|

시장보고서

상품코드

1998852

유방 재건 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Breast Reconstruction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

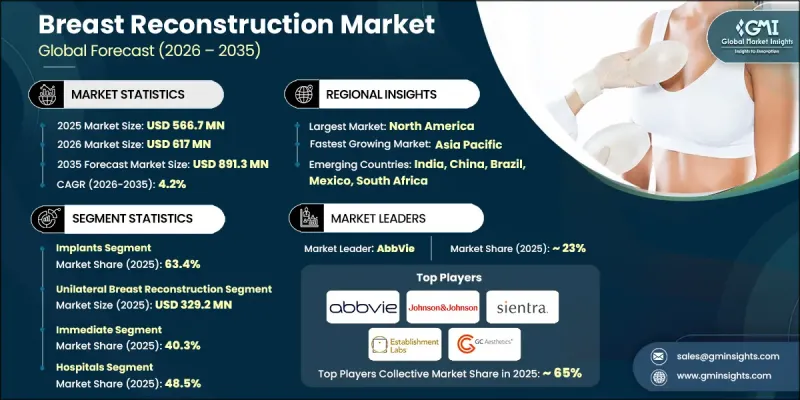

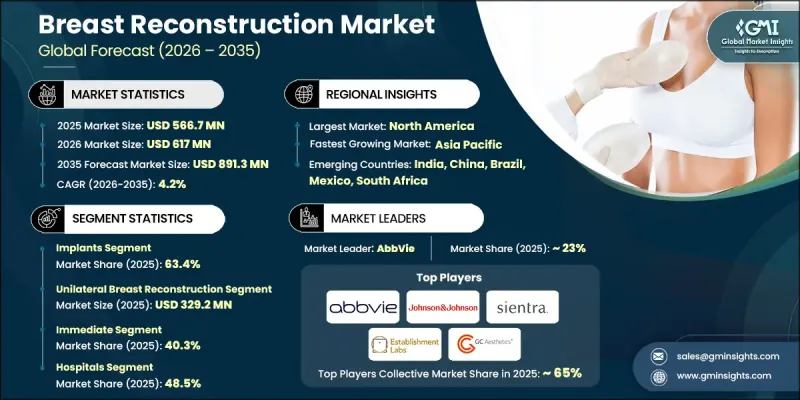

세계의 유방 재건 시장은 2025년에 5억 6,670만 달러로 평가되며, CAGR 4.2%로 성장하며, 2035년까지 8억 9,130만 달러에 달할 것으로 추정되고 있습니다.

유방 재건 시장의 꾸준한 성장은 주로 수술 기술의 지속적인 발전, 재건 치료 옵션에 대한 인식 증가, 최소 침습 수술에 대한 선호도 증가에 의해 주도되고 있습니다. 수술 계획 기술, 생체 재료 및 수술 후 관리의 개선으로 임상 결과와 환자 만족도가 크게 향상되었습니다. 동시에, 지원적인 보험 환급 제도와 정부의 의료 정책도 재건 수술에 대한 접근성 확대에 기여하고 있습니다. 재건 수술의 신체적, 심리적 이점에 대한 인식이 높아짐에 따라 더 많은 환자들이 치료의 일환으로 재건 수술을 고려하고 있습니다. 의료 프로바이더 및 지원 단체들도 환자들에게 재건 수술에 대한 인식 개선에 적극적으로 나서고 있으며, 이는 재건 수술의 보급을 촉진하고 환자층을 확대하는 데 기여하고 있습니다. 또한 재생조직 기술, 맞춤형 임플란트 솔루션, 첨단 수술기구의 혁신으로 치료의 정확성과 안전성이 지속적으로 향상되고 있습니다. 이러한 기술 발전은 의료 지원 정책 및 환자의 삶의 질에 대한 관심 증가와 함께 세계 유방 재건 시장에 유리한 성장 환경을 조성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 5억 6,670만 달러 |

| 예측액 | 8억 9,130만 달러 |

| CAGR | 4.2% |

유방재건술은 질병이나 선천성 기형으로 인한 외과적 절제나 구조적 손상을 입은 후 유방의 모양, 볼륨, 자연스러운 외관을 회복시키는 것을 목적으로 하는 수술을 말합니다. 이 수술은 인공 보형물을 사용하는 방법과 환자 자신의 신체 조직을 이용하는 방법을 통해 이루어집니다. 경우에 따라는 1차 수술 직후에 재건술을 시행하기도 하고, 환자의 희망이나 임상적 권고에 따라 추후에 시행하기도 합니다. 재건 수술의 심리적, 정서적 이점에 대한 인식이 높아짐에 따라 이러한 치료 옵션을 고려하는 환자가 증가하고 있습니다. 의료 전문가와 환자 지원 단체의 지속적인 지원도 수요 증가에 기여하고 있습니다.

