|

시장보고서

상품코드

2027519

임상시험 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Clinical Trials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

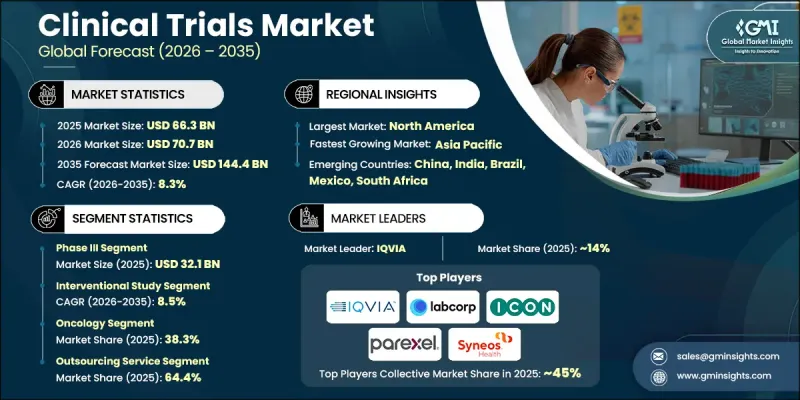

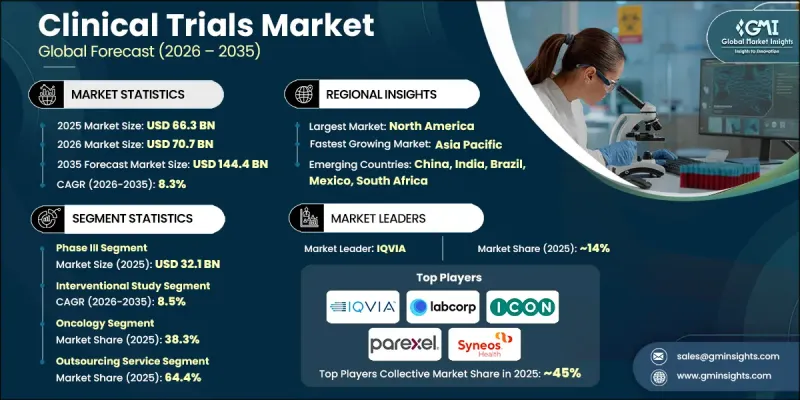

세계의 임상시험 시장은 2025년에 663억 달러로 평가되었고 CAGR 8.3%를 나타내 2035년까지 1,444억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 만성 질환 및 감염성 질환의 유병률 증가, 혁신적인 의약품 및 생물학적 제제에 대한 수요 증가, 제약 및 생명공학 분야의 지속적인 연구 개발 비용 증가에 의해 주도되고 있습니다. 임상시험은 모든 치료 영역에서 새로운 치료법의 안전성, 유효성 및 규제 당국의 승인을 확보하는 데 있어 여전히 의약품 개발의 핵심 요소로 작용하고 있습니다. 특히 바이오의약품, 종양학, 정밀의료 분야의 의약품 파이프라인이 복잡해짐에 따라 임상시험 건수가 증가하고, 첨단 연구 기법의 도입이 촉진되고 있습니다. 이와 함께 디지털 도구, 분산형 시험 모델, AI를 활용한 분석, 실세계 데이터(RWE)의 통합이 점점 더 많이 활용되고 있으며, 피험자 모집, 데이터 품질, 업무 효율성이 향상되어 세계 임상 연구 생태계가 강화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 663억 달러 |

| 예측 금액 | 1,444억 달러 |

| CAGR | 8.3% |

연구 설계에 따라 중재 연구 부문은 규제 당국에 대한 신청과 증거 창출에 있어 중심적인 역할을 하는 중재 연구 부문에 힘입어 2035년까지 연평균 8.5%의 성장률을 나타낼 것으로 예측됩니다. 중재시험은 치료법을 전향적으로 할당하고, 안전성과 유효성에 대한 강력하고 편향되지 않은 임상 데이터를 생성할 수 있다는 점에서 널리 선호되고 있습니다. 이러한 시험은 의약품, 생물학적 제제, 의료기기 개발에 널리 활용되고 있으며, 적응형 시험 설계, 정밀의료 접근법, 첨단 디지털 모니터링 기술이 점점 더 많이 도입되고 있습니다. 전자 데이터 수집(EDC), 원격 모니터링, AI를 활용한 분석의 활용 확대는 임상시험의 효율성, 확장성, 데이터 무결성을 더욱 향상시켜 세계 임상시험 시장에서 중재시험의 우위를 강화하고 있습니다.

