|

시장보고서

상품코드

2027509

폼 테이프 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Foam Tape Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

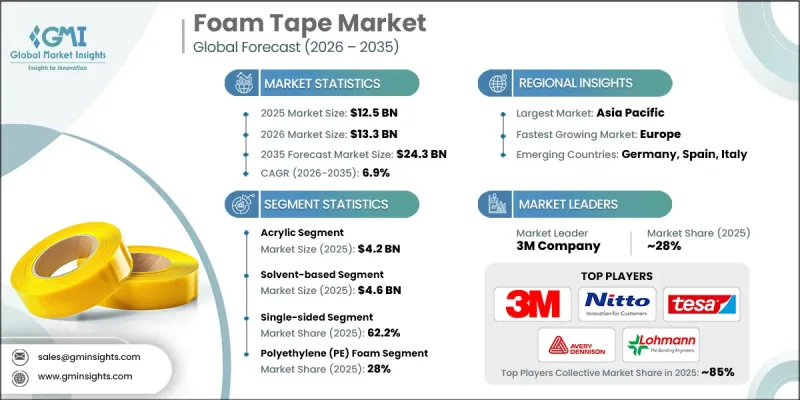

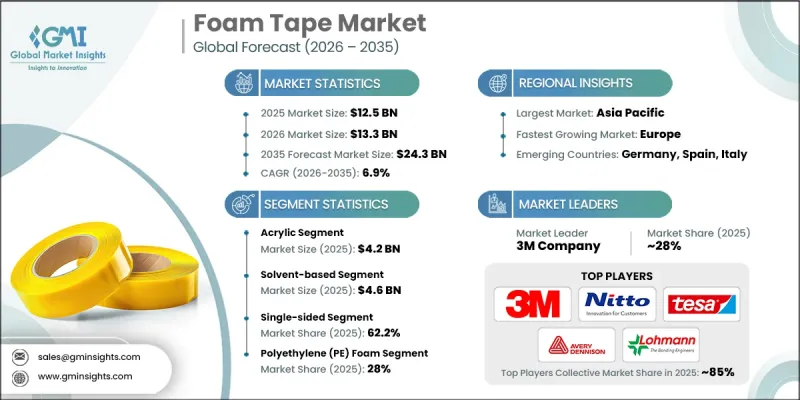

세계의 폼 테이프 시장은 2025년에 125억 달러로 평가되었고 CAGR 6.9%를 나타내 2035년까지 243억 달러에 이를 것으로 추정되고 있습니다.

세계의 폼 테이프 산업은 산업, 상업, 소비자 등 다양한 이용 사례에 힘입어 꾸준히 성장하고 있습니다. 폼 테이프 솔루션은 완충, 밀봉, 진동 제어, 단열, 접착 기능을 위해 널리 사용되고 있으며, 운송, 건설, 전자, 의료, 제조 등의 분야에서 필수 불가결한 요소로 자리 잡고 있습니다. 가볍고 효율적이며 깨끗한 조립 솔루션에 대한 수요가 증가함에 따라 각 산업계가 전통적인 기계식 체결 시스템에서 벗어나면서 폼 테이프의 채택이 가속화되고 있습니다. 자동차 및 운송 부문에서는 폼 테이프가 개스킷 형성, 트림 장착, 소음 감소, 단열에 널리 사용되고 있으며, 전기자동차의 보급이 증가함에 따라 고급 접착 솔루션에 대한 수요가 더욱 증가하고 있습니다. 건설 산업도 도시 개발 및 개보수 활동을 배경으로 밀봉, 유리 설치, 단열 등의 용도를 통해 시장 성장에 크게 기여하고 있습니다. 접착제 화학 및 발포 재료 공학의 지속적인 발전으로 제품 성능이 향상되어 습기, 온도 변화 및 환경적 스트레스에 대한 내성을 유지하면서 다양한 기판 간 보다 견고한 접착이 가능해졌습니다. 두께, 밀도, 접착제 조성물 제어를 포함한 커스터마이징 능력의 향상으로 특수 용도에 대한 제품 적합성이 더욱 향상되었습니다. 지속가능성에 대한 관심도 제품 개발에 영향을 미치고 있으며, 저 VOC 배합 및 재활용 가능한 부품에 대한 수요 증가는 친환경 제조 관행을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 125억 달러 |

