|

시장보고서

상품코드

2027504

우주 경제 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Space Economy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

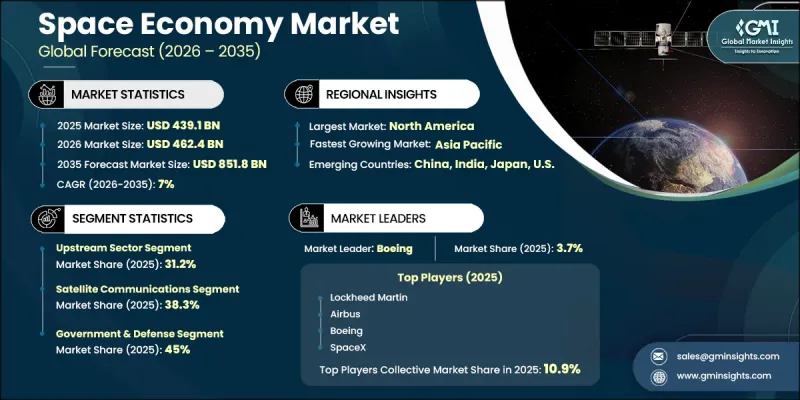

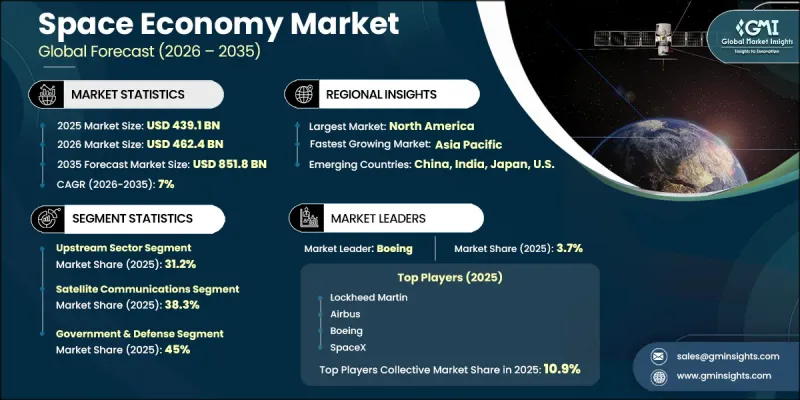

세계의 우주 경제 시장은 2025년에 4,391억 달러로 평가되었고 CAGR 7%를 나타내 2035년까지 8,518억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 위성 기반 서비스의 급속한 성장, 우주 프로그램에 대한 공공 부문의 자금 지원 증가, 우주 기술에 대한 민간 자본의 유입 증가에 의해 주도되고 있습니다. 위성 시스템 및 발사 능력의 지속적인 혁신은 운영 효율성을 크게 향상시키고 비용을 절감하여 업계 전반의 채택을 더욱 가속화하고 있습니다. 통신, 내비게이션, 데이터 서비스에서 우주 기술을 활용한 용도에 대한 의존도가 높아지면서 전 세계 수요를 지속적으로 견인하고 있습니다. 우주 활동의 상업화가 진행됨에 따라 신규 진출기업 및 기존 기업들이 첨단 인프라에 투자하고 있으며, 경쟁 구도도 재편되고 있습니다. 산업 전반의 응용 분야 확대와 기술 발전이 시장의 상승세를 견인하고 있습니다. 또한, 안정적인 연결성과 데이터 기반 서비스에 대한 수요가 증가함에 따라 현대 경제에서 우주 기술의 역할이 점점 더 중요해지고 있으며, 이는 장기적인 시장 성장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 4,391억 달러 |

| 예측액 | 8,518억 달러 |

| CAGR | 7% |

위성 네트워크의 확장 및 우주 기반 연결 솔루션의 중요성이 증가함에 따라 우주 경제 시장은 점점 더 큰 추진력을 얻고 있습니다. 첨단 통신, 항법, 관측 기능에 대한 수요는 지속적으로 확대되고 있으며, 이는 업계의 지속적인 성장을 뒷받침하고 있습니다. 각국이 독자적인 우주 능력과 첨단 기술 개발에 우선순위를 두고 있는 상황에서 정부 자금과 국방 관련 투자는 여전히 중요한 원동력이 되고 있습니다. 민간 부문의 참여도 활발해지면서 차세대 우주 인프라를 위한 자금 투입이 증가하고 있습니다. 대규모 위성 네트워크의 급속한 확장은 제조, 발사 서비스, 궤도 운영의 혁신을 가져왔고, 궁극적으로 전체 시장의 용량과 효율성을 향상시켰습니다.

