|

시장보고서

상품코드

2019233

의약품 블리스터 포장 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Pharmaceutical Blister Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

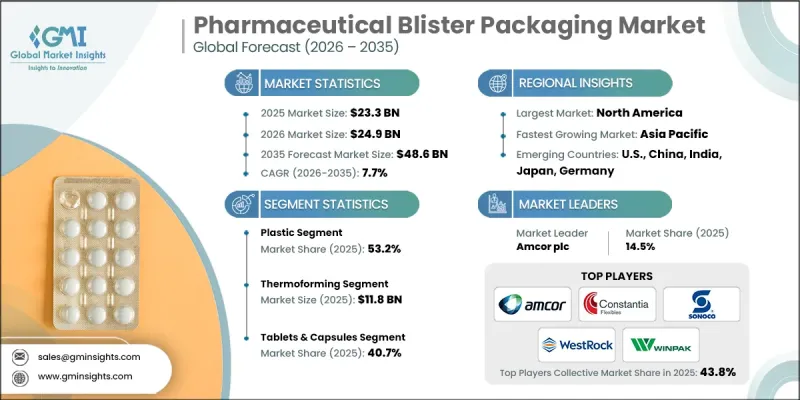

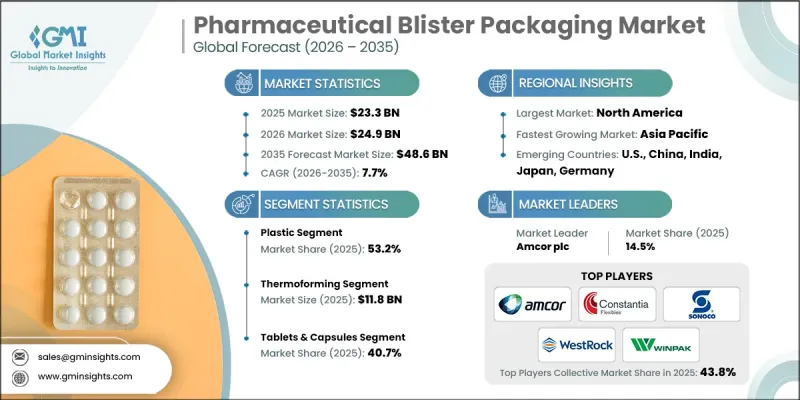

세계의 의약품 블리스터 포장 시장은 2025년에 233억 달러로 평가되었고, CAGR 7.7%로 성장하여 2035년에는 486억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 변조 방지 기능과 추적 가능한 포장을 의무화하는 엄격한 규제 요건과 함께 습기와 산소에 민감한 의약품을 보호하기 위한 고차단성 소재의 채택 확대에 힘입어 성장세를 보이고 있습니다. 만성질환 증가, 고령화, 의료 접근성 향상에 힘입어 선진국 및 신흥 지역의 의약품 생산 확대는 수요를 더욱 증가시키고 있습니다. 제약사들은 추적성 강화 및 확실한 식별 요건을 포함한 위조 방지 규정을 준수하면서 환자의 안전을 강화하기 위해 1회용 포장을 점점 더 많이 활용하고 있습니다. 이러한 추세에 따라 제약 업계 전반에서 제품 보호, 운영 효율성 및 공급망 무결성을 향상시키는 블리스터 포장 솔루션의 채택이 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 233억 달러 |

| 예측액 | 486억 달러 |

| CAGR | 7.7% |

열성형 부문은 정제 및 캡슐에 적합한 투명한 블리스터 캐비티를 효율적으로 생산할 수 있다는 점에서 2025년 118억 달러에 달할 것으로 예측됩니다. 열성형 기술은 가시성, 높은 처리 능력, 자동 포장 시스템과의 원활한 통합을 보장하여 제약 생산 시설 전반에 걸쳐 폭넓게 채택되고 있습니다.

2025년 의약품 블리스터 포장 부문은 시장 점유율의 53.2%를 차지하여 PVC 및 PET와 같은 플라스틱에 대한 높은 의존도를 반영합니다. 이 소재는 성형성이 우수하여 정제나 캡슐을 담을 수 있는 정밀한 캐비티 성형이 가능하여 매우 선호되고 있습니다. 투명성이 뛰어나 내용물을 명확하게 확인할 수 있어 품질 검사와 환자들에게 안심감을 주는데 중요한 역할을 합니다. 또한, PVC와 PET는 대규모 생산에서 비용 효율적인 솔루션을 제공하여 제조업체가 재료비를 최소화하면서 높은 처리 능력을 유지할 수 있게 해줍니다.

2025년 북미 의약품 블리스터 포장 시장은 34.7%의 점유율을 차지했습니다. 이 지역의 성장은 대규모 의약품 제조 기지, 엄격한 규제 기준, 병원 및 소매 약국에서의 1회용 포장에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다. 제약회사와 포장 공급업체들은 업무 효율성 향상, 규제 준수, 환경 문제 대응을 위해 고도의 자동화 및 지속 가능한 블리스터 포장 솔루션에 투자하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 재료별, 2022-2035

제6장 시장 추산 및 예측 : 기술별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.05.08The Global Pharmaceutical Blister Packaging Market was valued at USD 23.3 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 48.6 billion in 2035.

