|

시장보고서

상품코드

1998841

산업용 레이저 시스템 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Laser Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

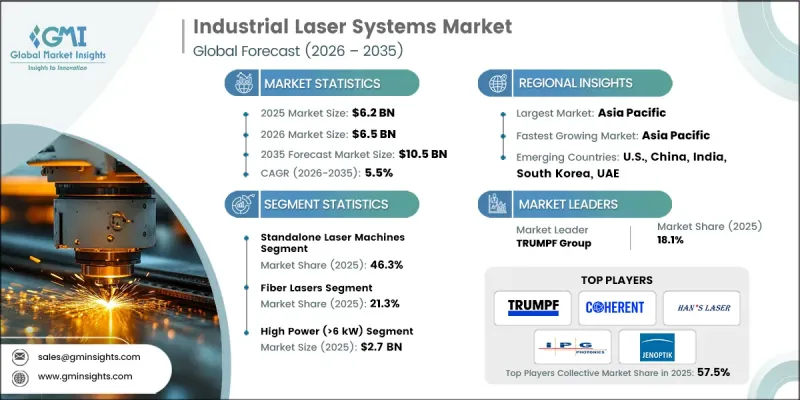

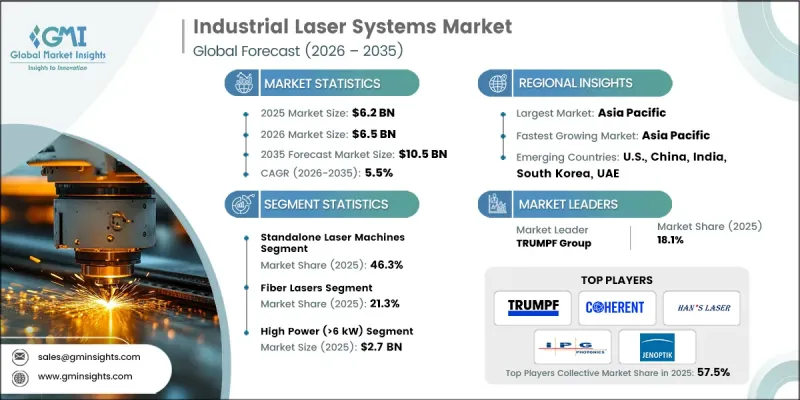

세계의 산업용 레이저 시스템 시장은 2025년에 62억 달러로 평가되며, CAGR 5.5%로 성장하며, 2035년에는 105억 달러에 달할 것으로 추정되고 있습니다.

이 시장은 정밀 제조, 특히 정밀도와 효율성이 요구되는 고부가가치 응용 분야에서 레이저 기술 채택이 확대되면서 성장하고 있습니다. 전기자동차 배터리 생산의 레이저 용접, 전자기기 제조의 레이저 마킹, 반도체 미세화를 위한 초고속 레이저 미세 가공, 항공우주 및 산업용 부품의 레이저 지원 적층제조에 대한 수요 증가로 인해 산업이 확대되고 있습니다. 파이버 레이저, 초고속 레이저 및 로봇 통합의 기술 발전으로 제조업체는 생산 시간을 단축하고 품질, 신뢰성 및 에너지 효율을 향상시키면서 생산 시간을 단축할 수 있게 되었습니다. 이러한 요인들은 자동화 및 인더스트리 4.0 프로세스에 대한 지속적인 투자와 함께 여러 산업 분야에서 강력한 성장 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 62억 달러 |

| 예측액 | 105억 달러 |

| CAGR | 5.5% |

산업용 레이저 시스템 시장은 특히 배터리 및 전자제품 제조에서 정밀 레이저 용접에 대한 수요 증가에 힘입어 성장하고 있습니다. 레이저 용접은 열 변형을 최소화하면서 전도성 재료를 고속으로 접합할 수 있으며, 견고한 구조적 무결성과 전기적 성능 향상을 보장합니다. 동시에 초고속 레이저 미세 가공이 반도체 제조에서 주목받고 있으며, 열 손상을 일으키지 않고 고정밀 웨이퍼 절단, 마이크로 비아 가공 및 박막 구조 형성을 가능하게 합니다. 또한 레이저를 이용한 적층제조 기술도 높은 구조적 요건을 수반하는 복잡한 항공우주 부품 및 산업용 부품의 제조에 채택되어 고성능 레이저의 적용 범위를 넓혀가고 있습니다. 레이저 시스템의 정확성, 속도, 자동화의 융합으로 인해 제조업체들은 생산 라인 전체에 첨단 레이저 솔루션을 통합하여 수율, 반복성 및 운영 효율성을 향상시킬 수 있도록 유도하고 있습니다.