2025년에는 위성 제조, 발사 운영, 우주선 부품 제조와 같은 고부가가치 활동에 힘입어 업스트림 부문이 31.2%의 점유율을 차지했습니다. 우주 인프라에 대한 강력한 투자 흐름과 민관 협력 이니셔티브가 결합되어 이 부문의 성장을 계속 지원하고 있습니다. 발사 기술 및 위성 설계의 발전은 상업용 및 정부용 모두에서 수요를 더욱 강화하고 있습니다.

위성 통신 부문은 고속 연결 및 첨단 통신 네트워크에 대한 수요 증가에 힘입어 2025년 38.3%의 점유율을 차지했습니다. 위성 별자리 확대와 신뢰할 수 있는 연결 솔루션에 대한 수요 증가가 이 부문의 성장을 주도하고 있습니다. 다양한 응용 분야에서 위성 활용 기술의 채택이 확대됨에 따라 전체 우주 경제 시장에서 이 부문의 중요성이 점점 더 커지고 있습니다.

2025년 북미의 우주 경제 시장은 43.8%의 점유율을 차지했습니다. 이 지역은 우주 관련 이니셔티브에 대한 정부의 강력한 투자와 기술 발전에 대한 지속적인 노력으로 선도적 지위를 유지하고 있습니다. 공공기관과 민간기업의 협력으로 차세대 우주 시스템 개발 및 보급이 가속화되고 있습니다. 우주 역량을 강화하기 위한 자금 증가와 전략적 이니셔티브는 이미 구축된 혁신 및 상업화 생태계와 함께 이 지역의 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 밸류체인 부문별(2022-2035년)

제6장 시장 추산 및 예측 : 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTH 26.05.20The Global Space Economy Market was valued at USD 439.1 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 851.8 billion by 2035.

Market expansion is driven by the rapid growth of satellite-based services, increasing public sector funding for space programs, and rising private capital flowing into space technologies. Continuous innovation in satellite systems and launch capabilities is significantly improving operational efficiency and reducing costs, which further accelerates adoption across industries. The growing reliance on space-enabled applications for communication, navigation, and data services continues to drive global demand. Increased commercialization of space activities is also reshaping the competitive landscape, with new entrants and established players investing in advanced infrastructure. Expanding applications across industries and rising technological advancements are reinforcing the market's upward trajectory. Additionally, growing demand for reliable connectivity and data-driven services continues to enhance the role of space technologies in modern economies, supporting long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $439.1 Billion |

| Forecast Value | $851.8 Billion |

| CAGR | 7% |

The space economy market is gaining momentum due to the increasing deployment of satellite networks and the rising importance of space-based connectivity solutions. Demand for advanced communication, navigation, and observation capabilities continues to expand, supporting sustained industry growth. Government funding and defense-related investments remain critical drivers, with nations prioritizing the development of independent space capabilities and advanced technologies. Private sector involvement is also intensifying, with increased funding directed toward next-generation space infrastructure. The rapid expansion of large-scale satellite networks is transforming manufacturing, launch services, and orbital operations, ultimately increasing overall market capacity and efficiency.

The upstream segment captured 31.2% share in 2025, driven by high-value activities such as satellite production, launch operations, and spacecraft component manufacturing. Strong investment flows into space infrastructure, combined with collaborative initiatives between public and private sectors, continue to support growth in this segment. Advancements in launch technologies and satellite design are further strengthening demand across both commercial and government applications.

The satellite communications segment held a 38.3% share in 2025, supported by increasing demand for high-speed connectivity and advanced communication networks. Expansion of satellite constellations and the growing need for reliable connectivity solutions are driving segment growth. Rising adoption of satellite-enabled technologies across various applications continues to enhance the importance of this segment within the overall space economy market.

North America Space Economy Market held a 43.8% share in 2025. The region maintains its leadership position due to strong government investment in space-related initiatives and continued focus on technological advancement. Collaboration between public institutions and private companies is accelerating the development and deployment of next-generation space systems. Increased funding and strategic initiatives aimed at strengthening space capabilities are further supporting regional growth, along with a well-established ecosystem for innovation and commercialization.

