|

시장보고서

상품코드

2027533

식품 산업용 열 처리 장비 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Food Industry Heat Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

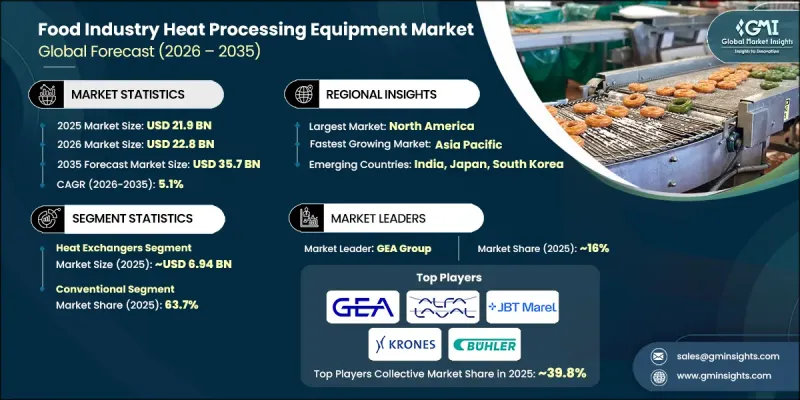

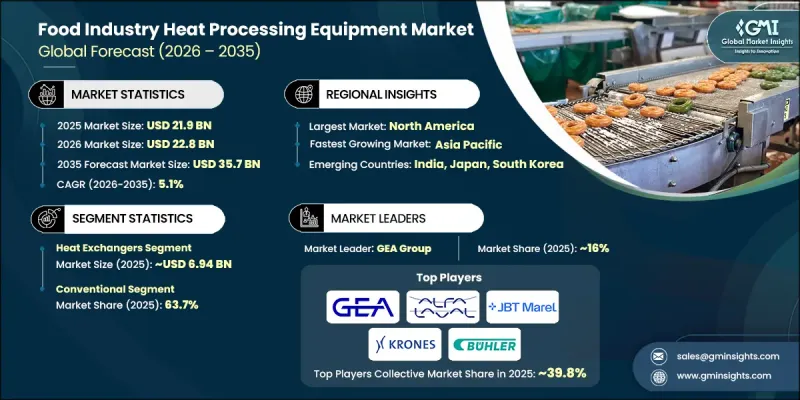

세계의 식품 산업용 열 처리 장비 시장은 2025년에 219억 달러로 평가되었고 CAGR 5.1%를 나타내 2035년까지 357억 달러에 이를 것으로 추정되고 있습니다.

세계 식음료 가공 부문의 확대는 첨단 열 처리 시스템에 대한 수요를 크게 견인하고 있습니다. 식품 제조업체는 제품의 안전성을 보장하고, 유통기한을 연장하고, 전체 생산주기 동안 일관된 품질을 유지하기 위해 효율적인 열 처리 장비에 의존하고 있습니다. 포장식품 및 가공식품의 소비가 증가함에 따라 대규모 운영에 대응할 수 있는 대용량, 고효율 시스템에 대한 요구가 증가하고 있습니다. 열 처리는 엄격한 품질 관리 기준을 지원하면서 유해한 미생물을 제거하는 데 중요한 역할을 합니다. 식품 안전에 대한 규제 요건 강화도 첨단 제어 가열 기술의 도입을 촉진하고 있습니다. 이에 따라 각 제조업체들은 생산성 향상, 운영비 절감, 에너지 효율 향상을 위한 혁신적인 설비 투자를 진행하고 있습니다. 또한, 열의 균일한 분포와 정밀한 온도 관리를 통해 식품 가공 공정 전반에 걸쳐 신뢰성과 일관성을 보장하는 시스템에 대한 관심도 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 219억 달러 |

| 예측액 | 357억 달러 |

| CAGR | 5.1% |

열교환기 부문은 2025년 69억 4,000만 달러 시장 규모를 기록했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. 이 부문은 각 가공 공정에서 온도 관리에 필수적인 역할을 하기 때문에 시장에서 큰 비중을 차지하고 있습니다. 열교환기는 제조 공정 전반에 걸쳐 일관되고 효율적인 온도 조절을 가능하게 함으로써 제품의 안전성 향상, 품질 유지 및 유통기한 연장에 기여하고 있습니다.

2025년 기존 열 기술은 63.7%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 4.6%의 성장률을 나타낼 것으로 예측됩니다. 이 부문은 조작의 편의성, 신뢰성 및 비용 효율성으로 인해 계속해서 선도적인 위치를 유지하고 있습니다. 다양한 가공 시설에서 널리 사용되고 있는 기존 시스템은 사용 편의성, 적은 유지보수, 그리고 신뢰할 수 있는 성능으로 평가받고 있습니다. 저렴하고 효율적인 가공 솔루션에 대한 수요가 증가함에 따라 이러한 기술의 채택이 계속 증가하고 있습니다.

미국의 식품 산업 열 처리 장비 시장은 2025년 44억 달러 규모에 달했으며, 2035년까지 연평균 5.1%의 성장률을 나타낼 것으로 예측됩니다. 시장 성장은 가공식품에 대한 수요 증가와 일관된 품질 및 안전 기준에 대한 요구로 인해 주도되고 있습니다. 제조업체들은 효율성 향상, 규제 프레임워크 준수, 생산 성과 최적화를 위해 첨단 열 처리 시스템에 투자하고 있습니다. 장비 설계의 지속적인 혁신은 에너지 효율 향상, 온도 정확도 개선, 가공 중 제품 손실 최소화에 중점을 두고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 조작 방식별(2022-2035년)

제7장 시장 추산 및 예측 : 가열 기술별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 유통 채널별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

KTHThe Global Food Industry Heat Processing Equipment Market was valued at USD 21.9 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 35.7 billion by 2035.