2025년 기준, 임플란트 분야는 63.4%의 점유율을 차지했습니다. 이러한 높은 시장 점유율은 주로 다른 수술법에 비해 수술 시간이 상대적으로 짧고, 첨단 임플란트 기술이 널리 이용 가능하므로 임플란트 재건술이 널리 채택되고 있기 때문입니다. 임플란트 재료와 표면 기술의 개선으로 재건 수술을 받는 환자들에게 내구성, 안전성 및 심미적 결과가 향상되었습니다. 임플란트 설계의 지속적인 혁신으로 임상 결과가 크게 향상되고 환자 만족도가 높아지고 있습니다. 이러한 발전은 세계 시장에서 임플란트 재건술의 지속적인 우위를 지속적으로 지원하고 있습니다.

일측 유방 재건 부문은 2025년 3억 2,920만 달러의 시장 규모를 기록하며, 2026-2035년 연평균 3.8%의 성장률을 보일 것으로 전망됩니다. 유방 수술 후 균형과 미적 대칭을 회복하는 치료를 원하는 환자가 증가함에 따라 한쪽 재건 수술에 대한 수요는 계속 증가하고 있습니다. 의료영상 기술의 발전과 인공지능(AI)을 활용한 수술 전 계획 시스템의 도입으로 외과의사는 보다 높은 정확도로 재건수술을 시행하여 치료 결과를 향상시킬 수 있게 되었습니다. 이러한 기술은 수술의 정확성을 높일 뿐만 아니라 보다 일관된 미적 결과를 초래하는 데 도움이 되고 있습니다. 또한 규제 측면의 발전과 기술적으로 진보된 수술 전 계획 툴의 승인 증가로 인해 임상적 효율성이 향상되고 편측 유방 재건술의 채택이 더욱 촉진될 것으로 예측됩니다.

2025년 기준, 북미 유방 재건 시장은 45.2%의 점유율을 차지했습니다. 이 지역은 유방 관련 질환의 높은 유병률과 조기 진단 검진 프로그램이 널리 보급되어 있으며, 지속적으로 시장을 주도하고 있습니다. 조기 발견 노력으로 재건 수술 대상 환자 수가 크게 증가했고, 그 결과 유방 재건 수술에 대한 수요가 증가하고 있습니다. 또한 북미에는 수많은 주요 의료기기 제조업체와 기술 개발 기업이 있으며, 혁신적인 재건 솔루션을 적극적으로 도입하고 있습니다. 임플란트 재료, 조직 지지 기술 및 첨단 수술기구의 지속적인 제품 혁신은 수술 결과 향상에 기여하고 시장의 지속적인 성장을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035

제6장 시장 추산·예측 : 유형별, 2022-2035

제7장 시장 추산·예측 : 치료법별, 2022-2035

제8장 시장 추산·예측 : 최종 용도별, 2022-2035

제9장 시장 추산·예측 : 지역별, 2022-2035

제10장 기업 개요

KSA 26.04.20The Global Breast Reconstruction Market was valued at USD 566.7 million in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 891.3 million by 2035.

The steady expansion of the breast reconstruction market is largely driven by ongoing advancements in surgical technologies, increasing awareness regarding reconstructive treatment options, and a growing preference for minimally invasive procedures. Improvements in surgical planning techniques, biomaterials, and post-operative care have significantly enhanced clinical outcomes and patient satisfaction. At the same time, supportive reimbursement frameworks and favorable government healthcare initiatives are contributing to broader accessibility of reconstruction procedures. Rising awareness about the physical and psychological benefits of reconstructive surgery has encouraged more patients to consider these procedures as part of their treatment journey. Healthcare providers and advocacy organizations are also actively educating patients about available options, which help normalize reconstruction procedures and expand the patient base. Furthermore, innovation in regenerative tissue technologies, customized implant solutions, and advanced surgical tools continues to improve treatment precision and safety. These technological developments, combined with supportive healthcare policies and a growing focus on patient quality of life, are creating favorable growth conditions for the global breast reconstruction market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $566.7 Million |

| Forecast Value | $891.3 Million |

| CAGR | 4.2% |

Breast reconstruction refers to a surgical procedure designed to restore the shape, volume, and natural appearance of the breast following surgical removal or structural damage caused by medical conditions or congenital abnormalities. The procedure can be performed using artificial implants or by utilizing tissue from the patient's own body. In certain cases, reconstruction may take place immediately after the primary surgical procedure, while in other situations it may be performed at a later stage, depending on patient preferences and clinical recommendations. Increasing awareness regarding the psychological and emotional benefits associated with reconstructive procedures has encouraged a growing number of patients to explore these treatment options. Continuous support from medical professionals and patient advocacy initiatives has also contributed to increasing demand.