| 예측액 | 243억 달러 |

| CAGR | 6.9% |

아크릴 폼 테이프 시장은 2025년 42억 달러 규모로 평가되었고 2035년까지 연평균 복합 성장률(CAGR) 7.1%를 나타낼 것으로 예측됩니다. 이 부문은 강력한 접착력, 장기적인 내구성, 열, 자외선, 노화에 대한 우수한 내성으로 인해 지속적으로 성장하고 있습니다. 이러한 성능 특성으로 인해 아크릴 폼 테이프는 자동차 조립, 건축 시스템, 전자 제품 및 산업 제조 공정의 까다로운 응용 분야에 매우 적합합니다. 금속, 플라스틱, 유리를 포함한 다양한 표면 유형에 대한 접착력을 유지할 수 있는 능력은 그 채택을 더욱 촉진하고 있습니다. 구조용 접착, 외장재 및 영구 밀봉 솔루션에 대한 사용이 증가함에 따라 아크릴 폼 테이프 시장 지배력이 강화되고 있습니다.

단면 폼 테이프 부문은 2025년 78억 달러로 62.2%의 점유율을 차지했으며 2035년까지 연평균 복합 성장률(CAGR) 6.7%를 나타낼 것으로 예측됩니다. 이 부문은 시공의 용이성, 비용 효율성, 광범위한 산업 및 상업용 응용 분야에 대한 적응성 때문에 선도적인 위치를 차지하고 있습니다. 단면 폼 테이프는 건설, 자동차, 전자 등 다양한 분야에서 단열, 완충, 밀봉, 표면 보호를 위해 널리 사용되고 있습니다. 다양한 기판과의 호환성, 일시적 및 반영구적 접착 응용에 대한 적합성이 시장 침투를 더욱 촉진하고 있습니다. 대규모 제조 및 조립 작업의 강력한 수요가 이 부문의 지속적인 성장을 뒷받침하고 있습니다.

북미의 폼 테이프 시장은 자동차, 건설 및 전기 장비 제조 산업의 존재로 인해 2025년 41억 달러로 평가되었습니다. 미국은 자동차 생산, 인프라 유지보수 활동 및 진행 중인 주택 개조 프로젝트에 힘입어 소비에서 중심적인 역할을 하고 있습니다. 폼 테이프는 밀봉, 진동 감쇠, 단열 및 부품 고정 용도로 널리 사용됩니다. 이 지역의 고성능 소재에 대한 집중, 엄격한 안전 기준 및 일관된 제품 품질 요구사항은 산업 및 상업 분야에서 지속적인 채택을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 수지별(2022-2035년)

제6장 시장 추산 및 예측 : 기술별(2022-2035년)

제7장 시장 추산 및 예측 : 테이프 유형별(2022-2035년)

제8장 시장 추산 및 예측 : 발포재 유형별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 이용 산업별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

KTH 26.05.20The Global Foam Tape Market was valued at USD 12.5 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 24.3 billion by 2035.

The global foam tape industry is witnessing steady expansion driven by its broad applicability across industrial, commercial, and consumer use cases. Foam tape solutions are widely utilized for cushioning, sealing, vibration control, thermal insulation, and bonding functions, making them essential across sectors such as transportation, construction, electronics, healthcare, and manufacturing. The increasing preference for lightweight, efficient, and clean assembly solutions is accelerating adoption as industries move away from traditional mechanical fastening systems. In the automotive and transportation sector, foam tapes are extensively used for gasket formation, trim attachment, noise reduction, and thermal insulation, with rising electric vehicle adoption further strengthening demand for advanced adhesive solutions. The construction industry is also contributing significantly to market growth through applications in sealing, glazing, and insulation, supported by urban development and renovation activities. Continuous advancements in adhesive chemistry and foam material engineering are enhancing product performance, enabling stronger bonding across diverse substrates while maintaining resistance to moisture, temperature variations, and environmental stress. Growing customization capabilities, including control over thickness, density, and adhesive composition, are further improving product suitability across specialized applications. Sustainability considerations are also influencing product development, with increasing demand for low-VOC formulations and recyclable components supporting environmentally responsible manufacturing practices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.5 Billion |

| Forecast Value | $24.3 Billion |

| CAGR | 6.9% |

The acrylic foam tape segment was valued at USD 4.2 billion in 2025 and is projected to grow at a CAGR of 7.1% through 2035. This segment continues to expand due to its strong bonding strength, long-term durability, and excellent resistance to heat, ultraviolet exposure, and aging effects. These performance characteristics make acrylic-based foam tapes highly suitable for demanding applications across automotive assembly, construction systems, electronics, and industrial manufacturing processes. Their ability to maintain adhesion across different surface types, including metals, plastics, and glass, further strengthens their adoption. Increasing use in structural bonding, exterior applications, and permanent sealing solutions is reinforcing the dominance of acrylic foam tapes in the market.

