|

시장보고서

상품코드

2019156

친환경 식품 포장 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Eco-friendly Food Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

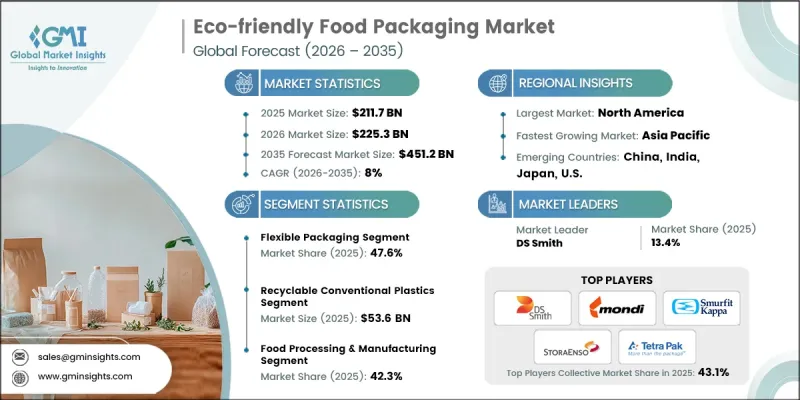

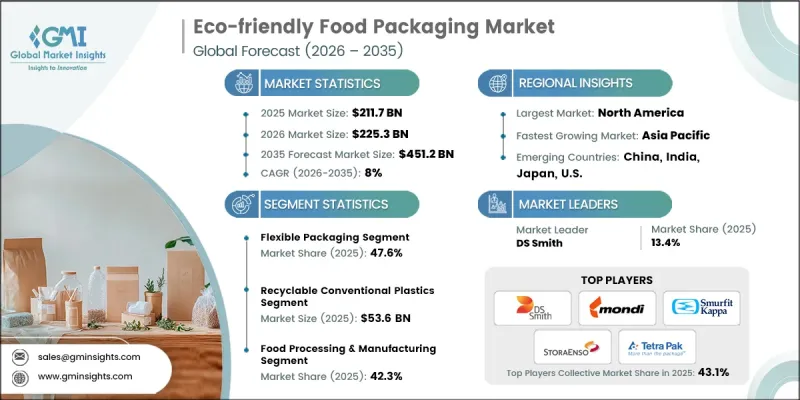

세계의 친환경 식품 포장 시장은 2025년에 2,117억 달러로 평가되었고, CAGR 8%로 성장하여 2035년까지 4,512억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 플라스틱 폐기물 감소를 위한 규제 프레임워크 강화와 더불어 식음료 산업 전반에 걸쳐 지속 가능한 포장 솔루션의 채택이 확대되면서 성장세를 견인하고 있습니다. 친환경 대체품에 대한 수요 증가와 음식 배달 서비스의 급속한 확장과 함께 재활용 및 퇴비화 가능한 재료로의 전환이 가속화되고 있습니다. 바이오 포장 기술의 지속적인 혁신은 제품의 성능과 지속가능성 향상에 기여하고 있습니다. 각 제조업체들은 포장의 효율성과 내구성을 유지하면서 환경에 미치는 영향을 줄이는 데 주력하고 있습니다. 순환 경제의 실천이 점점 더 중요시되는 가운데, 기업들은 재사용 또는 재활용 가능한 재료를 효율적으로 재사용하거나 재활용할 수 있도록 장려하고 있습니다. 또한, 지속 가능한 소비 패턴으로의 전환으로 환경 친화적인 포장 형태에 대한 수요가 증가함에 따라 친환경 식품 포장은 전 세계 공급망 전반에서 중요한 중점 분야가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 2,117억 달러 |

| 예측 금액 | 4,512억 달러 |

| CAGR | 8% |

주요 경제권에서 일회용 플라스틱에 대한 규제가 강화됨에 따라 친환경 식품 포장 산업은 강력한 모멘텀을 보이고 있습니다. 규제 당국은 환경에 미치는 영향을 최소화하기 위해 보다 엄격한 규정 준수 기준을 시행하고 있으며, 이로 인해 기업들은 지속 가능한 대안으로 전환해야 하는 상황에 직면해 있습니다. 동시에 음료 및 식품 제조업체들은 재활용 및 퇴비화 가능한 재료를 사용하여 더 높은 지속가능성 목표를 달성하기 위해 노력하고 있습니다. 기업들이 기존 플라스틱 패키지를 대체하기 위해 섬유 및 종이 기반 패키지 솔루션으로 전환하는 추세에 따라 섬유 및 종이 기반 패키지 솔루션으로의 전환이 가속화되고 있습니다. 업계 관계자들은 재료의 회수 및 재사용에 중점을 두어 포장 전략을 순환 경제 원칙에 점점 더 적합하게 만들고 있습니다. 이러한 전환은 제품 개발 및 공급망 전략을 재구성하고 지속 가능한 소재의 적용에 대한 혁신을 촉진하고 있습니다.

