|

시장보고서

상품코드

2019064

자동차 연료 이송 펌프 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Fuel Transfer Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

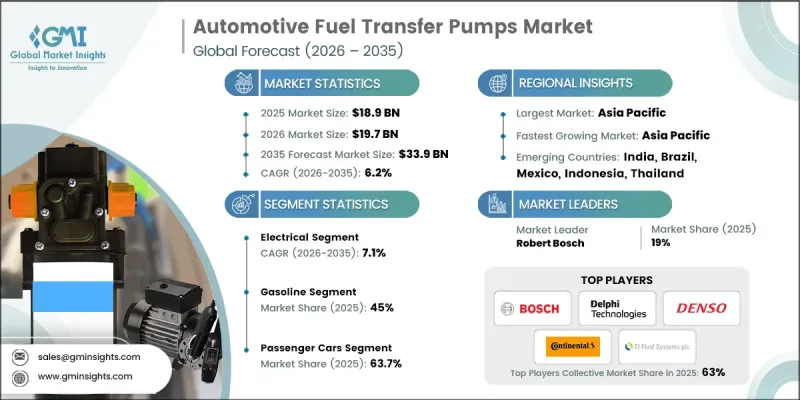

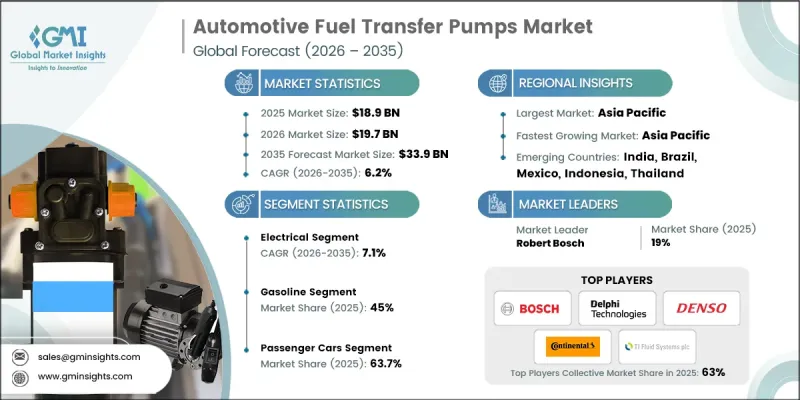

세계의 자동차 연료 이송 펌프 시장은 2025년에 189억 달러로 평가되었으며, CAGR 6.2%로 성장하여 2035년까지 339억 달러에 달할 것으로 추정됩니다.

자동차 연료 이송 펌프 시장은 효율적인 연료 공급 시스템이 여전히 필수적인 내연기관차에 대한 의존도가 지속되고 있는 것이 원동력이 되고 있습니다. 승용차 및 상용차 생산 증가로 인해 OEM(순정 부품) 및 애프터마켓 채널 모두에서 연료 이송 펌프에 대한 지속적인 수요가 발생하고 있습니다. 또한, 자동차 연료 이송 펌프 시장은 물류 및 화물 운송의 급속한 성장의 혜택을 누리고 있습니다. 이로 인해 전 세계적으로 상용차량이 증가하고 있습니다. 이러한 차량은 장시간의 운행 주기를 지원하기 위해 내구성이 높고 효율적인 연료 시스템이 필요합니다. 그 결과, 고성능 연료 이송 펌프에 대한 수요가 지속적으로 증가하고 있습니다. 또한, 제조업체들은 시스템의 신뢰성과 운영 효율성 향상에 주력하고 있으며, 이는 여러 차량 카테고리에 걸쳐 자동차 연료 이송 펌프 시장의 성장을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 189억 달러 |

| 예측 규모 | 339억 달러 |

| CAGR | 6.2% |

자동차 연료 이송 펌프 시장은 전 세계 차량 보유대수의 노후화에 영향을 받고 있으며, 이는 교체 부품의 수요를 견인하고 있습니다. 차량의 사용 연한이 경과함에 따라 연료 시스템의 주요 부품에 대한 유지보수 및 교체 필요성이 계속 증가하고 있습니다. 가동 중 부하와 장기간 사용으로 인한 마모 증가는 애프터마켓의 수요를 더욱 촉진하고 있습니다. 이러한 추세는 차량 보유 대수가 많은 지역에서 특히 두드러지며, 장기적인 사용 주기가 연료 이송 펌프의 교체 수요를 안정적으로 뒷받침하고 있습니다.

