|

시장보고서

상품코드

2027575

드론 카메라 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Drone Camera Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

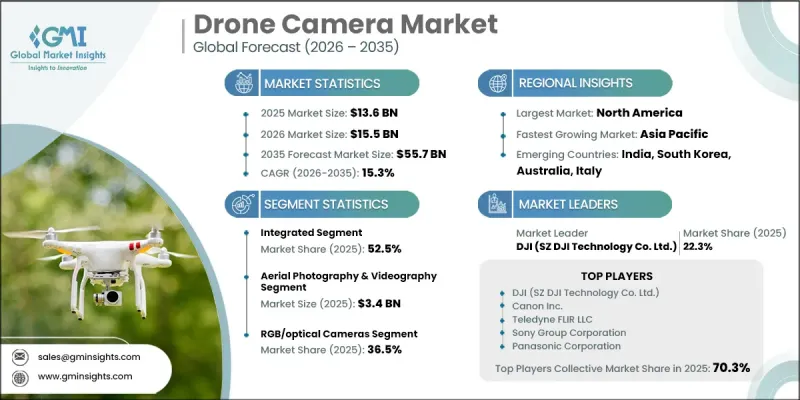

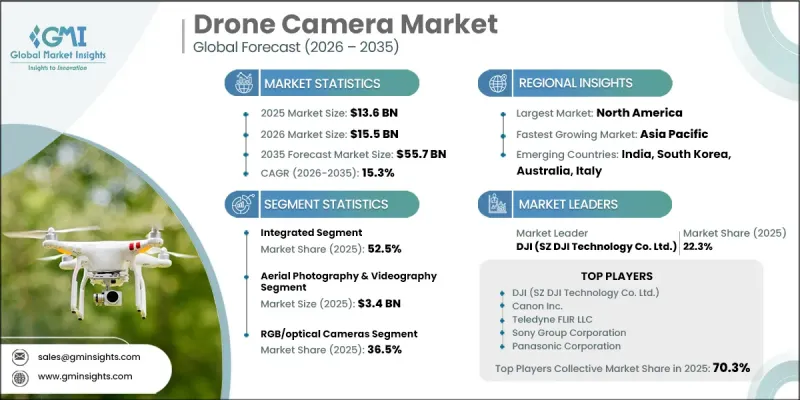

세계의 드론 카메라 시장은 2025년에 136억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15.3%를 나타내 557억 달러에 이를 것으로 추정되고 있습니다.

이 시장은 다양한 산업 분야에서 고해상도 영상 솔루션에 대한 수요가 증가함에 따라 강력한 성장세를 보이고 있습니다. 드론을 활용한 점검 서비스의 상용화가 진행되면서 도입을 더욱 촉진하고 있으며, 정밀농업의 발전으로 첨단 영상시스템에 대한 수요는 계속 가속화되고 있습니다. AI를 활용한 영상 기술의 통합은 데이터의 정확성과 운영 효율성을 향상시켜 상업 및 산업 분야에서 활용도를 높이고 있습니다. 동시에 영화 촬영 및 디지털 미디어 제작에서 항공 촬영 컨텐츠에 대한 수요 증가도 지속적인 성장에 기여하고 있습니다. 조직은 인프라 감시, 보안, 매핑 등의 용도로 드론을 이용한 영상 촬영에 대한 의존도가 높아지고 있습니다. 이러한 분야에서는 고화질 시각적 데이터가 의사결정을 개선하는 데 도움을 줍니다. 열화상 및 다중 스펙트럼 이미징을 포함한 센서 기술의 지속적인 발전은 응용 범위를 더욱 확장하고 자율 운영 능력을 강화하여 드론 카메라를 현대 데이터 기반 산업의 중요한 구성 요소로 자리 매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 136억 달러 |

| 예측액 | 557억 달러 |

| CAGR | 15.3% |

2025년 기준, 통합형 부문은 52.5%의 점유율을 차지했습니다. 이 부문은 카메라, 센서, 안정화 시스템이 통합된 시스템으로 설계되어 일관된 성능을 보장하기 때문에 지속적으로 시장을 선도하고 있습니다. 이러한 솔루션은 운영 안정성, 도입 용이성, 상용 드론 플랫폼과의 호환성으로 인해 널리 선호되고 있습니다. 간소화된 기능성은 효율적인 영상 솔루션을 필요로 하는 다양한 산업 분야에서 널리 보급되고 있습니다.

항공 사진 및 영상 촬영 부문은 2025년 34억 달러 시장 규모를 기록했습니다. 이 부문의 성장은 미디어 제작, 부동산 시각화, 여행 관련 컨텐츠 제작의 강력한 수요에 의해 주도되고 있습니다. 고해상도 촬영 기능과 첨단 손떨림 보정 시스템의 결합으로 드론 카메라는 전문적인 시각적 컨텐츠 제작에 필수적인 도구로 자리 잡았으며, 이 분야의 지속적인 성장을 뒷받침하고 있습니다.

