|

시장보고서

상품코드

2027526

전기 트랙터 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Electric Tractor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

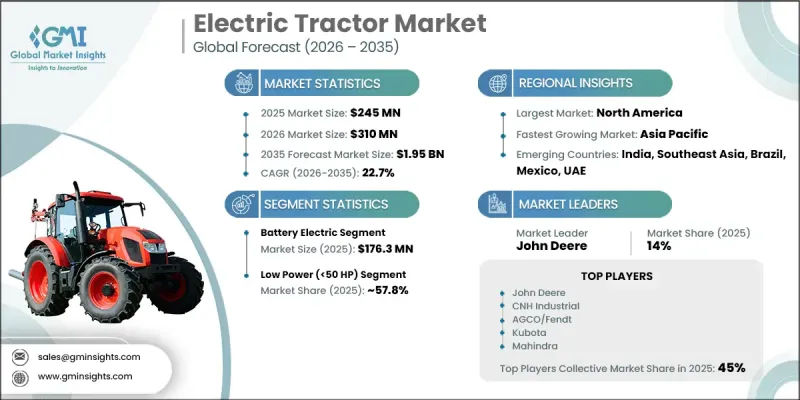

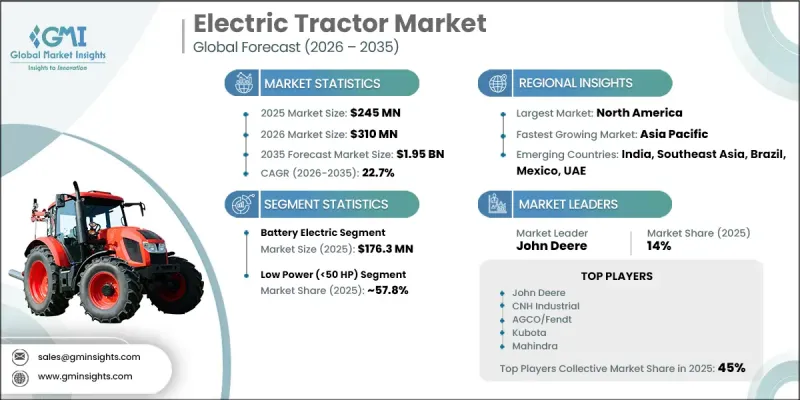

세계의 전기 트랙터 시장은 2025년에 2억 4,500만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 22.7%를 나타내 19억 5,000만 달러에 이를 것으로 추정되고 있습니다.

배출가스 저감, 운영 비용 절감, 장기적인 지속가능성 향상을 위해 농업 분야에서 전기화로의 전환이 진행됨에 따라 시장은 강한 추진력을 보이고 있습니다. 오프로드 농기계에서 배출되는 온실 가스 배출을 억제하기 위한 규제 압력이 높아지면서 주요 농업 지역에서의 도입이 크게 가속화되고 있습니다. 또한, 각국 정부는 보조금, 세제 혜택, 저렴한 융자 프로그램 등의 재정적 인센티브를 통해 이러한 전환을 지원하고 있으며, 이를 통해 농부들이 전기 트랙터 도입을 보다 경제적으로 실현할 수 있도록 돕고 있습니다. 동시에 배터리 시스템과 전기 구동 시스템의 급속한 발전으로 인해 성능에 대한 기대치도 변화하고 있습니다. 에너지 밀도, 충전 속도, 배터리 수명이 향상되어 가동 주기가 길어지고, 농업용으로도 폭넓게 활용할 수 있게 되었습니다. 배터리 비용의 감소는 도입 비용을 더욱 절감하고 총소유비용(TCO)을 개선하는 데에도 기여하고 있습니다. 파워 일렉트로닉스의 발전으로 토크 전달 성능도 향상되어 전기 트랙터는 가혹한 농작업에도 대응할 수 있게 되었습니다. 이 트랙터는 기존 디젤 모델보다 기계 부품이 적기 때문에 유지 보수에 대한 부담이 적고 운영 효율이 높습니다. 기술이 계속 성숙해짐에 따라 전기 트랙터는 실험적인 대안이 아닌 실용적이고 생산성을 중시하는 농기계로 점점 더 많이 인식되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 2억 4,500만 달러 |

| 예측액 | 19억 5,000만 달러 |

| CAGR | 22.7% |

배터리식 트랙터 시장은 2025년 1억 7,630만 달러 시장 규모를 기록했습니다. 추진 방식별로 보면, 이 시장에는 배터리식, 하이브리드식, 연료전지식 트랙터가 포함되며, 각기 다른 운영 요구에 맞게 설계되어 있습니다. 배터리식 모델은 다른 구성에 비해 기술 기반이 더 성숙하고 상용화 준비가 잘 되어 있어 시장을 선도하고 있습니다. 간소화된 아키텍처는 유지보수 요구 사항 감소, 시스템 복잡성 감소, 소유 비용 예측 가능성 향상 등의 이점을 제공합니다. 이러한 시스템은 특히 단시간에서 중시간의 농업 활동에 효과적이며, 특히 저출력 및 중출력 농업 이용 사례에서 현재 배터리 성능의 한계에 잘 부합합니다.

