|

시장보고서

상품코드

1998854

시트러스 펙틴 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Citrus Pectin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

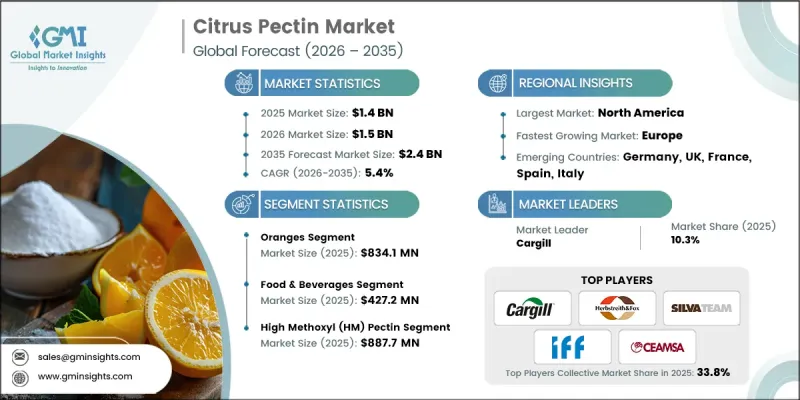

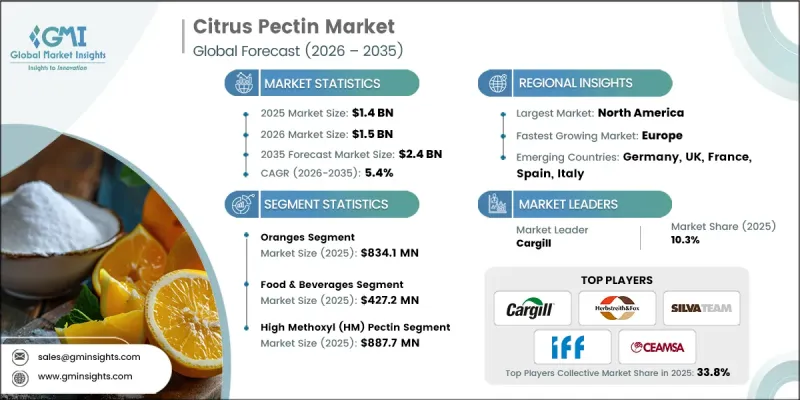

세계의 시트러스 펙틴 시장은 2025년에 14억 달러로 평가되며, CAGR 5.4%로 성장하며, 2035년까지 24억 달러에 달할 것으로 추정되고 있습니다.

시장 확대는 식품 및 음료, 뉴트리슈티컬, 의약품에서 천연 유래 식물성 원료에 대한 수요 증가에 힘입어 성장하고 있습니다. 주로 감귤류의 과피에서 추출되는 다당류인 감귤 펙틴은 겔화, 증점, 안정화 특성으로 높은 평가를 받고 있습니다. 다양한 제품에서 식감, 점도, 보존성을 향상시키면서 저당 배합과 클린 라벨을 지원하며, 배합의 다양성을 통해 다양한 제품에서 식감, 점도, 보존성을 향상시킬 수 있습니다. 고메톡실(HM) 펙틴은 산성 및 당분 함유 조건에서 겔을 형성하지만, 저메톡실(LM) 펙틴은 칼슘 이온을 필요로 하므로 잼, 젤리, 제과류, 유제품, 기능성 식품 등에 유연하게 적용될 수 있습니다. 천연 유래, 비GMO 원료에 대한 소비자의 선호도 증가와 식생활의 건강 효과에 대한 인식이 높아지면서 시트러스펙틴의 활용이 확대되고 있으며, 변화하는 식품 및 건강기능식품 수요에 대응하고자 하는 제조업체들에게 필수적인 기능성 원료로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 14억 달러 |

| 예측액 | 24억 달러 |

| CAGR | 5.4% |

오렌지 유래 펙틴 시장은 2025년 8억 3,410만 달러를 차지했습니다. 이는 이 원료에서 얻을 수 있는 펙틴의 범용성과 기능적 성능을 반영합니다. 오렌지 유래의 펙틴은 천연의 농축, 겔화, 안정화 특성으로 인해 식품 분야에서 널리 사용되고 있으며, 식감 및 제품 품질 향상에 필수적인 존재가 되고 있습니다. 또한 클린 라벨로서의 매력과 비 유전자 변형(Non-GMO)이라는 점은 자연스럽고 최소한의 가공만을 거친 원료를 찾는 건강 지향적인 소비자들 수요를 높이고 있습니다.

유통업체 및 도매업체 부문은 2025년 5억 7,890만 달러에 달했습니다. 이러한 채널은 식품 제조업체, 건강보조식품 회사, 제약회사 등 대량 구매자에게 도달하는 데 필수적입니다. 이는 제품의 광범위한 가용성을 보장하고, 맞춤형 배합을 용이하게 하며, 장기 계약을 지원하는 한편, 온라인 소매 플랫폼은 펙틴 제품을 찾는 소규모 제조업체와 전문 소비자에게 펙틴 제품에 대한 접근성을 개선하고 있습니다.

