|

시장보고서

상품코드

2019131

선박용 엔진 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Marine Engines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

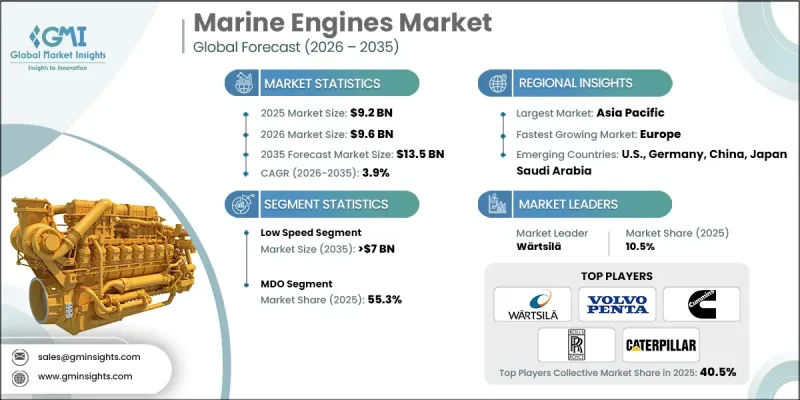

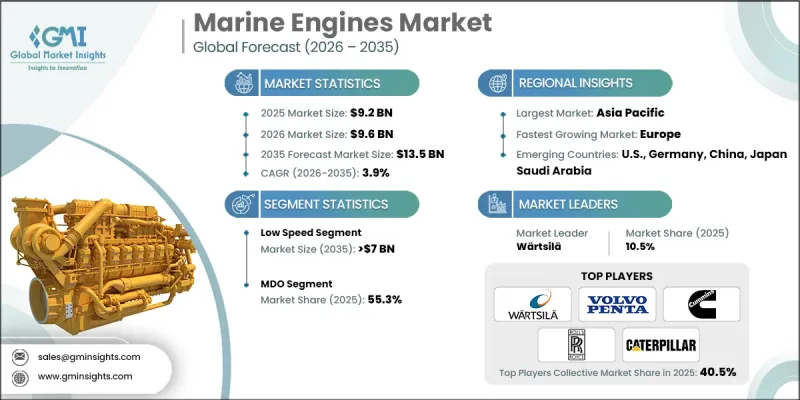

세계의 선박용 엔진 시장은 2025년에 92억 달러로 평가되었고, CAGR 3.9%로 성장하여 2035년까지 135억 달러에 이를 것으로 추정되고 있습니다.

이 산업은 각국의 경쟁력에 영향을 미치는 물류 구조, 가격 전략, 공급망 조정 등 국제 해운 무역의 변화하는 요인에 의해 형성되고 있습니다. 세계 상품 무역의 확대와 경제 성장으로 선박용 추진 시스템에 대한 수요는 더욱 증가할 것으로 예측됩니다. 선박용 엔진은 선박 성능의 핵심으로 소형 선박부터 대형 화물선까지 다양한 유형의 선박에 필요한 출력과 효율을 제공합니다. 설계 시 염수, 진동, 가혹한 기상 조건 등 혹독한 해양 환경에 대한 내구성을 확보해야 합니다. 시장 동향은 연료 효율성, 엔진의 현대화, 그리고 환경적으로 지속 가능한 솔루션에 중점을 두고 있습니다. 또한, 상업, 국방, 레저 분야에서의 해상 활동 확대가 고성능, 고신뢰성 엔진에 대한 수요를 견인하고 있으며, 선대의 현대화 및 무역량 증가는 전체 시장의 잠재력을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 92억 달러 |

| 예측액 | 135억 달러 |

| CAGR | 3.9% |

저속 선박용 엔진 시장은 항만 개발 및 예인선 및 소형 선박에 대한 수요 증가를 배경으로 2035년까지 70억 달러에 달할 것으로 예측됩니다. 이들 엔진은 대부분 기통수가 적은 4행정 엔진으로 컴팩트한 디자인과 높은 성능으로 평가받고 있습니다. 크기가 작아 설치가 용이하면서도 운영 효율을 유지할 수 있어 페리, 요트, 어선에 적합합니다. 컴팩트함과 신뢰성을 겸비하여 다양한 선박 응용 분야에서 채택이 계속 확대되고 있습니다.

MDO(선박용 디젤유) 엔진 부문은 2025년 55.3%의 점유율을 차지할 것으로 예상되며, 고속 성능, 저소음, 대규모 생산에 대한 적합성 등으로 인해 성장세를 보이고 있습니다. 이 엔진은 움직이는 부품이 적고, 연료 효율이 높으며, 배기가스 배출이 적고, 추가 윤활유가 필요하지 않아 비용 효율성이 뛰어나 상업용 및 산업용 선박에 매력적인 선택이 될 수 있습니다.

미국 선박용 엔진 시장은 선박의 운영 신뢰성에 대한 수요 증가, 디젤 엔진의 성능 요구 사항 향상, 해운 산업의 확장에 힘입어 2025년 8억 9,010만 달러 규모에 달할 것으로 예측됩니다. 또한, 경제의 안정, 엔진 효율에 대한 수요 증가, 편안함과 고성능 선박 솔루션에 대한 관심은 이 지역 시장 성장을 더욱 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모와 예측 : 제품별, 2022-2035

제6장 시장 규모와 예측 : 출력별, 2022-2035

제7장 시장 규모와 예측 : 기술별, 2022-2035

제8장 시장 규모와 예측 : 추진력별, 2022-2035

제9장 시장 규모와 예측 : 용도별, 2022-2035

제10장 시장 규모와 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.05.08The Global Marine Engines Market was valued at USD 9.2 billion in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 13.5 billion by 2035.

