|

시장보고서

상품코드

2019051

반려동물용 의약품 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Companion Animal Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

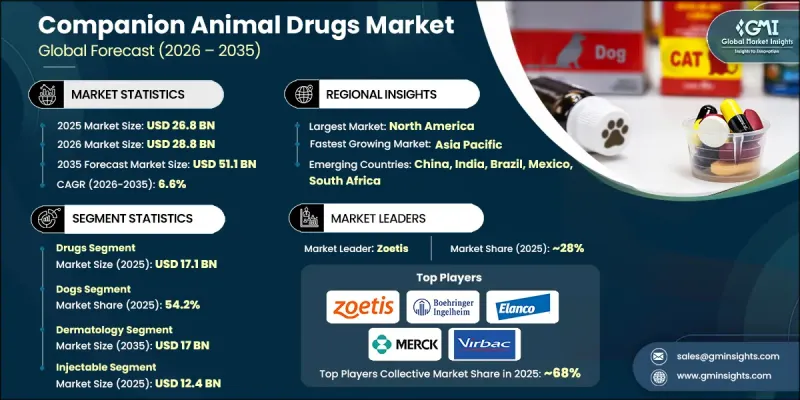

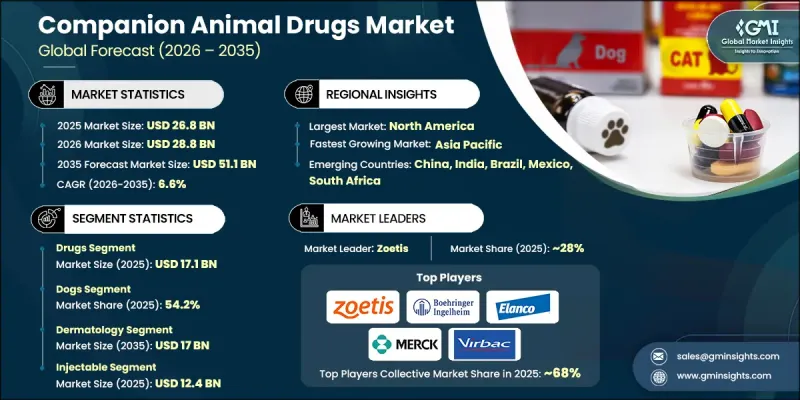

세계의 반려동물용 의약품 시장은 2025년에 268억 달러로 평가되고 CAGR 6.6%로 성장하며, 2035년까지 511억 달러에 달할 것으로 추정되고 있습니다.

반려동물 사육두수 증가, 반려동물의 만성질환 및 감염성 질환의 유병률 증가, 반려동물 보호자들의 첨단 수의학에 대한 투자 의지가 높아짐에 따라 이 같은 성장세가 지속되고 있습니다. 반려동물 보호자들은 사랑하는 동물을 가족의 일원으로 여기는 경향이 강해지면서 예방약, 백신 및 전문 치료에 대한 수요가 증가하고 있습니다. 반려동물 건강관리 인프라의 확충과 반려동물의 건강과 웰빙에 대한 대중의 인식이 높아짐에 따라 시장 성장이 더욱 가속화되고 있습니다. 관절염, 당뇨병, 심혈관 질환, 기생충 감염 등의 만성질환은 반려동물에게 많이 나타나며, 효과적인 의약품의 필요성을 강조하고 있습니다. 동물병원이 혁신적인 치료 솔루션과 예방의학 접근법을 도입함에 따라 반려동물용 의약품에 대한 수요는 전 세계에서 계속 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 268억 달러 |

| 예측액 | 511억 달러 |

| CAGR | 6.6% |

반려동물용 의약품에는 반려동물의 건강 상태를 예방, 치료 또는 관리하기 위해 제조된 의약품, 백신, 약용 사료첨가제 등이 포함됩니다. 이러한 의약품은 만성질환, 감염성 질환, 피부질환을 치료하는 것은 물론, 동물 간 전염성 질환의 확산을 억제하는 데 필수적입니다.

