|

시장보고서

상품코드

2019201

육류 및 가금육 가공 장비 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Meat and Poultry Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

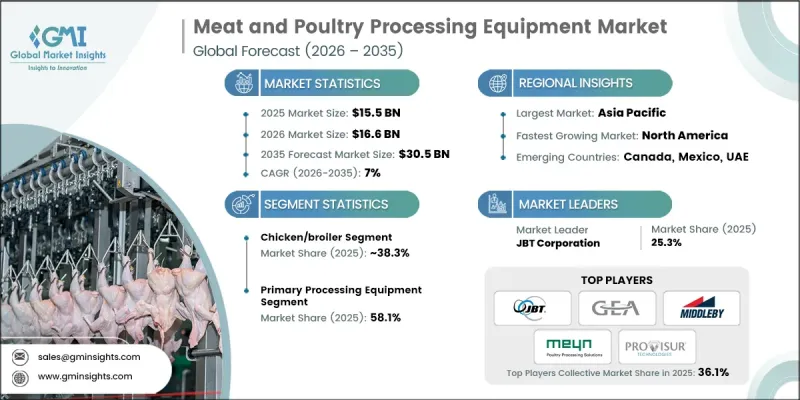

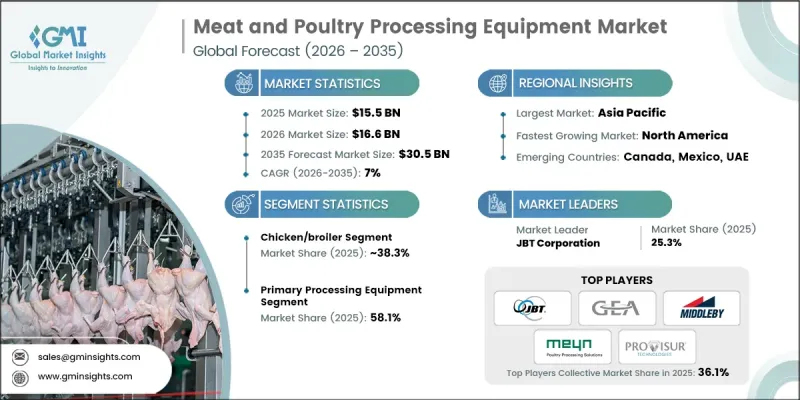

세계의 육류 및 가금육 가공 장비 시장은 2025년에 155억 달러로 평가되었고, CAGR 7%로 성장하여 2035년까지 305억 달러에 이를 것으로 추정되고 있습니다.

이 시장의 성장은 전 세계 육류 소비량 증가와 효율성, 안전성 및 규제 준수를 보장하는 현대화된 첨단 가공 장비에 대한 수요에 의해 주도되고 있습니다. 육류 가공기계는 도축 및 1차 가공부터 포장, 보존에 이르는 전 과정을 아우르며 생산자가 더 높은 생산 수요를 충족시킬 수 있도록 돕고 있습니다. 아시아태평양은 중산층 인구 증가, 가처분 소득 증가, 육류 중심의 식습관 변화로 인해 세계 시장을 주도하고 있습니다. 북미는 자동화와 기술 발전으로 노동력 부족이 해소되고 엄격한 식품 안전 기준을 준수할 수 있는 북미는 가장 빠르게 성장하는 시장입니다. 업무 효율성 향상, 위생 관리 유지 및 대규모 생산 요구 사항에 대응하기 위해 자동화 로봇 및 지능형 가공 시스템에 대한 투자가 필수적입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 155억 달러 |

| 예측액 | 305억 달러 |

| CAGR | 7% |

2025년 기준, 닭고기/육계 부문은 38.3%의 점유율을 차지하고 있으며, 2035년까지 연평균 복합 성장률(CAGR) 7.1%를 나타낼 것으로 예측됩니다. 닭고기의 높은 소비량, 다용도성 및 높은 비용 효율성은 효율성과 안전성을 향상시키는 뼈 제거기, 부분육 가공기, 포장기 등 전문 가공 장비의 주요 촉진요인이 되고 있습니다. 1차 가공 장비는 도축, 내장 제거, 도체 분할과 같은 중요한 공정을 다루기 때문에 2025년 시장의 58.1%를 차지할 것으로 예측됩니다. 이 단계의 자동화는 높은 처리 능력, 위생 관리 및 안전 규정 준수를 위해 필수적입니다.