전기 부문은 2025년 58%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 7.1%로 성장할 것으로 예상됩니다. 현대 차량은 정밀한 유량 제어와 안정적인 압력을 필요로 하는 전자식 연료 공급 시스템을 점점 더 많이 채택하고 있으며, 이 부문의 중요성이 증가하고 있습니다. 자동차 연료 이송 펌프 시장은 내구성, 내마모성, 경량화 등 전기 펌프 설계의 발전으로 혜택을 누리고 있습니다. 이러한 발전은 효율 기준 충족을 지원하는 동시에 전체 차량 성능 향상에도 기여하고 있습니다.

가솔린 부문은 2025년 45%의 점유율을 차지했으며, 2035년까지 연평균 6.1%의 성장률을 기록할 것으로 전망됩니다. 이 우위는 신뢰할 수 있는 연료 공급 시스템을 필요로 하는 가솔린 차량의 보급에 의해 뒷받침되고 있습니다. 자동차 연료 이송 펌프 시장은 견조한 생산량과 지속적인 교체 수요에 힘입어 OEM과 애프터마켓 부문 모두에서 지속적인 성장이 예상됩니다.

미국의 자동차 연료 이송 펌프 시장은 2025년 43억 달러에 달했습니다. 미국 내 자동차 연료 이송 펌프 시장은 내구성이 뛰어난 연료 시스템과 높은 주행 성능을 갖춘 차량에 대한 강한 수요로 인해 확대되고 있습니다. 이 시장은 방대한 차량 보유 대수와 장기간의 사용 주기가 뒷받침하고 있으며, 이는 안정적인 교체 수요를 창출하고 있습니다. 시간이 지남에 따라 연료 시스템 부품에 대한 유지보수 요구사항이 지속적으로 증가함에 따라, 잘 구축된 서비스 네트워크와 탄탄한 애프터마켓 생태계가 더욱 성장을 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 유형별, 2022-2035

제6장 시장 추정 및 예측 : 연료별, 2022-2035

제7장 시장 추정 및 예측 : 차종별, 2022-2035

제8장 시장 추정 및 예측 : 판매 채널별, 2022-2035

제9장 시장 추정 및 예측 : 지역별, 2022-2035

제10장 기업 개요

KSM 26.05.06The Global Automotive Fuel Transfer Pumps Market was valued at USD 18.9 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 33.9 billion by 2035.

The automotive fuel transfer pumps market is driven by the continued reliance on internal combustion engine vehicles, where efficient fuel delivery systems remain essential. Increasing production of passenger and commercial vehicles is creating sustained demand for fuel transfer pumps across original equipment and replacement channels. The automotive fuel transfer pumps market is also benefiting from the rapid growth of logistics and freight transportation, which is expanding the global fleet of commercial vehicles. These vehicles require durable and efficient fuel systems to support extended operational cycles. As a result, demand for high-performance fuel transfer pumps continues to rise. In addition, manufacturers are focusing on improving system reliability and operational efficiency, which is further supporting the expansion of the automotive fuel transfer pumps market across multiple vehicle categories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.9 Billion |

| Forecast Value | $33.9 Billion |

| CAGR | 6.2% |

The automotive fuel transfer pumps market is also influenced by the increasing age of the global vehicle fleet, which is driving demand for replacement components. As vehicles accumulate higher usage over time, the need for maintenance and replacement of essential fuel system parts continues to grow. Exposure to operational stress and prolonged usage contributes to increased wear, further strengthening aftermarket demand. This trend is particularly significant in regions with large vehicle populations, where long-term usage cycles support consistent demand for replacement fuel transfer pumps.

The electric segment accounted for 58% share in 2025 and is expected to grow at a CAGR of 7.1% from 2026 to 2035. This segment is gaining prominence as modern vehicles increasingly incorporate electronic fuel delivery systems that require precise flow control and consistent pressure. The automotive fuel transfer pumps market is benefiting from advancements in electric pump design, including improvements in durability, resistance to wear, and lightweight construction. These developments are supporting compliance with efficiency standards while enhancing overall vehicle performance.