The implants segment held 63.4% share in 2025. This strong market share is primarily attributed to the high adoption of implant-based reconstruction techniques due to their relatively shorter procedure duration compared with other surgical methods and the widespread availability of advanced implant technologies. Improvements in implant materials and surface engineering have enhanced durability, safety profiles, and aesthetic outcomes for patients undergoing reconstruction procedures. Continuous innovation in implant design has significantly improved clinical performance while also increasing patient satisfaction. These developments continue to support the sustained dominance of implant-based reconstruction within the global market.

The unilateral breast reconstruction segment generated USD 329.2 million in 2025 and is expected to grow at a CAGR of 3.8% between 2026 and 2035. Demand for unilateral reconstruction procedures continues to increase as patients seek treatments that restore balance and aesthetic symmetry following breast surgery. Advancements in medical imaging technologies and the introduction of artificial intelligence-assisted surgical planning systems are enabling surgeons to perform reconstruction procedures with greater accuracy and improved outcomes. These technologies help enhance surgical precision while supporting more consistent aesthetic results. In addition, ongoing regulatory progress and increased approvals for technologically advanced surgical planning tools are expected to improve clinical efficiency and further encourage the adoption of unilateral breast reconstruction procedures.

North America Breast Reconstruction Market accounted for 45.2% share in 2025. The region continues to lead the market due to a high prevalence of breast-related medical conditions and the widespread adoption of early diagnostic screening programs. Early detection initiatives significantly increase the number of patients eligible for reconstructive procedures, which in turn strengthens demand for breast reconstruction surgeries. In addition, North America is home to numerous leading medical device manufacturers and technology developers that actively introduce innovative reconstruction solutions. Continuous product innovation in implant materials, tissue support technologies, and advanced surgical tools contributes to improved procedural outcomes, supporting the ongoing market expansion.

Key companies operating in the Global Breast Reconstruction Market include Johnson & Johnson, AbbVie, POLYTECH Health & Aesthetics, GC Aesthetics, Sientra, Establishment Labs, RTI Surgical, Sebbin, SILIMED, CEREPLAS, INTEGRA, HANSBIOMED, arion LABORATORIES, BIMINI HEALTH TECH, and Wanhe. Companies participating in the Breast Reconstruction Market are implementing several strategic initiatives to strengthen their competitive positioning and expand their global footprint. Leading manufacturers are focusing on continuous research and development activities to introduce innovative implant technologies, regenerative tissue solutions, and advanced surgical support materials. Many organizations are also investing in the development of customized implant designs and improved biomaterials to enhance safety, durability, and aesthetic outcomes. Strategic collaborations with healthcare providers, research institutions, and surgical centers help companies accelerate product development and increase clinical adoption. Companies are expanding their geographic presence through distribution partnerships and regulatory approvals in new markets.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 Procedure trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of breast cancer

- 3.2.1.2 Growing awareness about reconstructive surgery

- 3.2.1.3 Technological advancements in implants and mesh

- 3.2.1.4 Surge in cosmetic and aesthetic procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of breast reconstruction procedures

- 3.2.2.2 Surgical risks and complications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Increasing adoption of 3D printing and custom implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario (Driven by primary research)

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Customer insights (Driven by primary research)

- 3.11 Start-up scenarios (Driven by primary research)

- 3.12 Investment landscape (Driven by primary research)

- 3.13 Impact of AI and its future assessment

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Implants

- 5.2.1 Silicone breast implants

- 5.2.2 Saline breast implants

- 5.3 Tissue expander

- 5.4 Acellular dermal matrix

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Unilateral breast reconstruction

- 6.3 Bilateral breast reconstruction

Chapter 7 Market Estimates and Forecast, By Procedure, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Immediate

- 7.3 Delayed

- 7.4 Revision

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 arion LABORATORIES

- 10.3 BIMINI HEALTH TECH

- 10.4 CEREPLAS

- 10.5 Establishment Labs

- 10.6 GC Aesthetics

- 10.7 HANSBIOMED

- 10.8 INTEGRA

- 10.9 Johnson & Johnson

- 10.10 POLYTECH Health & Aesthetics

- 10.11 RTI Surgical

- 10.12 Sebbin

- 10.13 Sientra

- 10.14 SILIMED

- 10.15 Wanhe