2025년에는 전 세계 암 부담 증가와 항암제 개발에 대한 관심이 높아지면서 종양학 분야가 38.3%의 점유율을 차지했습니다. 질병 발병률 증가, 인구의 고령화, 미충족 수요 증가로 인해 전 세계적으로 종양학에 초점을 맞춘 R&D 투자가 지속적으로 증가하고 있습니다. 종양학 시험은 바이오마커, 동반진단, 정밀의학 전략을 도입하여 개인화된 치료 접근법을 가능하게 함으로써 점점 더 복잡해지고 있습니다. 다수의 종양학 약물 승인과 패스트트랙 지정 등 규제적 모멘텀은 종양학 임상시험의 확장을 더욱 촉진하고 있으며, 이 분야는 임상시험 시장의 성장과 혁신에 가장 영향력 있는 기여자로 자리매김하고 있습니다.

북미의 임상시험 시장은 2025년 50.7%의 점유율을 차지했습니다. 이는 첨단 연구 인프라, 제약 및 생명공학 기업의 집중, 그리고 확립된 규제 프레임워크가 뒷받침하고 있습니다. 이 지역은 임상연구에 대한 높은 인지도, 다수의 자격을 갖춘 임상연구자들에 대한 접근성, 특히 종양학 및 희귀질환을 위한 전문 임상연구시설의 가용성 등의 이점을 누리고 있습니다. 미국 국립보건원(NIH)의 대규모 투자를 포함한 강력한 공적 자금 지원과 CRO(임상시험수탁기관)에 대한 아웃소싱 증가가 결합되어 이 지역 전체에 걸쳐 꾸준한 성장을 지속하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 단계별(2022-2035년)

제6장 시장 추산 및 예측 : 연구 설계별(2022-2035년)

제7장 시장 추산 및 예측 : 치료 영역별(2022-2035년)

제8장 시장 추산 및 예측 : 서비스 유형별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.05.20The Global Clinical Trials Market was valued at USD 66.3 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 144.4 billion by 2035.

Market growth is driven by the rising prevalence of chronic and infectious diseases, increasing demand for innovative drugs and biologics, and sustained growth in pharmaceutical and biotechnology R&D spending. Clinical trials remain a critical component of drug development, ensuring the safety, efficacy, and regulatory approval of new therapies across therapeutic areas. Growing complexity in drug pipelines, particularly in biologics, oncology, and precision medicine, is accelerating trial volumes and driving adoption of advanced trial methodologies. In parallel, the increasing use of digital tools, decentralized trial models, AI-driven analytics, and real-world evidence integration is improving patient recruitment, data quality, and operational efficiency, thereby strengthening the global clinical research ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $66.3 Billion |

| Forecast Value | $144.4 Billion |

| CAGR | 8.3% |

Based on study design, the interventional study segment will grow at a CAGR of 8.5% through 2035, supported by its central role in regulatory submissions and evidence generation. Interventional trials are widely preferred due to their ability to prospectively assign treatments and generate robust, unbiased clinical data on safety and efficacy. These studies are extensively used across drug, biologic, and medical device development and increasingly incorporate adaptive trial designs, precision medicine approaches, and advanced digital monitoring technologies. The growing use of electronic data capture, remote monitoring, and AI-powered analytics is further enhancing trial efficiency, scalability, and data integrity, reinforcing the dominance of interventional studies within the global clinical trials market.

The oncology segment held 38.3% share in 2025, driven by the rising global cancer burden and increasing focus on cancer drug development. Growing incidence rates, aging populations, and significant unmet clinical needs continue to drive oncology-focused R&D investments worldwide. Oncology trials are becoming more complex, incorporating biomarkers, companion diagnostics, and precision medicine strategies to enable personalized treatment approaches. Regulatory momentum, including a high volume of oncology drug approvals and fast-track designations, further supports the expansion of oncology trials, positioning this segment as the most influential contributor to growth and innovation in the clinical trials market.