Expansion in the global food and beverage processing sector is significantly driving demand for advanced thermal processing systems. Food manufacturers rely on efficient heat processing equipment to ensure product safety, extend shelf life, and maintain consistent quality throughout production cycles. The rising consumption of packaged and processed food products is accelerating the need for high-capacity, efficient systems that can handle large-scale operations. Thermal processing plays a critical role in eliminating harmful microorganisms while supporting strict quality control standards. Increasing regulatory requirements related to food safety are also encouraging the adoption of advanced and controlled heating technologies. In response, manufacturers are investing in innovative equipment designed to improve productivity, reduce operational costs, and enhance energy efficiency. There is also a growing focus on systems that provide uniform heat distribution and precise temperature management, ensuring reliability and consistency across food processing operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.9 Billion |

| Forecast Value | $35.7 Billion |

| CAGR | 5.1% |

The heat exchangers segment generated USD 6.94 billion in 2025 and is expected to grow at a CAGR of 5% between 2026 and 2035. This segment holds a substantial share of the market due to its essential role in maintaining controlled temperatures across processing stages. Heat exchangers contribute to improved product safety, quality retention, and extended shelf stability by enabling consistent and efficient thermal regulation throughout production processes.

In 2025, the conventional heat technology accounted for 63.7% share and is anticipated to grow at a CAGR of 4.6% during 2026-2035. This segment continues to lead due to its operational simplicity, reliability, and cost-effectiveness. Widely adopted across various processing facilities, conventional systems are valued for their ease of use, low maintenance requirements, and dependable performance. The growing need for accessible and efficient processing solutions continues to support the adoption of these technologies.

United States Food Industry Heat Processing Equipment Market captured USD 4.4 billion in 2025 and is expected to grow at a CAGR of 5.1% through 2035. Market growth is driven by increasing demand for processed food products and the need for consistent quality and safety standards. Manufacturers are investing in advanced thermal processing systems to improve efficiency, ensure compliance with regulatory frameworks, and optimize production outcomes. Continuous innovation in equipment design is focused on enhancing energy efficiency, improving temperature accuracy, and minimizing product loss during processing.

Key companies operating in the Global Food Industry Heat Processing Equipment Market include Alfa Laval, GEA Group, SPX FLOW, Tetra Pak, Buhler Group, JBT Corporation, Krones AG, Marel, Heat and Control, Inc., HRS Heat Exchangers, Actini Group, KHS GmbH, IDMC Limited, FMT Food Machinery & Technology, and Scherjon Dairy Equipment. Companies in the Food Industry Heat Processing Equipment Market are strengthening their competitive position through continuous innovation, strategic collaborations, and expansion of product offerings. Many manufacturers are investing in research and development to introduce energy-efficient systems with advanced temperature control and automation capabilities. Partnerships with food processing companies help in customizing solutions tailored to specific operational requirements. Firms are also focusing on expanding their global footprint by entering emerging markets and enhancing distribution networks. Digital integration and smart monitoring technologies are being adopted to improve operational efficiency and equipment performance. Additionally, companies are emphasizing after-sales services and maintenance support to build long-term customer relationships and ensure sustained market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of the global food and beverage processing industry

- 3.2.1.2 Expansion of ready-to-eat and convenience food segments

- 3.2.1.3 Strict food safety and hygiene regulations in food manufacturing

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High capital investment required for industrial heat processing systems

- 3.2.2.2 Energy-intensive nature of thermal food processing operations

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of automated and digitally controlled processing systems

- 3.2.3.2 Rising demand for energy recovery and sustainable heating technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research) (2019-2024)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 TCO analysis: CAPEX vs OPEX considerations

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume & value trends (HS code 8438) (driven by paid database)

- 3.10.2 Key trade corridors & tariff impact (driven by paid database)

- 3.10.3 Leading exporting & importing countries

- 3.11 Capacity & production landscape (driven by primary research)

- 3.11.1 Installed capacity by region & key producer (driven by primary research)

- 3.11.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Heat Exchangers

- 5.3 Pasteurizers & Sterilizers

- 5.4 Evaporators

- 5.5 Dehydration Equipment

- 5.6 Fryers

- 5.7 Ovens

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Operation, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automatic

- 6.4 Fully automatic

Chapter 7 Market Estimates & Forecast, By Heat Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Conventional (gas, electricity)

- 7.3 Infrared

- 7.4 Microwave

- 7.5 Induction

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Bakery and confectionery (bread, cakes).

- 8.3 Meat, poultry, and seafood.

- 8.4 Dairy products (milk, cheese).

- 8.5 Fruits and vegetables.

- 8.6 Beverages (juices, soft drinks).

- 8.7 Snacks (chips, nuts)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Alfa Laval

- 11.2 Tetra Pak

- 11.3 GEA Group

- 11.4 Buhler Group

- 11.5 JBT Corporation

- 11.6 SPX FLOW

- 11.7 Krones AG

- 11.8 Marel

- 11.9 Heat and Control, Inc.

- 11.10 HRS Heat Exchangers

- 11.11 IDMC Limited

- 11.12 Scherjon Dairy Equipment

- 11.13 KHS GmbH

- 11.14 FMT Food Machinery & Technology

- 11.15 Actini Group