand growth. Public health policies that promote annual vaccination, combined with national stockpiling programs and broader healthcare coverage, are encouraging consistent vaccine uptake. These policy frameworks continue to stimulate investment in research, development, and manufacturing capacity while addressing longstanding challenges related to vaccine effectiveness and production timelines.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9 Billion |

| Forecast Value | $17.4 Billion |

| CAGR | 7% |

The inactivated segment held 85.7% share in 2025 and is projected to grow at a CAGR of 6.9% throughout 2026-2035. This segment maintains a leading position due to its well-established safety record and broad applicability across diverse population groups. Inactivated influenza vaccines remain widely utilized in immunization programs because they generate protective immune responses without introducing replicating viral particles. Their safety profile makes them suitable for use across a wide demographic range, including individuals with varying health conditions, which reinforces their widespread adoption within national vaccination strategies.

The quadrivalent vaccine segment generated USD 7.9 billion in 2025. These vaccines dominate the segment because they provide expanded protection against multiple circulating influenza virus strains within a single formulation. Broader strain coverage helps reduce the risk of mismatch between vaccine composition and seasonal viral patterns, which improves the overall effectiveness of vaccination campaigns. This expanded protective capability has made quadrivalent vaccines a preferred choice for large-scale immunization initiatives. In addition, the ability of these vaccines to address seasonal variability contributes to improved clinical outcomes, lower hospitalization rates, and stronger public health protection during influenza seasons.

North America Influenza Vaccines Market accounted for 44.9% share in 2025. The region maintains its strong position due to its advanced healthcare infrastructure, supportive regulatory frameworks, and high public awareness regarding preventive healthcare practices. The leadership of United States within the regional market is reinforced by well-established disease surveillance systems and healthcare policies that encourage routine vaccination. Public health programs that promote annual influenza vaccination across broad population groups continue to support strong demand, contributing to consistent market expansion across pediatric, adult, and high-risk populations.

Key participants operating in the Global Influenza Vaccines Market include Sanofi, GlaxoSmithKline, AstraZeneca, CSL Seqirus, Serum Institute of India, Sinovac Biotech, SK Bioscience, Viatris, GC Biopharma, Bharat Biotech, Cadila Healthcare (Zydus Lifesciences), Denka Seiken, and Bio Farma. Companies operating in the Global Influenza Vaccines Market are implementing several strategies to strengthen their competitive presence and expand market share. Leading vaccine manufacturers are investing heavily in research and development to advance next-generation vaccine platforms that offer improved immune responses and faster production capabilities. Strategic partnerships with government health agencies and international health organizations are helping companies secure large procurement contracts and strengthen supply networks. Firms are also expanding manufacturing capacity and adopting advanced production technologies to support large-scale vaccination programs. In addition, companies are increasing their focus on global distribution infrastructure and regional market expansion to improve vaccine accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Vaccine type trends

- 2.2.3 Indication trends

- 2.2.4 Flu type trends

- 2.2.5 Age group trends

- 2.2.6 Route of administration trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of influenza

- 3.2.1.2 Rising government health initiatives and immunization programs

- 3.2.1.3 Advancements in vaccine technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with vaccine development

- 3.2.2.2 Longer vaccine production timelines

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of universal and broader-spectrum influenza vaccines

- 3.2.3.2 Growth in pediatric and maternal immunization programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis

- 3.6 Patent analysis

- 3.7 Technology and innovation landscape (Driven by Primary Research)

- 3.7.1 Current technologies

- 3.7.2 Emerging technologies

- 3.8 Future market trends (Driven by Primary Research)

- 3.9 Impact of AI and generative AI on the market

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Inactivated

- 5.3 Live attenuated

- 5.4 Recombinant

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Quadrivalent

- 6.3 Trivalent

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Egg-based

- 7.3 Cell-based

- 7.4 Recombinant technology

Chapter 8 Market Estimates and Forecast, By Flu Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Seasonal

- 8.3 Pandemic

Chapter 9 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Pediatric

- 9.3 Adults

Chapter 10 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Injection

- 10.3 Nasal spray

Chapter 11 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 Hospitals

- 11.2.1 Public

- 11.2.2 Private

- 11.3 Clinics

- 11.4 Other end users

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 AstraZeneca

- 13.2 Bharat Biotech

- 13.3 Cadila Healthcare (Zydus Lifesciences)

- 13.4 CSL Seqirus

- 13.5 Denka Seiken

- 13.6 GlaxoSmithKline

- 13.7 Sanofi

- 13.8 Serum Institute of India

- 13.9 Sinovac Biotech

- 13.10 SK bioscience

- 13.11 Viatris

- 13.12 GC Biopharma

- 13.13 Bio Farma