로봇 레이저 가공 시스템 시장은 2026-2035년 연평균 복합 성장률(CAGR) 6.6%를 나타낼 것으로 예측됩니다. 이러한 시스템은 생산성과 정확도 향상을 위해 자동화에 대한 의존도가 높아지고 있는 자동차, 항공우주, 중공업 등의 분야에서 높은 수요를 보이고 있습니다. 로봇 레이저 시스템은 수작업을 줄이고 생산의 일관성을 향상시키며, 인더스트리 4.0 환경에 원활하게 통합될 수 있습니다. 로봇 레이저 가공은 정확하고 재현성 높은 결과를 제공하면서 연속적인 작업이 가능하므로 품질 기준을 유지하면서 생산 규모를 확대하고자 하는 제조업체에게 매력적인 투자 대상입니다.

고출력(6kW 이상) 부문은 중후한 재료 가공 응용 분야에 힘입어 2025년 27억 달러 규모에 달했습니다. 고출력 레이저는 후판 금속 절단, 자동차 섀시 제조, 조선, 철강 가공 등에 널리 도입되었습니다. 크고 반사성이 높은 금속 표면을 빠르고 효율적으로 절단할 수 있는 능력은 견고한 금속 가공 솔루션이 필요한 산업에서 없어서는 안 될 필수 요소입니다. 이러한 고출력 레이저의 채용 확대는 대규모 제조 공정에서 생산 중단을 방지하고 시장 매출 점유율에 큰 기여를 하고 있습니다.

2025년 북미 산업용 레이저 시스템 시장은 27.7%의 점유율을 차지했습니다. 이 지역의 성장은 고정밀 레이저 용접, 절단 및 미세 가공 솔루션을 필요로 하는 자동차, 항공우주 및 전자제품 제조업체의 강력한 수요에 힘입은 바 큽니다. 전기자동차 산업, 반도체 생산 및 첨단 금속 가공 시설의 확대는 파이버 레이저 및 초고속 레이저 시스템의 도입을 더욱 가속화하고 있습니다. 스마트 제조 인프라, 로봇 공학 및 인더스트리 4.0을 지원하는 생산 라인에 대한 투자로 인해 다양한 분야에서 첨단 레이저 기술의 도입이 촉진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 레이저 유형별, 2022-2035

제6장 시장 추산·예측 : 소재 유형별, 2022-2035

제7장 시장 추산·예측 : 시스템 구성별, 2022-2035

제8장 시장 추산·예측 : 용도별, 2022-2035

제9장 시장 추산·예측 : 최종사용자별, 2022-2035

제10장 시장 추산·예측 : 지역별, 2022-2035

제11장 기업 개요

KSA 26.04.20The Global Industrial Laser Systems Market was valued at USD 6.2 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 10.5 billion in 2035.

The market is propelled by the growing adoption of laser-based technologies in precision manufacturing, particularly for high-value applications that require accuracy and efficiency. Increasing demand for laser welding in electric vehicle battery production, laser marking in electronics manufacturing, ultrafast laser micromachining for semiconductor miniaturization, and laser-assisted additive manufacturing for aerospace and industrial components is driving industry expansion. Technological advances in fiber lasers, ultrafast lasers, and robotic integration allow manufacturers to reduce production times while improving quality, reliability, and energy efficiency. These factors, combined with ongoing investments in automation and Industry 4.0 processes, are creating strong growth opportunities across multiple industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.2 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 5.5% |

The industrial laser systems market is particularly fueled by the rising need for precision laser welding in battery and electronics manufacturing. Laser welding enables high-speed joining of conductive materials with minimal thermal distortion, ensuring strong structural integrity and improved electrical performance. Simultaneously, ultrafast laser micromachining is gaining traction in semiconductor manufacturing, enabling highly precise wafer cutting, micro-via drilling, and thin-film structuring without causing heat damage. Laser-based additive manufacturing is also increasingly adopted for producing complex aerospace components and industrial parts with high structural requirements, creating broader applications for high-performance lasers. The convergence of precision, speed, and automation in laser systems is pushing manufacturers to integrate advanced laser solutions across production lines, supporting improved yield, repeatability, and operational efficiency.

The robotic laser processing systems segment is expected to grow at a CAGR of 6.6% during 2026-2035. These systems are highly sought after in sectors like automotive, aerospace, and heavy manufacturing that increasingly rely on automation to enhance productivity and precision. Robotic laser systems reduce manual labor, improve production consistency, and integrate seamlessly into Industry 4.0 environments. The ability to operate continuously while delivering accurate and repeatable results has made robotic laser processing an attractive investment for manufacturers aiming to scale production while maintaining quality standards.