North America Clinical Trials Market held 50.7% share in 2025, supported by advanced research infrastructure, a strong concentration of pharmaceutical and biotechnology companies, and a well-established regulatory framework. The region benefits from high awareness of clinical research, access to a large pool of qualified investigators, and the availability of specialized trial sites, particularly for oncology and rare diseases. Strong public funding support, including significant investments from the National Institutes of Health, combined with increasing outsourcing to Contract Research Organizations (CROs), continues to drive steady growth across the region.

Key players operating in the Global Clinical Trials Market include IQVIA Holdings Inc., ICON plc, Laboratory Corporation of America Holdings (Covance Inc.), Charles River Laboratories International, Inc., Parexel International Corporation, Syneos Health, Medpace, SGS SA, WuXi AppTec Co., Ltd., Worldwide Clinical Trials, ClinChoice, Celerion, Veeda, Qserve, The Emmes Company, and Pharmaceutical Product Development (Thermo Fisher Scientific). Companies operating in the Clinical Trials Market are strengthening their market position through strategic outsourcing models, geographic expansion, and technology-driven service innovation. Leading players are investing heavily in decentralized and hybrid trial solutions, leveraging digital platforms, remote patient monitoring, and AI-based analytics to accelerate trial timelines and improve patient engagement. Partnerships and collaborations with pharmaceutical sponsors, biotechnology firms, and academic institutions are widely adopted to expand therapeutic expertise and access diverse patient populations. Additionally, companies are expanding their presence in high-growth regions such as the Asia Pacific to capitalize on cost advantages and faster recruitment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Phase trends

- 2.2.3 Study design trends

- 2.2.4 Therapeutic area trends

- 2.2.5 Service type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases across the globe

- 3.2.1.2 Growing demand for outsourcing clinical trials to CROs

- 3.2.1.3 Rise in government and non-government funding for clinical trials

- 3.2.1.4 Growing opportunities for conducting clinical trials in countries in Asia Pacific

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of standard-of-care coverage from insurance providers

- 3.2.2.2 Infrastructural barriers and social hurdles

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of decentralized clinical trials (DCTs)

- 3.2.3.2 Integration of artificial intelligence and advanced analytics

- 3.2.1 Growth drivers

- 3.3 Clinical trials volume analysis (Driven by Primary Research)

- 3.3.1 Clinical trials volume analysis, by region, 2022 - 2025

- 3.3.2 Clinical trials volume analysis, by phase of development, 2022 - 2025

- 3.3.3 Clinical trials volume analysis, by indication, 2022 - 2025

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.3.1 Singapore

- 3.4.3.2 Malaysia

- 3.4.3.3 Indonesia

- 3.4.3.4 Thailand

- 3.4.3.5 South Korea

- 3.4.3.6 Philippines

- 3.5 Clinical trials - Asia Pacific advantage (Driven by Primary Research)

- 3.6 Impact of AI and Gen AI on the market

- 3.7 Porters analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Phase, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Phase I

- 5.3 Phase II

- 5.4 Phase III

- 5.5 Phase IV

Chapter 6 Market Estimates and Forecast, By Study Design, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Interventional study

- 6.3 Observational study

- 6.4 Expanded access study

Chapter 7 Market Estimates and Forecast, By Therapeutic Area, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Autoimmune disease

- 7.3 Oncology

- 7.4 Cardiology

- 7.5 Infectious disease

- 7.6 Dermatology

- 7.7 Ophthalmology

- 7.8 Neurology

- 7.9 Hematology

- 7.10 Other therapeutic areas

Chapter 8 Market Estimates and Forecast, By Service Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Outsourcing service

- 8.3 In-house service

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.3.8 Switzerland

- 9.3.9 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.4.9 Thailand

- 9.4.10 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.5.5 Peru

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Cadiya (Clinipace)

- 10.2 Celerio

- 10.3 Charles River Laboratories

- 10.4 ClinChoice

- 10.5 ICON plc

- 10.6 IQVIA HOLDINGS

- 10.7 Labcorp Holding (Covance )

- 10.8 Medpace

- 10.9 Parexel International Corporation

- 10.10 Pharmaceutical Product Development (Thermo Fisher Scientific)

- 10.11 Qserve

- 10.12 SGS SA

- 10.13 Syneos Health

- 10.14 The Emmes Company

- 10.15 Veeda

- 10.16 Worldwide Clinical Trials

- 10.17 Wuxi AppTec Co.