연포장 부문은 경량 구조, 재료 사용량 감소, 비용 효율성으로 인해 2025년 47.6%의 점유율을 차지할 것으로 예측됩니다. 이 포장 형태는 제품의 보존성 향상과 물류 최적화를 지원하며, 식품 공급망 전반에 걸쳐 폭넓게 채택되고 있습니다. 재활용 가능한 단일 재료 구조와 지속 가능한 라미네이트 솔루션의 지속적인 발전은 그 매력을 더욱 높이고 있습니다. 성능과 환경 보호의 균형을 맞추는 능력은 연포장 솔루션에 대한 견고한 수요를 지속적으로 견인하고 있습니다.

재활용 가능한 재래식 플라스틱 부문은 2025년 536억 달러 시장 규모를 기록할 것으로 예측됩니다. 이 부문은 지속가능성과 기능성의 실용적인 균형을 제공하기 때문에 여전히 중요한 위치를 차지하고 있습니다. 잘 구축된 재활용 인프라, 비용적 우위, 기존 생산 시스템과의 호환성이 그 지속적인 활용을 뒷받침하고 있습니다. 이 카테고리의 소재는 효과적인 제품 보호와 유통기한 연장을 실현하고, 규제 요건을 준수하며, 순환 경제에 기여하고 있습니다.

북미 친환경 식품 포장 시장은 규제 압력과 기업의 지속가능성에 대한 관심 증가에 힘입어 2025년 46.2%의 점유율을 차지할 것으로 예측됩니다. 이 지역에서는 식품 관련 산업 전반에 걸쳐 재활용, 퇴비화 및 섬유 기반 포장 형태가 널리 채택되고 있습니다. 첨단 소재와 포장 기술에 대한 투자로 혁신 역량을 강화하고 있습니다. 식품 소매, 포장 상품 및 배달 서비스 수요 증가가 시장 확대를 뒷받침하고 있으며, 2035년까지 이 지역은 지속 가능한 포장 도입에 있어 선도적인 위치를 차지할 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별, 2022-2035

제6장 시장 추산 및 예측 : 포장 형태별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 최종사용자별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.05.08The Global Eco-friendly Food Packaging Market was valued at USD 211.7 billion in 2025 and is estimated to grow at a CAGR of 8% to reach USD 451.2 billion by 2035.

Market growth is driven by stricter regulatory frameworks aimed at reducing plastic waste, along with the rising adoption of sustainable packaging solutions across the food and beverage sector. Increasing demand for environmentally responsible alternatives, combined with rapid expansion in food delivery services, is accelerating the transition toward recyclable and compostable materials. Continuous innovation in bio-based packaging technologies is also enhancing product performance and sustainability credentials. Manufacturers are focusing on reducing environmental impact while maintaining packaging efficiency and durability. The growing emphasis on circular economy practices is encouraging companies to adopt materials that can be reused or recycled efficiently. In addition, the shift toward sustainable consumption patterns is reinforcing demand for eco-conscious packaging formats, making eco-friendly food packaging a key focus area across global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $211.7 Billion |

| Forecast Value | $451.2 Billion |

| CAGR | 8% |

The eco-friendly food packaging industry is experiencing strong momentum due to tightening regulations targeting single-use plastics across major economies. Regulatory bodies are enforcing stricter compliance standards to minimize environmental impact, prompting companies to transition toward sustainable alternatives. At the same time, food and beverage manufacturers are committing to higher sustainability targets by adopting recyclable and compostable materials. The shift toward fiber-based and paper-based packaging solutions is gaining traction as businesses aim to replace traditional plastic formats. Industry participants are increasingly aligning their packaging strategies with circular economy principles, focusing on material recovery and reuse. This transition is reshaping product development and supply chain strategies, encouraging innovation in sustainable material applications.

