|

시장보고서

상품코드

2027497

내약품성 코팅 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Chemical Resistant Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

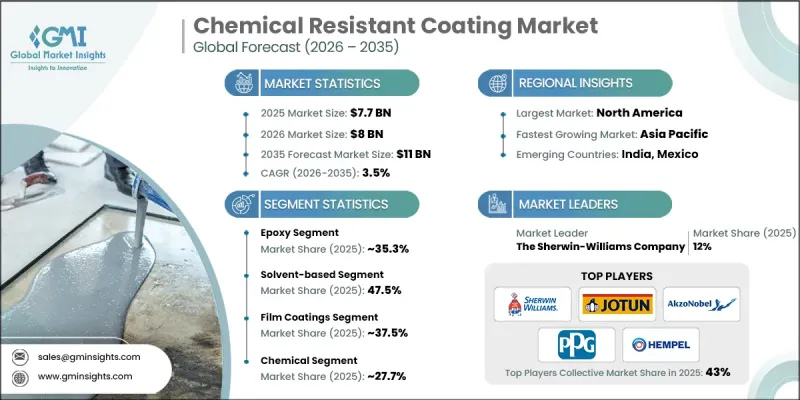

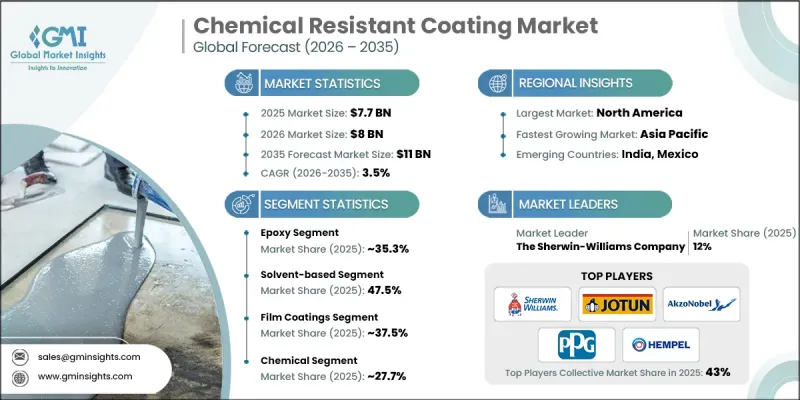

세계의 내약품성 코팅 시장은 2025년에 77억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.5%를 나타내 110억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 가혹한 화학 물질에 대한 노출을 견디고 중요한 자산의 수명을 연장할 수 있는 내구성 있는 보호 솔루션에 대한 산업 전반 수요 증가에 힘입어 성장세를 보이고 있습니다. 이러한 코팅은 단순한 보호의 범위를 넘어 제조, 에너지, 중공업 등의 분야에서 업무 효율성 유지, 유지보수로 인한 가동 중단 최소화 및 설비 수명 연장에 필수적인 역할을 하고 있습니다. 시장 역학은 지속가능성과 책임감 있는 산업 관행에 대한 관심이 높아짐에 따라 큰 영향을 받고 있습니다. 기업들은 높은 성능 기준을 유지하면서 배출량을 줄이고, 환경 규제를 준수하는 코팅 솔루션을 우선시하고 있습니다. 제조업체들은 내구성과 비용 효율성을 모두 갖춘 친환경적인 배합에 초점을 맞춘 혁신적인 제품 개발 전략으로 전환하고 있습니다. 또한, 북미에서는 고도의 연구 역량과 산업 현대화를 통해 혁신을 지속적으로 추진하고 있으며, 복잡한 운영 조건에 맞는 특수 코팅 기술을 개발할 수 있도록 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 77억 달러 |

| 예측액 | 110억 달러 |

| CAGR | 3.5% |

에폭시 코팅은 2025년 35.3%의 점유율을 차지했으며, 2035년까지 연평균 3.4%의 성장률을 나타낼 것으로 예측됩니다. 이 코팅은 우수한 접착력, 강력한 장벽 보호 및 화학적, 기계적, 열적 스트레스에 대한 내성으로 널리 인정받고 있습니다. 구조적 강도로 인해 일관되고 장기적인 보호가 필요한 중요한 산업 장비를 보호할 수 있는 신뢰할 수 있는 선택입니다. 에폭시와 폴리우레탄 기술을 결합한 코팅 시스템은 유연성, 내충격성, 내마모성이 향상되어 역동적인 구조물이나 복잡한 표면을 수반하는 용도에 적합합니다. 또한, 실리콘계 배합은 극한의 온도에서도 안정성을 유지하기 때문에 장시간 열, 산화, 가혹한 대기 조건에 노출되는 환경에서 중요한 역할을 계속하고 있습니다.

솔벤트 기반 페인트 부문은 2025년 47.5%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 3.3%의 성장률을 나타낼 것으로 전망됩니다. 우수한 필름 형성 능력, 뛰어난 접착력, 화학적으로 가혹한 환경에서의 내구성은 이 부문에서 지속적인 우위를 점하는 데 기여하고 있습니다. 이 시스템은 특히 부식성 물질이나 변동하는 온도 조건에 대한 확실한 보호가 필요한 응용 분야에 적합합니다. 한편, 조직이 지속가능성과 규제 준수에 점점 더 집중함에 따라 수성 페인트에 대한 수요가 증가하고 있습니다. 이러한 대체품은 효과적인 성능을 유지하면서 배출량을 줄이고, 작업장 안전을 개선하며, 환경 목표를 달성할 수 있도록 도와줍니다. 분체 도료 또한 재료의 낭비를 최소화하고 장기적인 운영상의 이점이 있는 효율적이고 환경 친화적인 도장 솔루션을 제공함으로써 시장 상황을 강화하고 있습니다.