50마력 미만의 트랙터로 정의되는 저출력 부문은 2025년 57.8%의 점유율을 차지했습니다. 이 카테고리가 선도적인 위치를 차지하는 이유는 전기 구동 시스템의 능력과 높은 친화력을 가지고 있기 때문입니다. 저출력 트랙터는 일반적으로 살포, 경운, 운반, 밭 관리 등 비교적 가벼운 작업의 농업용으로 사용되기 때문입니다. 이러한 작업은 짧은 가동 시간 주기와 적당한 토크 출력을 필요로 하기 때문에 현재 배터리용량과 충전 인프라의 제약에 잘 부합합니다. 특히 높은 견인력보다 기동성과 정확성이 중시되는 소규모 농장, 과수원, 포도원 및 세분화된 농지에서 수요가 두드러집니다. 낮은 구매 비용과 간소화된 충전 요건은 비용에 민감한 사용자들 사이에서 보급을 더욱 촉진하고 있습니다.

2025년 미국 전기 트랙터 시장은 76%의 점유율을 차지하며 8,130만 달러 시장 규모를 창출했습니다. 이 나라의 선도적 지위는 탄탄한 농기계 생태계, 높은 투자 능력, 그리고 선진 농업 기술의 조기 도입에 의해 뒷받침되고 있습니다. 연료비 상승, 노동력 부족, 그리고 작업 효율성 향상에 대한 필요성으로 인해 농부들은 점점 더 전기 트랙터로 전환하고 있습니다. 연방 및 주정부 차원의 무공해 장비 보급을 위한 지원 인센티브 프로그램도 특히 지속가능성 목표가 까다로운 지역에서의 도입을 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 추진 방식별(2022-2035년)

제6장 시장 추산 및 예측 : 배터리별(2022-2035년)

제7장 시장 추산 및 예측 : 출력별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 유통 채널별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

KTH 26.05.20The Global Electric Tractor Market was valued at USD 245 million in 2025 and is estimated to grow at a CAGR of 22.7% to reach USD 1.95 billion by 2035.

The market is gaining strong momentum as agriculture increasingly shifts toward electrification to reduce emissions, lower operational costs, and improve long-term sustainability. Growing regulatory pressure to curb greenhouse gas emissions from off-road agricultural machinery is significantly accelerating adoption across key farming regions. Governments are also supporting this transition through financial incentives such as subsidies, tax benefits, and affordable financing programs, making electric tractors more commercially viable for farmers. At the same time, rapid advancements in battery systems and electric drivetrains are reshaping performance expectations. Improvements in energy density, charging speed, and battery lifespan are enabling longer operational cycles and broader use across farming applications. Declining battery costs are further reducing acquisition expenses and improving the total cost of ownership. Enhancements in power electronics are also improving torque delivery, allowing electric tractors to handle demanding agricultural workloads. With fewer mechanical components than conventional diesel models, these tractors require less maintenance and offer higher operational efficiency. As technology continues to mature, electric tractors are increasingly being recognized as practical, productivity-focused agricultural machines rather than experimental alternatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $245 Million |

| Forecast Value | $1.95 Billion |

| CAGR | 22.7% |

The battery electric tractors segment generated USD 176.3 million in 2025. Across propulsion types, the segment includes battery electric, hybrid electric, and fuel cell electric tractors, each designed to meet different operational needs. Battery electric models lead due to their more developed technology base and stronger commercial readiness compared to other configurations. Their simplified architecture supports lower maintenance requirements, reduced system complexity, and more predictable ownership costs. These systems are particularly effective for short- to medium-duration farming activities, aligning well with current battery performance limitations, especially in low- and mid-power agricultural use cases.

The low power segment, defined as tractors below 50 HP, held a share of 57.8% in 2025. This category leads due to its strong compatibility with electric drivetrain capabilities, as low-power tractors are typically used for lighter agricultural tasks such as spraying, cultivation, hauling, and field maintenance. These operations require shorter runtime cycles and moderate torque output, making them well-suited to current battery capacities and charging infrastructure constraints. Demand is particularly strong in small farms, orchards, vineyards, and fragmented landholdings where maneuverability and precision are more important than high pulling power. Lower purchase costs and simplified charging requirements further support widespread adoption among cost-sensitive users.

U.S. Electric Tractor Market accounted for 76% share in 2025, generating USD 81.3 million. The country's leadership position is supported by a strong agricultural machinery ecosystem, high investment capacity, and early adoption of advanced farming technologies. Farmers are increasingly turning toward electric tractors due to rising fuel expenses, labor shortages, and the need to improve operational efficiency. Supportive federal and state-level incentive programs aimed at promoting zero-emission equipment are also accelerating adoption, particularly in regions with stricter sustainability targets.