The flexible packaging segment accounted for 47.6% share in 2025 owing to its lightweight structure, reduced material usage, and cost efficiency. This packaging format supports improved product preservation and optimized logistics, contributing to its widespread adoption across the food supply chain. Ongoing advancements in recyclable mono-material structures and sustainable laminate solutions are further enhancing its appeal. The ability to balance performance with environmental considerations continues to drive strong demand for flexible packaging solutions.

The recyclable conventional plastics segment generated USD 53.6 billion in 2025. This segment remains prominent as it offers a practical balance between sustainability and functionality. Established recycling infrastructure, cost advantages, and compatibility with existing production systems support its continued use. Materials within this category provide effective product protection, extend shelf life, and comply with regulatory requirements while contributing to circular economy initiatives.

North America Eco-friendly Food Packaging Market held a 46.2% share in 2025, supported by regulatory pressure and increasing corporate focus on sustainability. The region is witnessing the broad adoption of recyclable, compostable, and fiber-based packaging formats across food-related industries. Investments in advanced materials and packaging technologies are strengthening innovation capabilities. Growing demand from food retail, packaged goods, and delivery services is sustaining market expansion, positioning the region as a leader in sustainable packaging adoption through 2035.

Key companies operating in the Global Eco-friendly Food Packaging Market include Amcor, Biomass Packaging, Biopak, DS Smith, Elopak, Genpak, Huhtamaki, International Paper, Karl Knauer, Mondi, Nordic Paper, PacknWood, Smurfit Kappa, Sonoco Products, Stora Enso, Sulapac, Tetra Pak, TIPA, Vegware, and WestRock. Companies in the Global Eco-friendly Food Packaging Market are strengthening their competitive position through innovation, strategic partnerships, and sustainability-driven initiatives. Many firms are investing in research and development to create advanced bio-based and recyclable materials that meet performance and regulatory standards. Businesses are forming collaborations across the value chain to enhance recycling infrastructure and support circular economy models. Expansion of product portfolios with sustainable alternatives is helping companies address evolving consumer preferences. In addition, organizations are leveraging digital technologies to improve supply chain transparency and operational efficiency. Companies are also focusing on sustainable sourcing, eco-friendly manufacturing processes, and compliance with global environmental regulations to reinforce brand positioning and long-term market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Packaging format trends

- 2.2.3 Application trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent single-use plastic bans across EU, India, North America

- 3.2.1.2 FMCG brands adopting recyclable and compostable packaging targets

- 3.2.1.3 E-commerce food delivery driving need for biodegradable packaging

- 3.2.1.4 Corporate ESG commitments accelerating packaging material transitions

- 3.2.1.5 Advancements in bio-based polymers improving barrier performance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited industrial composting infrastructure in emerging economies

- 3.2.2.2 Performance limitations in moisture and oxygen barrier properties

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of molded fiber packaging in quick-service restaurants

- 3.2.3.2 Growth in reusable packaging systems for urban food delivery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Paper & paperboard

- 5.3 Recyclable conventional plastics

- 5.4 Recycled plastics

- 5.5 Bio-based & biodegradable plastics

- 5.6 Metal

- 5.7 Glass

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.3 Flexible packaging

- 6.4 Semi-rigid packaging

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fresh food

- 7.3 Dairy products

- 7.4 Frozen food (including frozen desserts)

- 7.5 Processed food

- 7.6 Beverages

- 7.7 Sauces, dressings & condiments

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food processing & manufacturing

- 8.3 Foodservice operators

- 8.4 Retail & private label packaging

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor

- 10.1.2 DS Smith

- 10.1.3 Mondi

- 10.1.4 Smurfit Kappa

- 10.1.5 Stora Enso

- 10.1.6 Tetra Pak

- 10.1.7 Huhtamaki

- 10.1.8 Sonoco Products

- 10.1.9 WestRock

- 10.1.10 International Paper

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Genpak

- 10.2.2 Asia Pacific

- 10.2.2.1 Biopak

- 10.2.3 Europe

- 10.2.3.1 Elopak

- 10.2.3.2 Karl Knauer

- 10.2.3.3 Nordic Paper

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Biomass Packaging

- 10.3.2 PacknWood

- 10.3.3 Sulapac

- 10.3.4 TIPA

- 10.3.5 Vegware