|

시장보고서

상품코드

2019197

카카오콩 파생 제품 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Cocoa Bean Derivatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

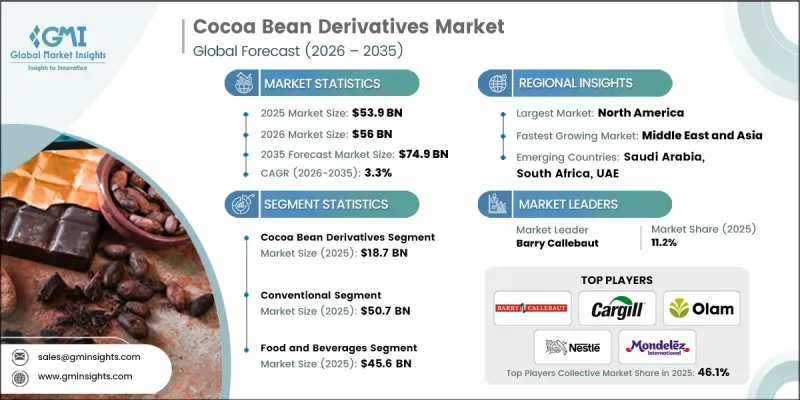

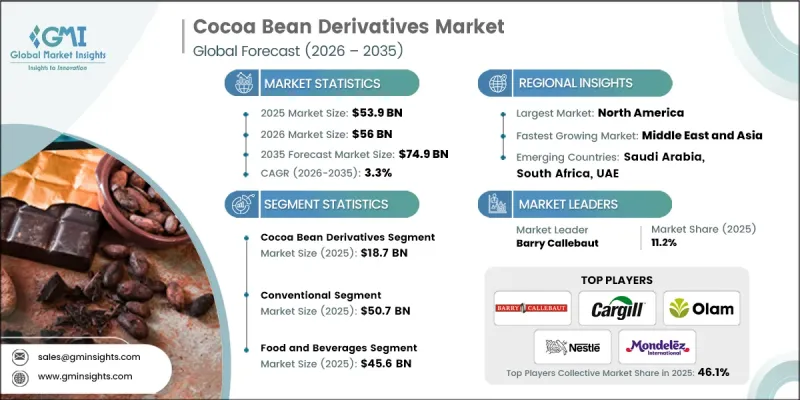

세계의 카카오콩 파생 제품 시장은 2025년에 539억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.3%로 성장하여 749억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 식음료, 퍼스널케어 및 산업 분야에서 카카오 기반 제품에 대한 수요 증가에 힘입은 바 큽니다. 코코아 리커, 코코아 버터, 코코아 파우더, 코코아 케이크, 코코아 껍질 제품별을 포함한 코코아 파생 제품은 건조, 로스팅, 분쇄 등 발효 후 공정을 통해 제조됩니다. 카카오 고형분과 카카오 버터로 구성된 반유동성 페이스트인 카카오 리커는 압착하여 카카오 케이크에서 카카오 버터를 분리한 후 가공하여 카카오 파우더로 만듭니다. 고급 로스팅, 유압 및 기계식 압착, 정밀 분쇄 시스템 등 최신 가공 기술을 통해 추출 효율, 맛의 일관성, 질감의 균일성을 향상시켰습니다. 이러한 혁신을 통해 제조업체는 공정 관리를 유지하고 생산 효율을 최적화하면서 다양한 산업 요구에 맞는 고품질 파생 제품을 생산할 수 있습니다.

| 시장 규모 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 539억 달러 |

| 예측액 | 749억 달러 |

| CAGR | 3.3% |

전통적인 코코아 파생 제품 부문은 2025년 507억 달러에 달할 것으로 예측됩니다. 이는 전 세계 식음료 및 퍼스널케어 산업에서 이러한 제품이 널리 채택되고 있음을 반영합니다. 이 제품들은 안정된 품질, 접근성, 비용 효율성으로 인해 초콜릿 제조, 베이커리 제품, 제과 및 기타 코코아 기반 식품의 기초가 되고 있습니다. 전통적인 코코아 파생 제품의 장점은 로스팅, 분쇄, 압착과 같은 확립된 가공 기술을 통해 대규모 생산에서 신뢰할 수 있는 맛, 질감 및 지방 함량을 보장하는 데 있습니다. 또한, 제조업체는 전통적인 코코아 원료를 선호합니다. 이는 대량 조달 및 표준화된 배합에 쉽게 통합할 수 있기 때문입니다.

2025년, 음료 및 식품 부문 시장 규모는 456억 달러에 달할 것입니다. 코코아 유래 제품은 초콜릿, 베이커리, 유제품, 음료 제품에 필수적인 맛, 질감, 색상, 안정성을 제공함으로써 기여하고 있습니다. 식품 분야 외에도 코코아 버터는 보습과 피부 유연화를 목적으로 퍼스널케어 제품에 널리 사용되고 있으며, 코코아 파생 제품은 뉴트리슈티컬, 의약품, 산업 공정에도 적용되어 다양한 분야에서 다재다능함을 보여주고 있습니다.