Major companies operating in the Global Electric Tractor Market include CNH Industrial, AGCO Corporation, John Deere (Deere & Company), Mahindra & Mahindra, Kubota Corporation, CLAAS, Massey Ferguson Limited, Yanmar Holdings Co., Ltd., Escorts Kubota Limited, Deutz-Fahr (SDF Group), Farmtrac (Escorts Group), Monarch Tractor, Solectrac, NAIO Technologies, AutoNxt Automation Pvt. Ltd., Cellestial E-Mobility, Alke, Lely Group, Motivo Engineering, and Ztractor. Companies in the Electric Tractor Market are focusing on strengthening competitiveness through continuous product innovation and advancement in battery and drivetrain technologies. Significant investments in R&D are enabling improvements in energy efficiency, torque performance, and charging speed. Manufacturers are also expanding production capabilities to scale output and reduce unit costs. Strategic collaborations with battery suppliers and technology firms help accelerate innovation cycles and improve supply chain stability. Many players are introducing flexible financing models and leasing options to increase affordability for farmers. Expansion into emerging agricultural markets is further supporting revenue diversification.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion type

- 2.2.3 Battery

- 2.2.4 Power

- 2.2.5 Application

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Environmental regulations and policy support

- 3.2.1.2 Technological advancements and battery cost reduction

- 3.2.1.3 Operating cost efficiency and farm economics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial acquisition cost

- 3.2.2.2 Charging infrastructure and operational limitations

- 3.2.3 Opportunities

- 3.2.3.1 Integration with smart and precision farming systems

- 3.2.3.2 Growing demand from small and specialty farming segments

- 3.2.4 Growth potential analysis

- 3.2.5 Future market trends

- 3.2.6 Technology and innovation landscape

- 3.2.6.1 Current technological trends

- 3.2.6.2 Emerging technologies

- 3.2.7 Pricing Analysis (driven by primary research)

- 3.2.7.1 Historical price trend analysis

- 3.2.7.2 Regional Price Variations

- 3.2.7.3 Price Comparison: electric vs diesel tractors

- 3.2.7.4 Price elasticity & consumer sensitivity

- 3.2.8 Regulatory Framework

- 3.2.8.1 Emission standards & agricultural equipment regulations

- 3.2.8.2 Government subsidies & incentive programs

- 3.2.8.3 Safety & certification requirements

- 3.2.8.4 Import/export regulations & trade policies

- 3.2.8.5 Rural electrification policies

- 3.2.8.6 Carbon credit & sustainability mandates

- 3.2.9 Porter's five forces analysis

- 3.2.10 PESTEL analysis

- 3.2.11 Consumer behavior analysis

- 3.2.11.1 Purchasing patterns

- 3.2.11.2 Preference analysis

- 3.2.11.3 Regional variations in consumer behavior

- 3.2.11.4 Impact of e-commerce on buying decisions

- 3.2.12 Trade data analysis - HS Code: 8701.24 (new) (driven by paid database)

- 3.2.12.1 Import/export volume & value trends

- 3.2.12.2 Key trade corridors & tariff impact

- 3.2.12.3 Trade flow analysis by region

- 3.2.12.4 HS code classification & trade documentation

- 3.2.13 Impact of AI & Generative AI on the Market

- 3.2.13.1 AI-driven disruption of existing business models

- 3.2.13.2 GenAI use cases & adoption roadmap by segment

- 3.2.13.3 Precision agriculture integration (AI-enabled field optimization)

- 3.2.13.4 Predictive maintenance & fleet management applications

- 3.2.13.5 Risks, limitations & regulatory considerations

- 3.2.1 Growth drivers

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Battery electric

- 5.3 Hybrid electric

- 5.4 Fuel cell electric

Chapter 6 Market Estimates and Forecast, By Battery, 2022 - 2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Lithium-ion

- 6.3 Lead-Acid

- 6.4 Others (solid-state, sodium-ion, etc.)

Chapter 7 Market Estimates and Forecast, By Power, 2022 - 2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Low power (<50 HP)

- 7.3 Medium power (50-100 HP)

- 7.4 High power (>100 HP)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Agriculture

- 8.2.1 Field operations

- 8.2.2 Orchard & vineyard operations

- 8.2.3 Livestock & dairy farm applications

- 8.2.4 Others

- 8.3 Utility

- 8.3.1 Landscaping & grounds maintenance

- 8.3.2 Golf courses & sports fields

- 8.3.3 Municipal & public spaces

- 8.4 Industrial

- 8.4.1 Construction site operations

- 8.4.2 Material handling & logistics

- 8.4.3 Municipal services & waste management

- 8.4.4 Airport & port operations

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AGCO Corporation

- 11.2 Alke

- 11.3 AutoNxt Automation Pvt. Ltd.

- 11.4 Cellestial E-Mobility

- 11.5 CLAAS

- 11.6 CNH Industrial

- 11.7 Deutz-Fahr (SDF Group)

- 11.8 Escorts Kubota Limited

- 11.9 Farmtrac (Escorts Group)

- 11.10 John Deere (Deere & Company)

- 11.11 Kubota Corporation

- 11.12 Lely Group

- 11.13 Mahindra & Mahindra

- 11.14 Massey Ferguson Limited

- 11.15 Monarch Tractor

- 11.16 Motivo Engineering

- 11.17 NAIO Technologies

- 11.18 Solectrac

- 11.19 Yanmar Holdings Co., Ltd.

- 11.20 Ztractor