Market growth is fueled by stringent regulatory mandates requiring tamper-evident and traceable packaging, coupled with heightened adoption of high-barrier materials to protect moisture- and oxygen-sensitive drugs. Expanding pharmaceutical production in developed and emerging regions, driven by the rising incidence of chronic diseases, aging populations, and enhanced healthcare access, is further boosting demand. Pharmaceutical manufacturers are increasingly leveraging unit-dose packaging to enhance patient safety while complying with anti-counterfeiting regulations, including enhanced traceability and secure identification requirements. These trends are accelerating the adoption of blister packaging solutions that improve product protection, operational efficiency, and supply chain integrity across the pharmaceutical sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.3 Billion |

| Forecast Value | $48.6 Billion |

| CAGR | 7.7% |

The thermoforming segment reached USD 11.8 billion in 2025, due to its efficiency in producing transparent blister cavities suitable for tablets and capsules. Thermoforming technology ensures visibility, high throughput, and seamless integration with automated packaging systems, supporting widespread adoption across pharmaceutical production facilities.

The pharmaceutical blister packaging segment accounted for 53.2% share in 2025, reflecting the widespread reliance on plastics such as PVC and PET. These materials are highly favored due to their excellent formability, allowing precise cavity shaping to hold tablets and capsules. Their superior clarity ensures that the contents are clearly visible, which is important for both quality inspection and patient assurance. PVC and PET also offer cost-effective solutions for large-scale production, enabling manufacturers to maintain high throughput while minimizing material expenses.

North America Pharmaceutical Blister Packaging Market accounted for 34.7% share in 2025. The region's growth is supported by its large pharmaceutical manufacturing base, strict regulatory standards, and increasing demand for unit-dose packaging in hospitals and retail pharmacies. Pharmaceutical companies and packaging suppliers are investing in advanced automation and sustainable blister packaging solutions to enhance operational efficiency, maintain regulatory compliance, and address environmental concerns.

Key players operating in the Global Pharmaceutical Blister Packaging Market include ACG, Amcor plc, AptarGroup, Inc., Borealis AG, Carcano Antonio S.p.A., Caprihans India Limited, Constantia Flexibles, Dow, Honeywell International Inc., Huhtamaki, RENOLIT SE, Rohrer Corporation, Romaco Group, Sonoco Products Company, SUDPACK, Syensqo, Tekni-Plex, Inc., Tjoapack LLC, VinylPlus, WestRock Company, and Winpak Control Group. Companies in the Global Pharmaceutical Blister Packaging Market are strengthening their presence through strategic innovation and operational enhancements. They are investing in R&D to develop high-barrier, eco-friendly, and sustainable materials that meet evolving regulatory requirements and consumer expectations. Collaborations with pharmaceutical manufacturers and technology providers enable tailored packaging solutions and seamless integration into automated production lines. Expansion into emerging markets and regional manufacturing facilities ensures improved supply chain access and cost efficiency. Additionally, players focus on process automation, digital tracking, and serialization technologies to enhance product security, optimize operational throughput, and maintain competitive advantage in the global pharmaceutical packaging landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Technology trends

- 2.2.3 End-use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global pharmaceutical consumption rates

- 3.2.1.2 Increasing demand for unit-dose patient safety packaging

- 3.2.1.3 Regulatory mandates for tamper-evidence and traceability

- 3.2.1.4 Adoption of high-speed automated packaging lines

- 3.2.1.5 Need for moisture/oxygen barrier protection for drugs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rigid regulatory compliance burden

- 3.2.2.2 Difficult recyclability of multilayer packs

- 3.2.3 Market opportunities

- 3.2.3.1 Shift to recyclable mono-material blisters

- 3.2.3.2 Smart/serialized packaging innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Aluminum Foil

- 5.4 Paper

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Cold Forming

- 6.3 Thermoforming

- 6.4 Heat Seal

Chapter 7 Market Estimates and Forecast, By End-Use, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Tablets & Capsules

- 7.3 Medical Devices

- 7.4 Injectables

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Amcor plc

- 9.1.2 Constantia Flexibles

- 9.1.3 Sonoco Products Company

- 9.1.4 WestRock Company

- 9.1.5 Winpak Control Group

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 AptarGroup, Inc.

- 9.2.1.2 Rohrer Corporation

- 9.2.1.3 Tekni-Plex, Inc.

- 9.2.1.4 Dow

- 9.2.2 Asia Pacific

- 9.2.2.1 ACG

- 9.2.2.2 Caprihans India Limited

- 9.2.2.3 Huhtamaki

- 9.2.3 Europe

- 9.2.3.1 Borealis AG

- 9.2.3.2 Carcano Antonio S.p.A.

- 9.2.3.3 RENOLIT SE

- 9.2.3.4 SUDPACK

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Honeywell International Inc.

- 9.3.2 Romaco Group

- 9.3.3 Syensqo

- 9.3.4 Tjoapack LLC

- 9.3.5 VinylPlus