The high-power (>6 kW) segment reached USD 2.7 billion in 2025, driven by heavy-duty material processing applications. High-power lasers are widely deployed in thick metal cutting, automotive chassis manufacturing, shipbuilding, and steel fabrication. Their ability to cut large and reflective metal surfaces with high speed and efficiency makes them indispensable in industries requiring robust metal processing solutions. The growing adoption of these high-output lasers ensures uninterrupted production in large-scale fabrication operations, contributing significantly to the market's revenue share.

North America Industrial Laser Systems Market accounted for 27.7% share in 2025. The region's growth is largely driven by strong demand from automotive, aerospace, and electronics manufacturers, which require high-precision laser welding, cutting, and micromachining solutions. The expanding electric vehicle industry, semiconductor production, and advanced metal fabrication facilities are further accelerating the adoption of fiber and ultrafast laser systems. Investments in smart manufacturing infrastructure, robotics, and Industry 4.0-enabled production lines are enhancing the deployment of advanced laser-based technologies across multiple sectors.

Key companies operating in the Global Industrial Laser Systems Market include Coherent Corp., Han's Laser Technology Industry Group Co., Ltd., IPG Photonics Corporation, Jenoptik AG, Lumentum Holdings Inc., Raycus Fiber Laser Technologies Co., Ltd., Amada Miyachi America, Inc., TRUMPF Group, Toptica Photonics AG, nLIGHT, Inc., LPKF Laser & Electronics AG, Bystronic Laser AG, Sahajanand Laser Technology Limited, Maxphotonics Co., Ltd., and MKS Instruments, Inc. Companies in the Global Industrial Laser Systems Market are implementing strategies to strengthen their market presence and competitive position. Key initiatives include investing heavily in R&D to improve laser power, precision, and efficiency while developing new fiber, ultrafast, and robotic laser solutions tailored to high-demand sectors. Expanding product portfolios to cater to emerging applications in electric vehicles, semiconductors, aerospace, and industrial manufacturing is a critical growth strategy. Firms are also pursuing strategic collaborations with system integrators, OEMs, and automation technology providers to create integrated manufacturing solutions. Increasing global manufacturing footprints and after-sales service networks allow companies to enhance accessibility and reliability for end users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Laser type trends

- 2.2.2 Power range trends

- 2.2.3 System configuration trends

- 2.2.4 Application trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 EV battery manufacturing demanding precision laser welding

- 3.2.1.2 Consumer electronics production demanding high-precision laser marking

- 3.2.1.3 Semiconductor miniaturization requiring ultrafast laser micromachining

- 3.2.1.4 Medical device manufacturing requiring micro-scale laser processing

- 3.2.1.5 Automated smart factories integrating laser processing equipment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Skilled operator shortage for complex laser machining processes

- 3.2.2.2 Maintenance complexity in high-power industrial laser sources

- 3.2.3 Market opportunities

- 3.2.3.1 Ultrafast lasers adoption in semiconductor wafer processing

- 3.2.3.2 Laser additive manufacturing expansion in aerospace components

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Laser Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Fiber lasers

- 5.3 Co2 lasers

- 5.4 Solid-state lasers

- 5.5 Diode lasers

- 5.6 Ultrafast lasers

- 5.7 Excimer lasers

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Low power (<1 kW)

- 6.3 Medium power (1-6 kW)

- 6.4 High power (>6 kW)

Chapter 7 Market Estimates and Forecast, By System Configuration, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Standalone laser machines

- 7.3 Robotic laser processing systems

- 7.4 Integrated production line systems

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Cutting

- 8.3 Welding

- 8.4 Marking & engraving

- 8.5 Drilling

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Electronics manufacturing

- 9.4 Semiconductor fabrication

- 9.5 Aerospace & defense

- 9.6 Metal fabrication & industrial manufacturing

- 9.7 Medical devices

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 TRUMPF Group

- 11.1.2 IPG Photonics Corporation

- 11.1.3 Coherent Corp.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Lumentum Holdings Inc.

- 11.2.1.2 nLIGHT, Inc.

- 11.2.1.3 Amada Miyachi America, Inc.

- 11.2.1.4 MKS Instruments, Inc.

- 11.2.2 Asia Pacific

- 11.2.2.1 Han's Laser Technology Industry Group Co., Ltd.

- 11.2.2.2 Raycus Fiber Laser Technologies Co., Ltd.

- 11.2.2.3 Maxphotonics Co., Ltd.

- 11.2.2.4 Sahajanand Laser Technology Limited

- 11.2.3 Europe

- 11.2.3.1 Bystronic Laser AG

- 11.2.3.2 Jenoptik AG

- 11.2.3.3 LPKF Laser & Electronics AG

- 11.2.3.4 Toptica Photonics AG

- 11.2.1 North America