|

시장보고서

상품코드

2019023

철도용 브레이크 패드 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Railway Brake Pads Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

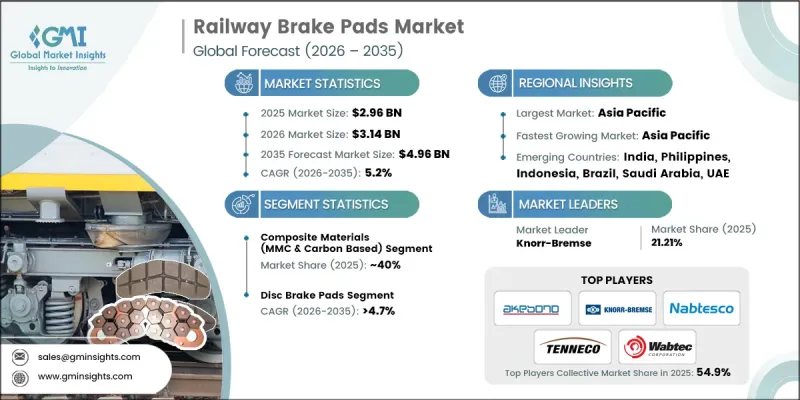

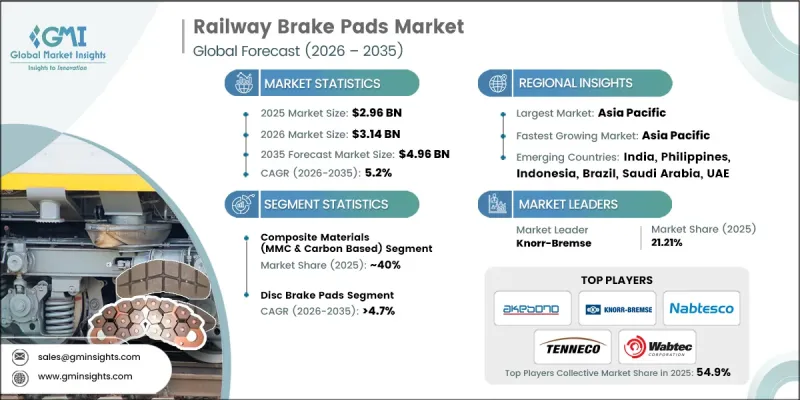

세계의 철도용 브레이크 패드 시장은 2025년에 29억 6,000만 달러로 평가되었으며, CAGR 5.2%로 성장하여 2035년까지 49억 6,000만 달러에 달할 것으로 추정됩니다.

안전 요구 사항 강화, 축 중량 증가, 철도 운송 밀도 증가로 인해 브레이크 시스템에 대한 기대치가 재정의되면서 철도용 브레이크 패드 산업은 큰 변화의 시기를 맞이하고 있습니다. 브레이크 패드는 더 이상 단순한 표준 교체 부품으로 취급되지 않고 제동 성능, 휠 내구성, 소음 수준 및 규정 준수에 직접적인 영향을 미치는 중요한 안전 부품으로 설계되었습니다. 철도 시스템이 고속화, 화물 적재량 증가 등 더욱 가혹한 조건에서 운영되는 가운데, 제동 부품의 성능은 운영 효율성 확보와 장기적인 자산 보호에 필수적인 요소로 자리 잡았습니다. 기술 발전은 내구성 향상, 마모 감소, 더 엄격한 환경 요구 사항에 대한 대응에 초점을 맞추고 있습니다. 동시에, 예지보전 및 상태 모니터링 유지보수 관행이 확산됨에 따라 라이프사이클 관리에서 브레이크 패드의 중요성이 커지고 있습니다. 철도 사업자들은 신뢰성 향상, 다운타임 감소, 교체 주기 최적화를 위해 성능 데이터와 유지보수 지식을 점점 더 많이 활용하고 있으며, 이는 전 세계 철도 네트워크에서 첨단 브레이크 솔루션의 전략적 가치를 더욱 높여주고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035 |

| 시작 시점 시장 규모 | 29억 6,000만 달러 |

| 예측 규모 | 49억 6,000만 달러 |

| CAGR | 5.2% |

복합재료(MMC 및 탄소 기반) 부문은 2025년 40%의 점유율을 차지했으며, 2035년까지 CAGR 4.9%로 성장할 것으로 예상됩니다. 이 소재는 높은 열 안정성, 낮은 마모율, 고부하 작동 환경에서의 안정적인 마찰 성능으로 인해 널리 선호되고 있습니다. 극한의 온도에서도 효과적으로 작동하고 소음과 환경 영향을 최소화하는 능력은 진화하는 규제 표준을 준수하고 현대 철도 시스템 전반에 걸쳐 보급을 촉진하는 데 도움이 되고 있습니다.