북미 육류 및 가금류 가공 장비 시장은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.4%를 나타낼 것으로 예측됩니다. 폐수 재활용 및 폐수 관리와 같은 지속 가능한 가공 방식에 대한 관심이 첨단 장비 도입에 힘을 실어주고 있습니다. 환경 영향에 대한 소비자의 인식이 높아지면서 자연 사육 육류 및 가금류에 대한 수요가 증가함에 따라 제조업체는 환경 친화적이고 효율적인 가공 기술에 대한 투자를 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 육류 유형별, 2022-2035

제6장 시장 추산 및 예측 : 가공 단계별, 2022-2035

제7장 시장 추산 및 예측 : 자동화 레벨별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.05.08The Global Meat and Poultry Processing Equipment Market was valued at USD 15.5 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 30.5 billion by 2035.

The market growth is fueled by rising global meat consumption and the demand for modernized advanced processing equipment that ensures efficiency, safety, and regulatory compliance. Meat processing machinery covers all stages, from slaughtering and primary processing to packaging and preservation, allowing producers to meet higher production demands. Asia-Pacific leads the global market due to a growing middle-class population, rising disposable incomes, and shifts toward meat-based diets. North America is the fastest-growing market as automation and technological advancements address labor shortages while ensuring compliance with stringent food safety standards. Investment in automated robots and intelligent processing systems has become essential to improve operational efficiency, maintain hygiene, and meet large-scale production requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.5 Billion |

| Forecast Value | $30.5 Billion |

| CAGR | 7% |

The chicken/broiler segment held a 38.3% share in 2025 and is expected to grow at a CAGR of 7.1% through 2035. The high consumption, versatility, and cost-effectiveness of chicken make it a major driver for specialized processing equipment, including deboning, portioning, and packaging machines that increase efficiency and safety. Primary processing equipment accounted for 58.1% of the market in 2025, as it covers crucial stages like slaughtering, evisceration, and carcass splitting. Automation at this stage is critical for high throughput, hygiene, and compliance with safety regulations.

North America Meat and Poultry Processing Equipment Market is expected to grow at a CAGR of 7.4% between 2026 and 2035. Emphasis on sustainable processing practices, such as wastewater recycling and effluent management, is supporting the adoption of advanced equipment. Consumer awareness of environmental impact, coupled with rising demand for naturally produced meat and poultry, encourages manufacturers to invest in eco-friendly and efficient processing technologies.

Key players in the Global Meat and Poultry Processing Equipment Market include Alberk Poultry Processing Equipment, BAADER, Bayle SA, Cantrell Gainco, Frontmatec, GEA Group, Jarvis Canada, JBT Corporation, Mayekawa, Meyn, Middleby Corporation, Provisur Technologies, and Tomra Food. Companies in the Meat and Poultry Processing Equipment Market strengthen their foothold by investing in R&D to develop automated, high-throughput, and safety-compliant machinery. They expand portfolios to include energy-efficient and sustainable solutions, while forming strategic partnerships with meat producers to enhance market reach. Focused marketing campaigns, after-sales service, and training programs for operators improve product adoption. Regional expansion into high-growth markets, customization to local processing needs, and integration of smart monitoring systems enhance operational efficiency and customer satisfaction, solidifying market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Meat type

- 2.2.3 Processing stage

- 2.2.4 Automation level

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global meat consumption & production expansion

- 3.2.1.2 Labor shortage & automation imperative

- 3.2.1.3 Food safety & quality regulations stringency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment requirements

- 3.2.2.2 Maintenance & service cost concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit & upgrade market

- 3.2.3.2 Emerging species & product categories

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By meat type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Meat Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Beef

- 5.3 Pork

- 5.4 Chicken/broiler

- 5.5 Turkey

- 5.6 Duck

- 5.7 Lamb

- 5.8 Goat

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Processing Stage, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Primary processing equipment

- 6.2.1 Slaughter & evisceration

- 6.2.2 Chilling & carcass handling

- 6.3 Secondary processing equipment

- 6.3.1 Cutting, deboning & trimming

- 6.3.2 Portioning & fabrication

Chapter 7 Market Estimates and Forecast, By Automation Level, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Manual equipment

- 7.3 Semi-automated equipment

- 7.4 Fully automated equipment

- 7.5 Intelligent/AI-enabled systems

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Alberk Poultry Processing Equipment

- 9.2 BAADER

- 9.3 Bayle SA

- 9.4 Cantrell Gainco

- 9.5 Frontmatec

- 9.6 GEA Group

- 9.7 Jarvis Canada

- 9.8 JBT Corporation

- 9.9 Mayekawa

- 9.10 Meyn

- 9.11 Middleby Corporation

- 9.12 Provisur Technologies

- 9.13 Tomra Food