북미 감귤류 펙틴 시장은 2025년 5억 6,290만 달러 규모에 달했습니다. 기능성 식품, 저탄수화물 제품, 건강기능식품에 대한 관심이 높아지면서 그 확산이 가속화되고 있습니다. 미국에서는 감귤류 펙틴이 제과류, 음료, 유제품에 광범위하게 함유되어 건강을 중시하는 소비자의 니즈를 충족시키는 클린 라벨 제품을 생산하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 소스별, 2022-2035

제6장 시장 추산·예측 : 등급별, 2022-2035

제7장 시장 추산·예측 : 용도별, 2022-2035

제8장 시장 추산·예측 : 유통 채널별, 2022-2035

제9장 시장 추산·예측 : 지역별, 2022-2035

제10장 기업 개요

KSA 26.04.20The Global Citrus Pectin Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 2.4 billion by 2035.

Market expansion is driven by the growing demand for natural, plant-based ingredients in food, beverages, nutraceuticals, and pharmaceuticals. Citrus pectin, a polysaccharide extracted primarily from citrus fruit peels, is highly valued for its gelling, thickening, and stabilizing properties. Its versatility in formulation allows it to enhance texture, consistency, and shelf life across various products while supporting reduced-sugar formulations and clean-label initiatives. High methoxyl (HM) pectin forms gels under acidic and sugary conditions, whereas low methoxyl (LM) pectin requires calcium ions, enabling flexibility in application for jams, jellies, confectionery, dairy, and functional foods. Increasing consumer preference for natural, non-GMO ingredients and rising awareness of dietary health benefits are reinforcing the use of citrus pectin, making it a critical functional ingredient for manufacturers seeking to meet evolving food and supplement demands.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 5.4% |

The oranges segment accounted for USD 834.1 million in 2025, reflecting the versatility and functional performance of pectin derived from this source. Orange-based pectin is widely used in food systems for its natural thickening, gelling, and stabilizing characteristics, making it essential for improving texture and product quality. Its clean-label appeal and non-GMO status enhance demand among health-conscious consumers seeking natural and minimally processed ingredients.

The distributors and wholesalers segment reached USD 578.9 million in 2025. These channels are vital for reaching bulk buyers, including food manufacturers, dietary supplement companies, and pharmaceutical producers. They ensure widespread availability, facilitate customized formulations, and support long-term contracts, while online retail platforms are improving access for smaller manufacturers and specialty consumers seeking pectin products.

North America Citrus Pectin Market generated USD 562.9 million in 2025. Rising interest in functional foods, low-sugar products, and dietary supplements is driving adoption. In the United States, citrus pectin is widely incorporated into confectionery, beverages, and dairy products to create clean-label offerings that satisfy health-conscious consumer demands.

Leading companies operating in the Global Citrus Pectin Market include Cargill, Ingredion, Herbstreith & Fox KG Pektin-Fabriken, Tate & Lyle, Compania Espanola de Algas Marinas (CEAMSA), Quadra Chemicals, Silvateam, Fiberstar, Krishna Pectins Pvt Ltd, Labh Ingredients, and IFF. Key strategies adopted by companies in the Citrus Pectin Market focus on product innovation, including developing high-quality, low-sugar, and functional formulations to cater to health-conscious consumers. Strategic partnerships with food and beverage manufacturers help expand distribution channels and secure long-term contracts. Companies also invest in R&D to improve extraction efficiency, enhance purity, and create customized pectin solutions. Geographic expansion, especially into high-growth regions, strengthens market presence, while marketing campaigns emphasize natural, clean-label, and sustainable attributes to build brand loyalty and differentiate products in a competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Grade

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for clean-label ingredients

- 3.2.1.2 Expansion of functional foods and supplements

- 3.2.1.3 Increased processed and convenience food consumption

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Raw material supply fluctuations

- 3.2.2.2 High extraction and processing costs

- 3.2.3 Opportunities

- 3.2.3.1 Low-sugar and sugar-free product development

- 3.2.3.2 Pharmaceutical and nutraceutical applications

- 3.2.3.3 Sustainable and biodegradable packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Oranges

- 5.3 Lemon

- 5.4 Grapefruit

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Grade, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 High Methoxyl (HM) Pectin

- 6.3 Low Methoxyl (LM) Pectin

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & Beverages

- 7.3 Bakery and Confectionery

- 7.4 Pharmaceutical

- 7.5 Cosmetic and Personal Care Products

- 7.6 Dietary Supplements

- 7.7 Functional Food

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct Sales

- 8.3 Distributors and Wholesalers

- 8.4 Online Retail

- 8.5 Convenience Stores

- 8.6 Specialty Stores

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Cargill

- 10.2 Ingredion

- 10.3 Herbstreith & Fox KG Pektin-Fabriken

- 10.4 Tate & Lyle

- 10.5 Compania Espanola de Algas Marinas (CEAMSA)

- 10.6 Quadra Chemicals

- 10.7 Silvateam

- 10.8 CEAMSA

- 10.9 Fiberstar

- 10.10 Krishna Pectins Pvt Ltd

- 10.11 Labh Ingredients

- 10.12 IFF