2025년 의약품 부문은 관절염, 암, 피부질환 등 만성질환 및 감염성 질환의 증가에 힘입어 171억 달러를 차지할 것으로 예상됩니다. 반려동물의 '인간화' 추세는 동물의 복지를 향상시키기 위해 항생제, 항염증약, 구충제 등 첨단 동물용 의약품에 대한 투자를 더욱 촉진하고 있습니다.

피부과 분야는 2035년까지 170억 달러에 달할 것으로 예상됩니다. 알레르기성 피부염, 기생충 감염, 세균성 또는 진균성 감염을 포함한 피부 질환의 높은 발생률은 피부과 치료에 대한 수요를 촉진하고 있습니다. 반려동물은 환경 알레르겐, 음식물 과민증, 기생충의 영향을 받기 쉽기 때문에 항알레르기제, 항진균제, 항생제, 구충제는 시장에서 필수적인 카테고리로 자리 잡았습니다.

북미 반려동물 의약품 시장은 2025년 42.9%의 점유율을 차지하며 2035년까지 CAGR 6.3%로 성장할 것으로 예상됩니다. 이 지역의 성장은 높은 반려동물 보유율, 높은 수의학 인프라, 그리고 반려동물 건강관리에 대한 막대한 지출에 의해 지원되고 있습니다. 미국은 반려동물의 '인간화'가 진전되고 예방 및 치료 시술의 채택이 증가함에 따라 이 시장에 큰 기여를 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035년

제6장 시장 추산·예측 : 적응별, 2022-2035년

제7장 시장 추산·예측 : 동물 유형별, 2022-2035년

제8장 시장 추산·예측 : 투여 경로별, 2022-2035년

제9장 시장 추산·예측 : 유통 채널별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.05.13The Global Companion Animal Drugs Market was valued at USD 26.8 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 51.1 billion by 2035.

The expansion is driven by the rising adoption of companion animals, an increasing prevalence of chronic and infectious diseases in pets, and the growing willingness of owners to invest in advanced veterinary care. Pet owners increasingly consider their animals as family members, fueling demand for preventive medications, vaccinations, and specialized treatments. The market growth is further supported by the expanding veterinary healthcare infrastructure and increased public awareness of pet health and wellness. Chronic conditions like arthritis, diabetes, cardiovascular disorders, and parasitic infections are common in companion animals, emphasizing the need for effective pharmaceuticals. As veterinary practices embrace innovative therapeutic solutions and preventive care approaches, the demand for companion animal drugs continues to rise globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.8 Billion |

| Forecast Value | $51.1 Billion |

| CAGR | 6.6% |

Companion animal drugs include pharmaceuticals, vaccines, and medicated feed additives formulated to prevent, treat, or manage health conditions in pets. These drugs are essential in addressing chronic illnesses, infections, and dermatological conditions, as well as in controlling the spread of contagious diseases among animals.

In 2025, the drugs segment accounted for USD 17.1 billion, driven by increasing cases of chronic illnesses and infections such as arthritis, cancer, and skin conditions. The rising trend of pet humanization has further encouraged investment in advanced veterinary medicines, including antibiotics, anti-inflammatory agents, and parasiticides, to enhance animal well-being.

The dermatology segment is expected to reach USD 17 billion by 2035. High incidence of skin conditions, including allergic dermatitis, parasitic infestations, and bacterial or fungal infections, fuels demand for dermatological treatments. Pets are often susceptible to environmental allergens, food sensitivities, and parasites, which have made anti-allergy medications, antifungals, antibiotics, and parasiticides a vital category within the market.

North America Companion Animal Drugs Market held a 42.9% share in 2025 and is projected to grow at a CAGR of 6.3% through 2035. The regional growth is supported by high pet ownership, advanced veterinary infrastructure, and strong expenditure on pet healthcare. The U.S. contributes significantly to this market due to the rising humanization of pets and increased adoption of preventive and therapeutic treatments.