The industry is being shaped by evolving factors in international maritime trade, including logistics structures, pricing strategies, and supply chain adjustments, which influence the competitiveness of countries. Expanding global merchandise trade and economic growth are expected to further energize demand for marine propulsion systems. Marine engines are central to vessel performance, providing the necessary power and efficiency for various types of boats, from small crafts to large cargo carriers. Their design must ensure durability against harsh marine environments, including saltwater, vibrations, and extreme weather. Market trends emphasize fuel efficiency, engine modernization, and environmentally sustainable solutions. Additionally, the growth of commercial, defense, and leisure maritime activities drives the need for high-performance, reliable engines, while fleet modernization and increasing trade volumes enhance overall market potential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.2 Billion |

| Forecast Value | $13.5 Billion |

| CAGR | 3.9% |

The low-speed marine engines segment is expected to reach USD 7 billion by 2035, driven by seaport development and growing demand for tugboats and smaller vessels. These engines, often four-stroke with fewer cylinders, are valued for their compact design and high performance. Their smaller size allows easier installation while maintaining operational efficiency, making them ideal for ferries, yachts, and fishing boats. The combination of compactness and reliability continues to boost adoption across multiple marine applications.

The MDO (marine diesel oil) engine segment accounted for a 55.3% share in 2025 and is gaining momentum due to its high-speed capabilities, low noise levels, and suitability for large-scale production. These engines are cost-efficient with fewer moving parts, improved fuel efficiency, reduced emissions, and no need for additional lubricants, which makes them an attractive choice for commercial and industrial vessels.

U.S. Marine Engines Market was valued at USD 890.1 million in 2025, driven by the rising demand for operational reliability in vessels, increased diesel engine performance requirements, and the expansion of the maritime transportation industry. Additionally, economic stability, rising demand for engine efficiency, and a focus on comfort and high-performance marine solutions are further accelerating market growth in the region.

Key players in the Global Marine Engines Market include Wartsila, Rolls-Royce, Cummins, Hyundai Heavy Industries, Mitsubishi Heavy Industries, AB Volvo Penta, Caterpillar, Scania, YANMAR HOLDINGS, Mercury Marine, IHI Corporation, Societe Internationale des Moteurs Baudouin, Weichai Holding Group, DAIHATSU INFINEARTH, STX Engines, Deere & Company, Shanghai Diesel Engine, JCW Acoustic Flooring, Anglo Belgian Corporation, Everllence, and Yamaha Motor. Companies in the Marine Engines Market are leveraging several strategies to strengthen their market foothold. These include continuous investment in research and development to enhance fuel efficiency, durability, and environmental compliance of engines. Strategic partnerships with shipbuilders, maritime service providers, and global distributors help expand market reach. Companies are also focusing on product innovation, introducing hybrid and low-emission engines to meet regulatory requirements and attract environmentally conscious buyers. Marketing efforts emphasize reliability, performance, and lifecycle cost efficiency. Geographic expansion into emerging markets, coupled with after-sales services, maintenance programs, and customer training initiatives, further strengthens brand loyalty and market positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates and forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Power trends

- 2.1.4 Technology trends

- 2.1.5 Propulsion trends

- 2.1.6 Application trends

- 2.1.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/Unit)

- 3.5.1 By region

- 3.5.2 By power

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of marine engines

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 MDO

- 5.3 MGO

- 5.4 LNG

- 5.5 Hybrid

- 5.6 Others

Chapter 6 Market Size and Forecast, By Power, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 < 1,000 HP

- 6.3 1,000 - 5,000 HP

- 6.4 5,001 - 10,000 HP

- 6.5 10,001 - 20,000 HP

- 6.6 > 20,000 HP

Chapter 7 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 Medium speed

- 7.4 High speed

Chapter 8 Market Size and Forecast, By Propulsion, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 2 Stroke

- 8.3 4 Stroke

Chapter 9 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Merchant

- 9.2.1 Container vessels

- 9.2.2 Tankers

- 9.2.3 Bulk carriers

- 9.2.4 Gas carriers

- 9.2.5 RO-RO

- 9.2.6 Others

- 9.3 Offshore

- 9.3.1 Drilling rigs & ships

- 9.3.2 Anchor handling vessels

- 9.3.3 Offshore support vessels

- 9.3.4 Floating production units

- 9.3.5 Platform supply vessels

- 9.4 Cruise & ferry

- 9.4.1 Cruise vessels

- 9.4.2 Passenger ferries

- 9.4.3 Passenger/cargo vessels

- 9.4.4 Others

- 9.5 Navy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 Norway

- 10.3.5 France

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Vietnam

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Angola

- 10.5.5 Egypt

- 10.5.6 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 AB Volvo Penta

- 11.2 Anglo Belgian Corporation

- 11.3 Caterpillar

- 11.4 Cummins

- 11.5 DAIHATSU INFINEARTH MFG. CO., LTD.

- 11.6 DEUTZ

- 11.7 Deere & Company

- 11.8 Everllence

- 11.9 Hyundai Heavy Industries

- 11.10 IHI Corporation

- 11.11 Mercury Marine

- 11.12 Mitsubishi Heavy Industries

- 11.13 Rolls-Royce

- 11.14 Societe Internationale des Moteurs Baudouin

- 11.15 Scania

- 11.16 Shanghai Diesel Engine

- 11.17 STX Engines

- 11.18 Wartsila

- 11.19 Weichai Holding Group Co., Ltd.

- 11.20 Yamaha Motor Co., Ltd.

- 11.21 YANMAR HOLDINGS CO., LTD.

- 11.22 Yuchai International