The gasoline segment held a 45% share in 2025 and is projected to grow at a CAGR of 6.1% through 2035. This dominance is supported by the widespread presence of gasoline-powered vehicles, which continue to require reliable fuel delivery systems. The automotive fuel transfer pumps market is sustained by strong production volumes and ongoing replacement demand, ensuring continued growth across both OEM and aftermarket segments.

U.S. Automotive Fuel Transfer Pumps Market reached USD 4.3 billion in 2025. The automotive fuel transfer pumps market in the United States is expanding due to strong demand for vehicles equipped with durable fuel systems and high operational performance. The market is supported by a large vehicle base and extended usage cycles, which contribute to consistent replacement demand. Well-established service networks and a strong aftermarket ecosystem are further driving growth, as maintenance requirements for fuel system components continue to rise over time.

Key players operating in the Global Automotive Fuel Transfer Pumps Market include Robert Bosch, Denso, Continental Automotive, Delphi Technologies, Aisin Seiki, Mitsubishi Electric, TI Fluid Systems, Carter Fuel Systems, and Pierburg (Rheinmetall). Companies in the Global Automotive Fuel Transfer Pumps Market are strengthening their competitive position through continuous innovation and strategic expansion initiatives. Many players are investing in advanced pump technologies to improve efficiency, durability, and performance under demanding conditions. Collaborations with automotive manufacturers are enabling better integration of fuel systems within modern vehicle architectures. Companies are also expanding production capacities to meet rising global demand while optimizing cost structures. In addition, a strong focus on aftermarket services and distribution networks is helping companies capture long-term revenue opportunities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Vehicle

- 2.2.4 Fuel

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Growing commercial vehicle and logistics fleet

- 3.2.1.3 Expansion of automotive aftermarket demand

- 3.2.1.4 Increasing fuel injection system adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid shift toward electric vehicles

- 3.2.2.2 Fuel price volatility affecting vehicle usage

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging automotive markets

- 3.2.3.2 Development of high-efficiency electric fuel pumps

- 3.2.3.3 Expansion of biofuel and alternative fuel vehicles

- 3.2.3.4 Increasing demand from off-road and industrial vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 EPA Fuel System Regulations

- 3.4.1.2 CARB (California Air Resources Board) Standards

- 3.4.2 Europe

- 3.4.2.1 Euro 6 / Euro 7 Emission Standards

- 3.4.2.2 ECE R67 / R110 Fuel System Regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China VI Emission Standards

- 3.4.3.2 Japan JIS Fuel System Standards / JARI Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil PROCONVE

- 3.4.4.2 ABNT NBR Fuel System Standards

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE ESMA Fuel System & Emission Standards

- 3.4.5.2 South Africa SABS Fuel System Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by primary research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by primary research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Trade data analysis (Driven by paid database)

- 3.14.1 Import/export volume & value trends

- 3.14.2 Key trade corridors & tariff impact

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Mn, Million Units)

- 5.1 Key trends

- 5.2 Mechanical

- 5.3 Electrical

Chapter 6 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Ethanol/Biofuels

- 6.5 LPG/CNG

- 6.6 Other Alternative Fuels

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Million Units)

- 7.1 Key trends

- 7.2 Passenger car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two-wheelers

Chapter 8 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 OEM (Original Equipment Manufacturer)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Aisin Seiki

- 10.1.2 Continental Automotive

- 10.1.3 Delphi Technologies

- 10.1.4 Denso

- 10.1.5 Hitachi Astemo

- 10.1.6 Magnetti Marelli

- 10.1.7 Mitsubishi Electric

- 10.1.8 Pierburg (Rheinmetall)

- 10.1.9 Robert Bosch

- 10.1.10 TI Fluid Systems

- 10.2 Regional players

- 10.2.1 Airtex Pumps

- 10.2.2 Carter Fuel Systems

- 10.2.3 GMB

- 10.2.4 Spectra Premium

- 10.2.5 Stanadyne

- 10.2.6 UFI Filters

- 10.2.7 Walbro

- 10.3 Emerging players

- 10.3.1 Cummins Fuel Systems

- 10.3.2 Edelbrock

- 10.3.3 Holley Performance Products