디스크 브레이크 패드 부문은 2025년에 60%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 4.7%로 성장할 것으로 예상됩니다. 이 부문은 우수한 제동 효율, 작동 신뢰성, 첨단 차량 시스템과의 호환성을 바탕으로 선도적인 위치를 유지하고 있습니다. 디스크 브레이크 패드는 특히 고속 주행 및 고하중 조건에서 안정적이고 정밀한 제동 성능을 발휘하는 동시에 진동과 소음을 줄여줍니다. 철도 사업자들이 안전, 비용 효율성 및 시스템 성능 향상을 우선시함에 따라, 보다 진보된 제동 시스템으로의 전환이 가속화되고 있습니다.

북미 철도용 브레이크 패드 시장은 2025년에 32%의 점유율을 차지하며 2035년까지 연평균 4.9%의 성장률을 보일 것으로 예상됩니다. 이 지역의 성장은 광범위한 철도 인프라, 활발한 화물 운송 및 차량의 지속적인 사용으로 뒷받침되고 있습니다. 내구성과 고성능을 겸비한 브레이크 패드에 대한 지속적인 수요는 높은 운행 빈도와 잦은 유지보수 주기의 필요성에 의해 주도되고 있습니다. 또한, 철도 현대화 및 도시 교통 시스템에 대한 지속적인 투자는 이 지역 전체의 꾸준한 수요 성장에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 재료별, 2022-2035

제6장 시장 추정 및 예측 : 제품별, 2022-2035

제7장 시장 추정 및 예측 : 열차 유형별, 2022-2035

제8장 시장 추정 및 예측 : 판매 채널별, 2022-2035

제9장 시장 추정 및 예측 : 지역별, 2022-2035

제10장 기업 개요

KSM 26.05.06The Global Railway Brake Pads Market was valued at USD 2.96 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 4.96 billion by 2035.

The railway brake pads industry is undergoing a significant transformation as safety requirements, increasing axle loads, and rising rail traffic density reshape braking system expectations. Brake pads are no longer treated as standard replacement parts but are now engineered as critical safety components that directly affect stopping performance, wheel durability, acoustic output, and regulatory compliance. As rail systems continue to operate under more demanding conditions, including higher speeds and heavier freight loads, the performance of braking components has become essential to ensuring operational efficiency and long-term asset protection. Technological progress is focused on improving durability, reducing wear, and meeting stricter environmental requirements. At the same time, the growing adoption of predictive and condition-based maintenance practices is elevating the importance of brake pads in lifecycle management. Operators are increasingly relying on performance data and maintenance insights to improve reliability, reduce downtime, and optimize replacement cycles, reinforcing the strategic value of advanced braking solutions across global rail networks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.96 Billion |

| Forecast Value | $4.96 Billion |

| CAGR | 5.2% |

The composite materials (MMC and carbon-based) segment held 40% share in 2025 and is projected to grow at a CAGR of 4.9% through 2035. These materials are widely preferred due to their enhanced thermal stability, reduced wear rates, and consistent friction performance under high-stress operating environments. Their ability to function effectively under extreme temperatures while minimizing noise and environmental impact supports compliance with evolving regulatory standards, driving their widespread use across modern rail systems.

The disc brake pads segment held a 60% share in 2025 and is expected to grow at a CAGR of 4.7% between 2026 and 2035. This segment continues to lead due to its superior braking efficiency, operational reliability, and compatibility with advanced rolling stock systems. Disc brake pads deliver stable and precise braking performance, especially in high-speed and heavy-load conditions, while also reducing vibration and noise levels. The transition toward more advanced braking systems is accelerating as rail operators prioritize safety, cost efficiency, and improved system performance.

North America Railway Brake Pads Market held 32% share in 2025 and is anticipated to grow at a CAGR of 4.9% through 2035. The region's growth is supported by extensive rail infrastructure, high freight movement, and continuous utilization of rolling stock. Sustained demand for durable and high-performance brake pads is driven by operational intensity and the need for frequent maintenance cycles. Additionally, ongoing investments in rail modernization and urban transit systems are contributing to consistent demand growth across the region.

Key companies operating in the Global Railway Brake Pads Market include Alstom, Knorr-Bremse, Wabtec, Hitachi Rail, Siemens, Tenneco, Akebono Brake Industry, Nabtesco, SGL Carbon, and Miba. Companies in the Global Railway Brake Pads Market are strengthening their competitive position by focusing on product innovation, material advancement, and strategic expansion. They are investing in research and development to enhance braking efficiency, durability, and environmental performance. Manufacturers are also adopting advanced composite technologies to meet evolving regulatory and operational requirements. Strategic collaborations and long-term supply agreements with rail operators are helping companies secure consistent demand and expand their market presence. In addition, firms are leveraging digital solutions and predictive maintenance capabilities to improve product reliability and lifecycle performance. Expanding global production networks and optimizing supply chains are further enabling companies to meet rising demand while maintaining cost efficiency and operational scalability.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Product

- 2.2.4 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global passenger and freight rail traffic volumes

- 3.2.1.2 Increase in railway safety and braking performance regulations

- 3.2.1.3 Surge in high-speed rail and urban transit projects

- 3.2.1.4 Rise in adoption of preventive and condition-based maintenance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Long replacement cycles in low-utilization rail networks