Key companies operating in the Global Space Economy Market include Airbus, Arianespace, Astra Space, Axiom Space, Blue Origin, Boeing, China Aerospace Science and Technology Corporation, Firefly Aerospace, Iridium Communications, ispace, Lockheed Martin, Maxar Technologies, Mitsubishi Heavy Industries, Northrop Grumman, OneWeb, Raytheon Technologies, Relativity Space, Rocket Lab, Sierra Space, SpaceX, Thales Alenia Space, United Launch Alliance, and Virgin Galactic. Companies in the Space Economy Market are strengthening their market position through continuous innovation and strategic investments. They focus on developing advanced satellite technologies, efficient launch systems, and scalable space infrastructure to enhance performance and reduce operational costs. Partnerships and collaborations across public and private sectors are enabling companies to expand capabilities and access new markets. Investment in research and development supports the introduction of next-generation solutions and improves service reliability. Organizations are also increasing production capacity and optimizing supply chains to meet rising demand. Additionally, companies are prioritizing commercialization strategies, expanding service portfolios, and leveraging data-driven solutions to enhance competitiveness and secure long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Value chain sector trends

- 2.2.2 Application trends

- 2.2.3 End user trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Satellite Broadband Mega-Constellations and Space-Enabled Connectivity Services

- 3.2.1.2 Rising government and defense expenditures

- 3.2.1.3 Surging private investment in space technology

- 3.2.1.4 Rapid technological innovation in satellite and launch systems

- 3.2.1.5 Increasing utilization of space-enabled services across industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital expenditure for satellite development and launch

- 3.2.2.2 Regulatory complexities and international coordination

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of small satellite constellations for Earth observation and communication

- 3.2.3.2 Growth in reusable launch vehicle technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Value Chain Sector, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Upstream sector

- 5.2.1 Satellite manufacturing

- 5.2.2 Launch vehicle manufacturing

- 5.2.3 Ground equipment manufacturing

- 5.2.4 Others

- 5.3 Midstream sector

- 5.3.1 Launch services

- 5.3.2 Satellite operations & control

- 5.3.3 In-orbit servicing & debris removal

- 5.3.4 Others

- 5.4 Downstream sector

- 5.4.1 Satellite communications services

- 5.4.2 Earth observation & data services

- 5.4.3 Navigation & positioning services

- 5.4.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Satellite Communications

- 6.2.1 Broadband & Fixed Connectivity

- 6.2.2 Broadcasting & Media Distribution

- 6.2.3 Mobile & IoT connectivity

- 6.2.4 Government & military communications

- 6.2.5 Others

- 6.3 Earth observation & remote sensing

- 6.3.1 Imaging & monitoring services

- 6.3.2 Geospatial analytics & intelligence

- 6.3.3 Environmental & climate monitoring

- 6.3.4 Agriculture & natural resource management

- 6.3.5 Others

- 6.4 Navigation & positioning (GNSS)

- 6.4.1 Consumer location-based services

- 6.4.2 Precision agriculture & fleet management

- 6.4.3 Timing & synchronization services

- 6.4.4 Aviation & maritime navigation

- 6.4.5 Others

- 6.5 Space exploration & science

- 6.5.1 Planetary exploration missions

- 6.5.2 Space telescopes & observatories

- 6.5.3 Human spaceflight programs

- 6.5.4 Scientific research & experimentation

- 6.5.5 Others

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Government & defense

- 7.2.1 Military & intelligence applications

- 7.2.2 Civil government programs

- 7.2.3 National security & surveillance

- 7.2.4 Institutional space exploration

- 7.2.5 Others

- 7.3 Commercial enterprises

- 7.3.1 Telecommunications operators

- 7.3.2 Media & broadcasting companies

- 7.3.3 Agriculture & forestry

- 7.3.4 Maritime & aviation industries

- 7.3.5 Energy & utilities sector

- 7.3.6 Others

- 7.4 Scientific & academic

- 7.4.1 Research institutions

- 7.4.2 University space programs

- 7.4.3 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Airbus

- 9.1.2 Boeing

- 9.1.3 Lockheed Martin

- 9.1.4 Northrop Grumman

- 9.1.5 Raytheon Technologies

- 9.1.6 SpaceX

- 9.1.7 Thales Alenia Space

- 9.1.8 Iridium Communications

- 9.2 Regional key players

- 9.2.1 Arianespace

- 9.2.2 China Aerospace Science

- 9.2.3 Maxar Technologies

- 9.2.4 Mitsubishi Heavy Industries

- 9.2.5 OneWeb

- 9.2.6 Sierra Space

- 9.2.7 United Launch Alliance

- 9.3 Niche Players/Disruptors

- 9.3.1 Astra Space

- 9.3.2 Axiom Space

- 9.3.3 Blue Origin

- 9.3.4 Firefly Aerospace

- 9.3.5 ispace

- 9.3.6 Relativity Space

- 9.3.7 Rocket Lab

- 9.3.8 Virgin Galactic