북미의 내약품성 코팅 시장은 2025년 35% 점유율을 차지하며 강력한 성장 잠재력을 계속 보여주었습니다. 이 지역은 잘 정비된 산업 기반, 현대적 제조 인프라, 엄격한 환경 규제에 힘입어 첨단 코팅 기술의 주요 거점으로 자리매김하고 있습니다. 이러한 요인들은 고성능 및 친환경 코팅 시스템의 채택을 촉진하고, 기업이 안전 표준을 준수하면서 업무 효율성을 향상시킬 수 있도록 돕습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 수지 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 기술별(2022-2035년)

제7장 시장 추산 및 예측 : 필름 두께별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.05.20The Global Chemical Resistant Coating Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 11 billion by 2035.

Market growth is driven by the increasing need across industries for durable protective solutions that can withstand aggressive chemical exposure and extend the service life of critical assets. These coatings have evolved beyond basic protection and are now essential in maintaining operational efficiency, minimizing maintenance interruptions, and improving equipment longevity across sectors such as manufacturing, energy, and heavy engineering. Market dynamics are strongly influenced by the growing emphasis on sustainability and responsible industrial practices. Companies are prioritizing environmentally compliant coating solutions that reduce emissions while maintaining high performance standards. Manufacturers are shifting toward innovative product development strategies that focus on eco-friendly formulations capable of delivering durability and cost efficiency. In addition, North America continues to foster innovation through advanced research capabilities and industrial modernization, enabling the development of specialized coating technologies tailored for complex operating conditions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $11 Billion |

| CAGR | 3.5% |

The epoxy-based coatings accounted for 35.3% share in 2025 and is expected to grow at a CAGR of 3.4% through 2035. These coatings are widely recognized for their superior adhesion, strong barrier protection, and resistance to chemical, mechanical, and thermal stress. Their structural strength makes them a reliable choice for safeguarding essential industrial equipment that requires consistent and long-term protection. Coating systems that combine epoxy and polyurethane technologies offer enhanced flexibility, impact resistance, and abrasion protection, making them suitable for applications involving dynamic structures and complex surfaces. In addition, silicone-based formulations continue to play an important role in environments exposed to prolonged heat, oxidation, and demanding atmospheric conditions due to their stability under extreme temperatures.

The solvent-based coatings segment held 47.5% share in 2025 and is anticipated to grow at a CAGR of 3.3% from 2026 to 2035. Their strong film-forming capabilities, excellent adhesion, and durability in chemically aggressive environments contribute to their continued dominance. These systems are particularly suited for operations that require reliable protection against corrosive substances and fluctuating temperature conditions. At the same time, water-based coatings are gaining traction as organizations increasingly focus on sustainability and regulatory compliance. These alternatives offer reduced emissions while maintaining effective performance, improving workplace safety, and supporting environmental goals. Powder coatings are also strengthening the market landscape by minimizing material waste and delivering efficient, environmentally responsible coating solutions with long-term operational benefits.

North America Chemical Resistant Coating Market accounted for 35% share in 2025 and continues to demonstrate strong growth potential. The region has established itself as a key hub for advanced coating technologies, supported by a well-developed industrial base, modern manufacturing infrastructure, and stringent environmental regulations. These factors encourage the adoption of high-performance and eco-friendly coating systems, enabling companies to align with safety standards while improving operational efficiency.

Leading companies operating in the Global Chemical Resistant Coating Market include PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Hempel A/S, Jotun A/S, Axalta Coating Systems, RPM International Inc., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Asian Paints Limited, Carboline Company, and Tnemec Company, Inc. Companies in the chemical resistant coating market are adopting strategies such as expanding production capacity and strengthening global distribution networks to meet increasing demand across industries. Significant investments in research and development are enabling the creation of advanced formulations that offer enhanced durability, improved chemical resistance, and reduced environmental impact. Strategic collaborations and partnerships are helping firms access new markets and broaden their customer base. Many companies are also focusing on sustainable innovation by developing low-emission and eco-friendly coating solutions to comply with evolving regulatory standards. In addition, mergers and acquisitions are being utilized to consolidate market position, enhance technological capabilities, and diversify product portfolios, while branding and marketing efforts emphasize performance reliability and long-term cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Resin Type

- 2.2.3 Technology

- 2.2.4 Film Thickness

- 2.2.5 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in industrial applications

- 3.2.1.2 Stringent environmental regulations

- 3.2.1.3 Growing infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Transition to powder coating technologies in heavy industry

- 3.2.3.2 Sustainable & bio-based resin development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By resin type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Resin Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Epoxy

- 5.3 Polyester

- 5.4 Fluoropolymers

- 5.5 Polyurethane

- 5.6 Other resins

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-based

- 6.3 Water-based

- 6.4 Powder Coating

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Film Thickness, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Thin Film Coatings

- 7.3 Medium Build Coatings

- 7.4 Heavy Duty Coatings

- 7.5 Ultra-Heavy Duty Systems

Chapter 8 Market Estimates and Forecast, By End-User, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical

- 8.2.1 Chemical Processing Plants

- 8.2.2 Petrochemical Facilities

- 8.2.3 Fertilizer Manufacturing

- 8.2.4 Others

- 8.3 Oil & gas

- 8.4 Marine

- 8.5 Construction & infrastructural

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 The Sherwin-Williams Company

- 10.2 Jotun A/S

- 10.3 AkzoNobel N.V.

- 10.4 PPG Industries, Inc.

- 10.5 Hempel A/S

- 10.6 Axalta Coating Systems

- 10.7 RPM International Inc.

- 10.8 Kansai Paint Co., Ltd.

- 10.9 Nippon Paint Holdings Co., Ltd.

- 10.10 Asian Paints Limited

- 10.11 Carboline Company

- 10.12 Tnemec Company, Inc.