북미 코코아 원두 파생 제품 시장은 2025년 159억 달러에서 2035년 217억 달러로 강력한 성장세를 보일 것으로 예측됩니다. 이 지역은 첨단 가공 인프라, 탄탄한 소매 및 전자상거래 채널, 기능성 및 프리미엄 카카오 제품에 대한 수요 증가의 혜택을 누리고 있습니다. 미국에서는 스페셜티 초콜릿, 클린 라벨 제품, 유기농 제품에서 코코아 버터와 코코아 파우더의 사용이 증가하고 있으며, 이것이 시장을 주도하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035

제6장 시장 추산 및 예측 : 카테고리별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.05.08The Global Cocoa Bean Derivatives Market was valued at USD 53.9 billion in 2025 and is estimated to grow at a CAGR of 3.3% to reach USD 74.9 billion by 2035.

Growth is driven by the rising demand for cocoa-based products across food, beverage, personal care, and industrial applications. Cocoa derivatives, including cocoa liquor, cocoa butter, cocoa powder, cocoa cake, and cocoa shell by-products, are produced through post-fermentation processes such as drying, roasting, and grinding. Cocoa liquor, a semi-liquid paste of cocoa solids and cocoa butter, is pressed to separate cocoa butter from cocoa cake, which is further processed into cocoa powder. Modern processing technologies, including advanced roasting, hydraulic and mechanical pressing, and precise grinding systems, enhance extraction efficiency, flavor consistency, and texture uniformity. These innovations allow manufacturers to produce high-quality derivatives tailored to diverse industrial needs while maintaining process control and optimizing production efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.9 Billion |

| Forecast Value | $74.9 Billion |

| CAGR | 3.3% |

The conventional cocoa derivatives segment reached USD 50.7 billion in 2025, reflecting their widespread adoption across the global food, beverage, and personal care industries. These products remain the backbone of chocolate manufacturing, bakery items, confectionery, and other cocoa-based foods due to their consistent quality, availability, and cost-effectiveness. The dominance of conventional cocoa derivatives is supported by established processing techniques, including roasting, grinding, and pressing, which ensure reliable flavor, texture, and fat content for large-scale production. Additionally, manufacturers prefer conventional cocoa ingredients because they are easier to source in bulk and integrate into standardized formulations.

The food & beverage segment captured USD 45.6 billion in 2025. Cocoa derivatives contribute to chocolate, bakery, dairy, and beverage products by providing essential taste, texture, color, and stability. Beyond food, cocoa butter is widely used in personal care products for hydration and skin softening, while cocoa derivatives also find applications in nutraceuticals, pharmaceuticals, and industrial processes, demonstrating their versatility across multiple sectors.

North America Cocoa Bean Derivatives Market is projected to witness strong growth from USD 15.9 billion in 2025 to USD 21.7 billion in 2035. The region benefits from advanced processing infrastructure, robust retail and e-commerce channels, and increasing demand for functional and premium cocoa products. The United States drives the market through rising use of cocoa butter and powder in specialty chocolates, clean-label, and organic offerings.

Prominent players in the Global Cocoa Bean Derivatives Market include Barry Callebaut, Ferrero, Mondelez International, Nestle, Cargill, Cocoa Touton, ECOM Agroindustrial, Natra, JB Foods, Moner Cocoa, Indcre, Olam Group, CEMOI, Ecuakao Group, and United Cocoa Processor. Companies in the Cocoa Bean Derivatives Market are focusing on strategies such as expanding production capacity, investing in advanced processing technologies, and enhancing supply chain efficiency to strengthen their market presence. Firms are prioritizing sustainability and traceability initiatives to meet consumer demand for ethically sourced products. Product portfolio diversification, particularly with organic and specialty cocoa derivatives, helps cater to premium and functional product segments. Strategic partnerships with food, beverage, and personal care manufacturers allow market players to secure long-term contracts and improve market penetration. Companies also emphasize research and development to improve extraction efficiency, flavor consistency, and product quality while maintaining compliance with global food safety standards, creating a competitive advantage in the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Type

- 2.2.3 Category

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.2.6 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer interest in collagen-rich functional nutrition

- 3.2.1.2 Increasing adoption of paleo and keto lifestyles

- 3.2.1.3 Demand for dairy-free protein alternatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and sourcing costs

- 3.2.2.2 Limited appeal among vegetarian and vegan consumers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into ready-to-drink and convenience formats

- 3.2.3.2 Innovation in flavor enhancement and masking technologies

- 3.2.3.3 Growth in emerging health and wellness markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cocoa beans

- 5.3 Cocoa butter

- 5.4 Cocoa powder

- 5.5 Other cocoa derivatives

Chapter 6 Market Estimates and Forecast, By Category, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverages

- 7.3 Personal care

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Distributors / Wholesalers

- 8.3 Retail Channels

- 8.4 Online Channels

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Barry Callebaut

- 10.2 Cargill

- 10.3 CEMOI

- 10.4 Cocoa Touton

- 10.5 ECOM Agroindustrial

- 10.6 Ecuakao Group

- 10.7 Ferrero

- 10.8 Indcre

- 10.9 JB Foods

- 10.10 Mondelez International

- 10.11 Moner Cocoa

- 10.12 Natra

- 10.13 Nestle

- 10.14 Olam Group

- 10.15 United Cocoa Processor