|

시장보고서

상품코드

2019097

액체 포장용 카톤 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Liquid Packaging Cartons Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

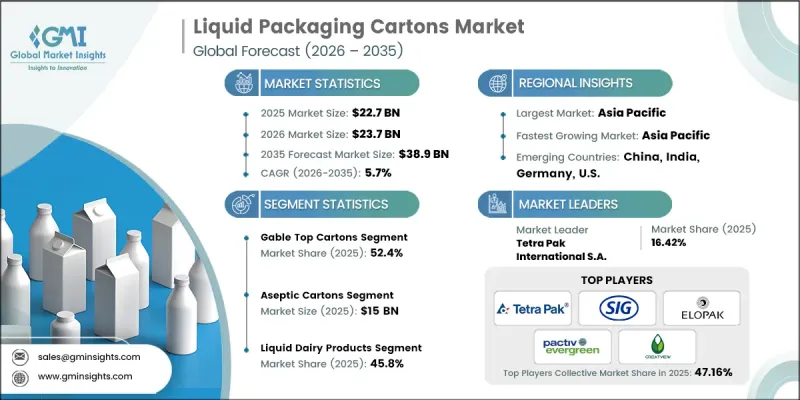

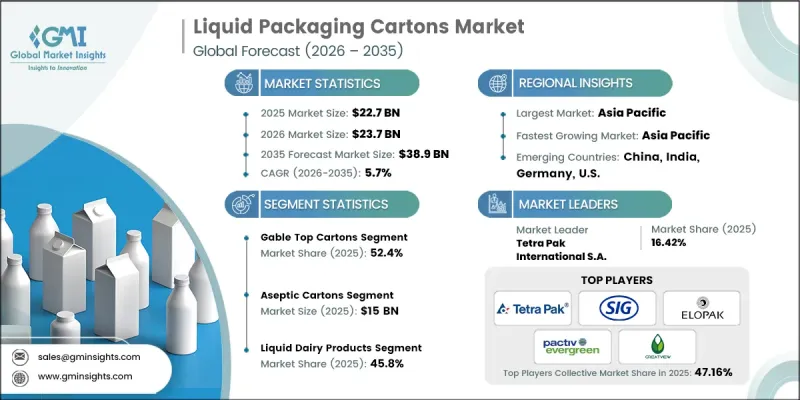

세계의 액체용 카톤 시장은 2025년에 227억 달러로 평가되었으며, CAGR 5.7%로 성장하여 2035년까지 389억 달러에 달할 것으로 추정됩니다.

시장 성장은 소비자 구매 행동의 급격한 변화, 특히 디지털 소매 채널의 영향력 증가에 의해 주도되고 있습니다. 편리하고 내구성이 뛰어나며 지속가능한 포장 솔루션에 대한 수요가 증가함에 따라 음료 및 신선 식품용 액체 카톤의 채택이 가속화되고 있습니다. 동시에 전 세계 즉석음료 제품의 소비 증가도 시장 확대에 크게 기여하고 있습니다. 라이프스타일의 변화, 도시화의 진전, 건강에 대한 인식이 높아짐에 따라 소비자들은 포장된 음료를 선택하게 되었습니다. 이것이 효율적인 패키지 형태에 대한 수요를 뒷받침하고 있습니다. 제조업체들은 지속가능성 목표와 규제 요건을 충족하기 위해 경량화 및 친환경 솔루션 개발에 점점 더 많은 노력을 기울이고 있습니다. 환경 친화적인 대체 패키지로의 전환은 기업이 제품의 안전성과 편의성을 유지하면서 환경에 미치는 영향을 줄이기 위해 노력하는 가운데 업계 내 혁신을 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 227억 달러 |

| 예측 규모 | 389억 달러 |

| CAGR | 5.7% |

브릭 카톤 부문은 2035년까지 CAGR 4.5%로 성장할 것으로 예상되며, 액체 포장용 카톤 시장에서 확고한 입지를 유지할 것으로 예상됩니다. 이 형태는 구조적 강도, 효율적인 보관 능력 및 제품 보관 기간을 연장할 수 있다는 점에서 널리 선호되고 있습니다. 첨단 패키징 기술의 채택 확대가 이 부문의 성장을 뒷받침하고 있습니다. 특히 장기간에 걸쳐 제품의 품질을 유지하는 데 효과적이라는 점이 그 요인입니다. 이 카톤의 디자인은 안전성을 보장하고 오염 위험을 줄이면서 제품 품질을 유지하는 데 도움이 되며, 액체 포장 응용 분야에서 신뢰할 수 있는 선택이 됩니다.