The single-sided foam tape segment accounted for USD 7.8 billion in 2025, holding a 62.2% share, and is expected to grow at a CAGR of 6.7% through 2035. This segment leads due to its ease of application, cost efficiency, and adaptability across a wide range of industrial and commercial uses. Single-sided foam tapes are widely employed for insulation, cushioning, sealing, and surface protection across multiple sectors, including construction, automotive, and electronics. Their compatibility with different substrates and suitability for both temporary and semi-permanent bonding applications further enhance their market penetration. Strong demand from large-scale manufacturing and assembly operations continues to support sustained growth in this segment.

North America Foam Tape Market was valued at USD 4.1 billion in 2025 owing to the presence of well-established automotive, construction, and electrical manufacturing industries. The United States plays a central role in consumption, driven by vehicle production, infrastructure maintenance activities, and ongoing residential renovation projects. Foam tapes are widely used across sealing, vibration dampening, insulation, and component mounting applications. The region's focus on high-performance materials, strict safety standards, and consistent product quality requirements continues to support sustained adoption across industrial and commercial sectors.

Key companies operating in the Global Foam Tape Market include 3M Company, Nitto Denko Corporation, Avery Dennison Corporation, Tesa SE (Tesa Tapes India), Lohmann GmbH & Co. KG, LINTEC Corporation, Intertape Polymer Group, Scapa Group, LAMATEK, Inc., 3F GmbH Klebe- & Kaschiertechnik, and Wuxi Canaan Adhesive Technology Co., Ltd. Companies in the foam tape market are focusing on strategic initiatives to strengthen market position and expand global reach. A primary focus is placed on product innovation, with manufacturers developing advanced adhesive systems that deliver higher bonding strength, improved durability, and enhanced resistance to environmental stressors. Investments in research and development are supporting the creation of customized foam tape solutions tailored to specific industrial requirements, including variations in thickness, density, and adhesive composition. Companies are also expanding production capabilities to meet rising demand across automotive, construction, and electronics sectors. Strategic partnerships with end-use industries are helping strengthen supply chain integration and improve application-specific performance solutions. Sustainability is becoming a key priority, with firms increasingly adopting low-VOC materials and recyclable components to align with environmental regulations.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Resin

- 2.2.3 Technology

- 2.2.4 Tape Type

- 2.2.5 Foam Type

- 2.2.6 End Use Industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Resin, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Acrylic

- 5.3 Rubber

- 5.4 Silicone

- 5.5 Ethylene Vinyl Acetate (EVA)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-based

- 6.3 Water-based

- 6.4 Hot melt-based

Chapter 7 Market Estimates and Forecast, By Tape Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Single-sided

- 7.3 Double-sided

Chapter 8 Market Estimates and Forecast, By Foam Type, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Polyethylene (PE) Foam

- 8.3 Polyurethane (PU) Foam

- 8.4 Neoprene Foam

- 8.5 Acrylic Foam

- 8.6 PVC Foam

- 8.7 Others (EPDM, SBR, Cork, etc.)

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Building & Construction

- 9.4 Electrical & Electronics

- 9.5 Aerospace

- 9.6 Packaging

- 9.7 Medical

- 9.8 Furniture

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East & Africa

Chapter 11 Company Profiles

- 11.1 3M Company

- 11.2 Nitto Denko Corporation

- 11.3 Lohmann GmbH & Co. KG

- 11.4 Tesa SE (Tesa Tapes India)

- 11.5 Avery Dennison Corporation

- 11.6 LINTEC Corporation

- 11.7 Scapa Group

- 11.8 Intertape Polymer Group

- 11.9 LAMATEK, Inc.

- 11.10 3F GmbH Klebe- & Kaschiertechnik

- 11.11 Wuxi Canaan Adhesive Technology Co., Ltd.