- 3.2.2.2 Price sensitivity and cost-driven procurement practices

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in demand for low-noise and low-emission brake pad materials

- 3.2.3.2 Surge in rail infrastructure investments in emerging economies

- 3.2.3.3 Increase in long-term maintenance and lifecycle service contracts

- 3.2.3.4 Rise in demand for high-durability brake pads for heavy-haul freight

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States: Federal Railroad Safety Act (FRSA) & FRA Brake System Safety Standards (49 CFR Part 232)

- 3.4.2 Europe

- 3.4.2.1 Germany: Eisenbahn-Bau- und Betriebsordnung (EBO)

- 3.4.2.2 United Kingdom: Railways and Other Guided Transport Systems (Safety) Regulations (ROGS)

- 3.4.2.3 France: Railway Safety Decree (Decret relatif a la securite ferroviaire)

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Railway Safety Management Regulations of the People’s Republic of China

- 3.4.3.2 Japan: Ministerial Ordinance on Technical Standards for Railways (MLIT)

- 3.4.3.3 South Korea: Railway Safety Act

- 3.4.3.4 Singapore: Rapid Transit Systems Act

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Railway Transport Safety Regulations (ANTT)

- 3.4.4.2 Mexico: Railway Service Regulatory Law (ARTF)

- 3.4.4.3 Chile: Railway Safety and Operations Regulations (MTT)

- 3.4.5 MEA

- 3.4.5.1 United Arab Emirates: Federal Railway Law No. 8 of 2020

- 3.4.5.2 Saudi Arabia: Railway Safety Regulatory Framework (Saudi Railway Safety Authority)

- 3.4.5.3 South Africa:Railway Safety Regulator Act, 2002Porter's analysis

- 3.4.1 North America

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Pricing Analysis

- 3.9.1 By region

- 3.9.2 By Product

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook & opportunities

- 3.13 Maintenance, repair & replacement cycle analysis

- 3.13.1 Brake pad lifecycle & wear characteristics

- 3.13.2 Replacement interval by train type & operating conditions

- 3.13.3 Predictive maintenance technologies & adoption

- 3.13.4 Cost analysis: preventive vs corrective maintenance

- 3.13.5 Inventory management & just-in-time practices

- 3.13.6 Extended life solutions & cost-benefit analysis

- 3.14 Digitalization & smart rail integration impact

- 3.14.1 Iot-enabled brake pad condition monitoring systems

- 3.14.2 Real-time wear sensor technologies

- 3.14.3 Integration with train management systems (tms)

- 3.14.4 Big data analytics for predictive replacement

- 3.14.5 Digital twin applications in brake system optimization

- 3.14.6 Blockchain for supply chain traceability

- 3.14.7 Impact of industry 4.0 on manufacturing & distribution

- 3.15 Customer buying behavior & procurement analysis

- 3.15.1 Railway operator procurement processes & decision criteria

- 3.15.2 Oem vs aftermarket purchase decision drivers

- 3.15.3 Total cost of ownership (tco) evaluation framework

- 3.15.4 Supplier qualification & approval procedures

- 3.15.5 Long-term supply agreements & partnership models

- 3.15.6 Tender & rfp analysis for major railway projects

- 3.15.7 Influence of sustainability & esg criteria on procurement

- 3.15.8 Regional procurement policy variations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Organic / Non-Asbestos Organic (NAO)

- 5.3 Sintered Metal

- 5.4 Semi-Metallic

- 5.5 Composite Materials (MMC & Carbon-Based)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Disc Brake Pads

- 6.3 Tread Brake Blocks / Shoes

Chapter 7 Market Estimates & Forecast, By Train Type, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Passenger Trains

- 7.3 Freight Trains

- 7.4 Metro / Urban Transit

- 7.5 Light Rail / Trams

- 7.6 Locomotives

- 7.7 Monorail

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Belgium

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Akebono Brake Industry

- 10.1.2 Alstom

- 10.1.3 CRRC

- 10.1.4 DAKO-CZ

- 10.1.5 Hitachi Rail.

- 10.1.6 Knorr-Bremse

- 10.1.7 Miba

- 10.1.8 Nabtesco

- 10.1.9 SGL Carbon

- 10.1.10 Siemens Mobility

- 10.1.11 Tenneco

- 10.1.12 Wabtec

- 10.2 Regional Players

- 10.2.1 Brakes India Private

- 10.2.2 Hindustan Composites

- 10.2.3 Jurid Railway Solutions

- 10.2.4 Railway Equipment Company (REC)

- 10.2.5 SAB WABCO India

- 10.2.6 Tenmat

- 10.2.7 Tribo Rail Group

- 10.2.8 TSE Brakes

- 10.3 Emerging Players

- 10.3.1 Advanced Material Labs

- 10.3.2 BrakeWear Analytics

- 10.3.3 EcoBrake Systems

- 10.3.4 GreenBrake Technologies

- 10.3.5 Rail Friction Innovations

- 10.3.6 Smart Rail Solutions

- 10.3.7 TMD Friction

- 10.3.8 Youcai