2025년 기준, 액체 유제품 부문은 45.8%의 점유율을 차지했습니다. 우유 음료에 대한 전 세계 수요 증가는 이 부문의 우위를 지속적으로 뒷받침하고 있습니다. 부가가치가 높은 유제품의 도입이 진행됨에 따라 각 제조사들은 제품의 유통기한을 연장할 수 있는 첨단 패키징을 도입하고 있습니다. 높은 장벽 성능을 갖춘 고성능 카톤 구조가 선호되고 있으며, 이는 신선도를 유지하면서 외부 보관 조건에 대한 의존도를 낮추는 데 도움이 되기 때문입니다.

2025년 북미 액체 포장용 카톤 시장은 27.9%의 점유율을 차지했습니다. 이 지역에서는 환경에 미치는 영향을 줄이기 위한 소비자의 인식 제고와 규제 조치로 인해 보다 지속가능하고 재활용 가능한 포장 솔루션으로의 전환이 진행되고 있습니다. 생분해성 및 퇴비화 가능한 재료의 개발과 함께 플라스틱 함량이 낮은 포장에 대한 수요가 증가하고 있습니다. 식품 안전성 향상, 지속가능성 강화, 재활용 효율성 향상에 초점을 맞춘 업계 전반의 노력은 시장 성장을 더욱 촉진하고 있습니다. 혁신적인 포장 기술과 친환경 소재에 대한 지속적인 투자로 세계 시장에서 이 지역의 입지를 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 카톤 유형별, 2022-2035

제6장 시장 추정 및 예측 : 보존 기간 기술별, 2022-2035

제7장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추정 및 예측 : 지역별, 2022-2035

제9장 기업 개요

KSM 26.05.06The Global Liquid Packaging Cartons Market was valued at USD 22.7 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 38.9 billion by 2035.

Market growth is driven by the rapid evolution of consumer purchasing behavior, particularly with the increasing influence of digital retail channels. The growing demand for convenient, durable, and sustainable packaging solutions is accelerating the adoption of liquid cartons for packaged beverages and perishable goods. At the same time, rising global consumption of ready-to-consume liquid products is contributing significantly to market expansion. Changing lifestyle patterns, increasing urbanization, and heightened health awareness are encouraging consumers to choose packaged beverages, which in turn is supporting demand for efficient packaging formats. Manufacturers are increasingly focusing on developing lightweight and environmentally responsible solutions to align with sustainability goals and regulatory expectations. The shift toward eco-conscious packaging alternatives is also shaping innovation within the industry, as companies aim to reduce environmental impact while maintaining product safety and convenience.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.7 Billion |

| Forecast Value | $38.9 Billion |

| CAGR | 5.7% |

The brick cartons segment is expected to grow at a CAGR of 4.5% through 2035, maintaining a strong position within the liquid packaging cartons market. This format is widely preferred due to its structural strength, efficient storage capabilities, and ability to extend product shelf life. Increasing adoption of advanced packaging technologies is supporting the segment's growth, particularly due to its effectiveness in preserving product quality over extended durations. The design of these cartons helps maintain product integrity while ensuring safety and reducing contamination risks, making them a reliable choice for liquid packaging applications.

The liquid dairy products segment accounted for 45.8% share in 2025. Strong global demand for dairy-based beverages continues to support this segment's dominance. The introduction of value-added and enhanced dairy offerings is encouraging manufacturers to adopt advanced packaging solutions that improve product longevity. High-performance carton structures with advanced barrier properties are gaining preference, as they help maintain freshness while reducing dependency on external storage conditions.

North America Liquid Packaging Cartons Market held a 27.9% share in 2025. The region is experiencing a transition toward more sustainable and recyclable packaging solutions, driven by increasing consumer awareness and regulatory initiatives aimed at reducing environmental impact. The demand for packaging with lower plastic content is rising, alongside the development of biodegradable and compostable materials. Industry-wide efforts focused on improving food safety, enhancing sustainability, and increasing recycling efficiency are further supporting market growth. Continuous investments in innovative packaging technologies and eco-friendly materials are strengthening the region's position within the global landscape.