Key players in the Global Companion Animal Drugs Market include Boehringer Ingelheim International, Zoetis, Elanco Animal Health Incorporated, Vetoquinol, Ceva Sante Animale, Dechra Pharmaceuticals, HIPRA, Indian Immunologicals, Agrolabo, Chanelle Pharma, Endovac Animal Health, Merck, Symrise, Norbrook, and Virbac. Key strategies adopted by companies in the Global Companion Animal Drugs Market include investing heavily in research and development to create innovative and effective pharmaceuticals targeting specific diseases and preventive care solutions. Firms focus on expanding product portfolios across therapeutic areas such as dermatology, cardiology, and endocrinology to meet diverse pet healthcare needs. Partnerships with veterinary clinics, hospitals, and distributors help strengthen market reach and ensure the timely availability of products. Companies also emphasize regulatory compliance, quality assurance, and education programs for veterinarians to enhance adoption. Geographic expansion and targeted marketing campaigns are employed to build brand recognition and boost market share in emerging regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Animal type trends

- 2.2.4 Indication trends

- 2.2.5 Route of administration trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising companion animal population

- 3.2.1.2 Increasing prevalence of animal diseases

- 3.2.1.3 Advancements in veterinary pharmaceuticals

- 3.2.1.4 Expansion of veterinary healthcare infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of veterinary drugs and treatments

- 3.2.2.2 Limited access to veterinary services in developing regions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of novel biologics and immunotherapies

- 3.2.3.2 Expansion of e-commerce veterinary pharmacies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Pipeline/clinical trial landscape (Driven by Primary Research)

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.7 Pet population statistics, by country (Driven by Primary Research)

- 3.8 Future market trends

- 3.9 Impact of AI & generative AI on the market

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Drugs

- 5.2.1 Antiparasitic

- 5.2.2 Anti-inflammatory

- 5.2.3 Anti-infectives

- 5.2.4 Corticosteroids

- 5.2.5 Tranquilizers

- 5.2.6 Cardiovascular drugs

- 5.2.7 Gastrointestinal drugs

- 5.2.8 Other drugs

- 5.3 Vaccines

- 5.3.1 Modified live vaccines (MLV)

- 5.3.2 Killed inactivated vaccines

- 5.3.3 Recombinant vaccines

- 5.4 Medicated feed additives

- 5.4.1 Antibiotics

- 5.4.2 Vitamins

- 5.4.3 Amino acids

- 5.4.4 Enzymes

- 5.4.5 Antioxidants

- 5.4.6 Prebiotics and probiotics

- 5.4.7 Minerals

- 5.4.8 Other medicated feed additives

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dermatology

- 6.3 Cardiovascular diseases

- 6.4 Gastrointestinal diseases

- 6.5 Respiratory diseases

- 6.6 Other indications

Chapter 7 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Dogs

- 7.3 Cats

- 7.4 Horses

- 7.5 Other animal types

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Topical

- 8.5 Other routes of administration

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospital pharmacies

- 9.3 E-commerce

- 9.4 Retail pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Poland

- 10.3.7 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Taiwan

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 GCC Countries

- 10.6.3 Israel

Chapter 11 Company Profiles

- 11.1 Agrolabo

- 11.2 Boehringer Ingelheim International

- 11.3 Ceva Sante Animale

- 11.4 Chanelle Pharma

- 11.5 Dechra Pharmaceuticals

- 11.6 Elanco Animal Health Incorporated

- 11.7 Endovac Animal Health

- 11.8 HIPRA

- 11.9 Indian Immunologicals

- 11.10 Merck

- 11.11 Norbrook

- 11.12 Symrise

- 11.13 Vetoquinol

- 11.14 Virbac

- 11.15 Zoetis