Key companies operating in the Global Liquid Packaging Cartons Market include Elopak AS, Greatview Aseptic Packaging Co. Ltd., IPI Srl (Coesia), Klabin S.A., Lami Packaging (Kunshan) Co. Ltd., Nampak Ltd., Nippon Paper Industries Co. Ltd., Oji Holdings Corporation, Pactiv Evergreen Inc., Parksons Packaging Ltd., SIG Combibloc Group AG, Smurfit Kappa Group plc, Stora Enso Oyj, Tetra Pak International S.A., TidePak Aseptic Packaging Material Co. Ltd., UFlex Limited (ASEPTO), and Visy Industries. Companies in the Global Liquid Packaging Cartons Market are strengthening their market position through innovation, sustainability initiatives, and strategic expansion. A key focus is being placed on developing recyclable and biodegradable packaging materials to align with evolving environmental regulations and consumer preferences. Firms are investing in advanced manufacturing technologies to enhance product durability and efficiency while reducing material usage. Strategic partnerships and collaborations help companies expand their geographic reach and improve distribution capabilities. Additionally, organizations are focusing on product differentiation through improved design and functionality.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Carton type trends

- 2.2.2 Shelf-life technology trends

- 2.2.3 End-use application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing consumption of packaged beverages

- 3.2.1.2 Rising demand for sustainable and eco-friendly packaging solutions

- 3.2.1.3 Growth in dairy product consumption

- 3.2.1.4 Expansion of e-commerce and home delivery services

- 3.2.1.5 Growth in the ready-to-drink (RTD) beverage market

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial production and recycling costs

- 3.2.2.2 Limited suitability for carbonated beverages

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of advanced smart and functional packaging technologies

- 3.2.3.2 Increasing penetration in emerging regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Carton Type, 2022 - 2035 (USD Billion & Kilo tons)

- 5.1 Key trends

- 5.2 Gable top cartons

- 5.2.1 Standard gable top

- 5.2.2 Fresh-lock gable top with reclosable cap

- 5.2.3 Slim gable top

- 5.3 Brick cartons

- 5.3.1 Standard brick

- 5.3.2 Slim brick

- 5.3.3 Square brick

- 5.4 Shaped cartons

- 5.4.1 Carton bottles

- 5.4.2 Custom shaped cartons

Chapter 6 Market Estimates and Forecast, By Shelf-Life Technology, 2022 - 2035 (USD Billion & Kilo tons)

- 6.1 Key trends

- 6.2 Aseptic cartons

- 6.2.1 Uht-compatible aseptic systems

- 6.2.2 Extended shelf life (ESL) aseptic systems

- 6.3 Non-aseptic cartons

- 6.3.1 Pasteurized product cartons

- 6.3.2 Fresh/chilled distribution cartons

Chapter 7 Market Estimates and Forecast, By End-Use Application, 2022 - 2035 (USD Billion & Kilo tons)

- 7.1 Key trends

- 7.2 Liquid dairy products

- 7.2.1 Fresh milk

- 7.2.2 Flavored milk

- 7.2.3 Liquid yogurt

- 7.2.4 Cream & buttermilk

- 7.2.5 Others

- 7.3 Non-carbonated soft drinks

- 7.3.1 Fruit juices & nectars

- 7.3.2 Iced tea & lemonades

- 7.3.3 Plant-based beverages

- 7.3.4 Sports & energy drinks

- 7.4 Liquid foods

- 7.4.1 Soups & broths

- 7.4.2 Sauces & cooking stocks

- 7.4.3 Liquid eggs & dairy alternatives

- 7.5 Other liquids

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion & Kilo tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global players

- 9.1.1 Elopak AS

- 9.1.2 Greatview Aseptic Packaging Co. Ltd.

- 9.1.3 Pactiv Evergreen Inc.

- 9.1.4 SIG Combibloc Group AG

- 9.1.5 Smurfit Kappa Group plc

- 9.1.6 Stora Enso Oyj

- 9.1.7 Tetra Pak International S.A.

- 9.2 Regional Champions

- 9.2.1 Klabin S.A.

- 9.2.2 Nampak Ltd.

- 9.2.3 Nippon Paper Industries Co. Ltd.

- 9.2.4 Oji Holdings Corporation

- 9.2.5 Visy Industries

- 9.3 Emerging Players

- 9.3.1 IPI Srl (Coesia)

- 9.3.2 Lami Packaging (Kunshan) Co. Ltd.

- 9.3.3 Parksons Packaging Ltd.

- 9.3.4 TidePak Aseptic Packaging Material Co. Ltd.

- 9.3.5 UFlex Limited (ASEPTO)