2025년 북미의 드론 카메라 시장은 38.5%의 점유율을 차지했습니다. 이 지역 시장 성장은 인프라 점검, 정밀 농업, 공공 안전 업무에서의 사용 확대에 힘입어 성장하고 있습니다. AI 통합 이미징 시스템에 대한 강한 수요는 에너지, 건설, 방위 산업에서 특히 두드러집니다. 자율 및 분석 기반 드론 기술에 대한 공공 및 민간 부문의 투자가 증가하면서 이 지역 시장 확대가 더욱 가속화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 카메라 기술별(2022-2035년)

제6장 시장 추산 및 예측 : 페이로드 구성별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자 산업별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.05.20The Global Drone Camera Market was valued at USD 13.6 billion in 2025 and is estimated to grow at a CAGR of 15.3% to reach USD 55.7 billion by 2035.

The market is witnessing strong expansion driven by rising demand for high-resolution imaging solutions across multiple industries. Growing commercialization of drone-based inspection services is further strengthening adoption, while precision agriculture continues to accelerate demand for advanced imaging systems. Increasing integration of AI-powered imaging technologies is enhancing data accuracy and operational efficiency, supporting wider usage across commercial and industrial applications. At the same time, the rising need for aerial content in cinematography and digital media production is contributing to sustained growth. Organizations are increasingly relying on drone-based imaging for infrastructure monitoring, surveillance, and mapping applications, where high-detail visual data supports improved decision-making. Continuous improvements in sensor technologies, including thermal and multispectral imaging, are further expanding application scope and strengthening autonomous operational capabilities, positioning drone cameras as a key component in modern data-driven industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.6 Billion |

| Forecast Value | $55.7 Billion |

| CAGR | 15.3% |

The integrated segment held a 52.5% share in 2025. This segment continues to dominate due to its pre-configured design, where cameras, sensors, and stabilization systems are combined into a unified system that ensures consistent performance. These solutions are widely preferred due to their operational reliability, ease of deployment, and compatibility with commercial drone platforms. Their simplified functionality supports broad adoption across industries requiring efficient imaging solutions.

The aerial photography and videography segment generated USD 3.4 billion in 2025. Growth in this segment is driven by strong demand from media production, property visualization, and travel-related content creation. High-resolution imaging capabilities combined with advanced stabilization systems have made drone cameras essential tools for professional visual content development, supporting the continued expansion of this segment.

North America Drone Camera Market accounted for 38.5% share in 2025. Market growth in the region is supported by rising utilization across infrastructure inspection, precision agriculture, and public safety operations. Strong demand for AI-integrated imaging systems is particularly evident in industries such as energy, construction, and defense. Increased investment from both public and private sectors in autonomous and analytics-driven drone technologies is further strengthening regional market expansion.

Key companies operating in the Global Drone Camera Market include DJI (SZ DJI Technology Co., Ltd.), Autel Robotics, Skydio Inc., Parrot SA, Yuneec International, Canon Inc., Sony Group Corporation, GoPro, Inc., Intel Corporation, Panasonic Corporation, Teledyne FLIR LLC, Quantum-Systems GmbH, Kespry Inc., Controp Precision Technologies Ltd., Zen Technologies, Guangzhou EHang Intelligent Technology Co., Ltd., Aerialtronics DV B.V., AiDrones GmbH, Bayspec Inc., and WSS. Companies in the Drone Camera Market are focusing on strengthening their competitive position through technological innovation and product advancement. Significant investments are being directed toward AI-enabled imaging systems, sensor integration, and autonomous flight capabilities to enhance operational efficiency. Strategic partnerships with software developers and analytics providers are helping expand application ecosystems. Manufacturers are also emphasizing miniaturization and improved battery performance to increase flight time and imaging quality. Expansion into emerging markets and industry-specific solutions is further supporting revenue growth. In addition, companies are strengthening distribution networks and enhancing after-sales services to improve customer retention and brand loyalty in a highly competitive environment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Camera technology trends

- 2.2.2 Payload configuration trends

- 2.2.3 Application trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-resolution aerial imaging

- 3.2.1.2 Expansion of commercial drone-based inspections globally

- 3.2.1.3 Increasing adoption in agriculture precision monitoring

- 3.2.1.4 Integration of AI-enabled image processing capabilities

- 3.2.1.5 Growth in cinematography and content creation industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced sensor-equipped camera systems

- 3.2.2.2 Stringent airspace and imaging regulatory restrictions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in smart city surveillance infrastructure

- 3.2.3.2 Growth of autonomous drone imaging solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Camera Technology, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 RGB/optical cameras

- 5.3 Thermal/infrared cameras

- 5.4 Multispectral & advanced sensing systems

- 5.5 LiDAR & 3D imaging systems

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Payload Configuration, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Integrated

- 6.3 Semi-integrated

- 6.4 Fully modular

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Aerial photography & videography

- 7.3 Surveying & mapping

- 7.4 Industrial inspection

- 7.5 Agriculture precision management

- 7.6 Environmental monitoring

- 7.7 Surveillance & security

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Agriculture

- 8.3 Construction & infrastructure

- 8.4 Energy & utilities

- 8.5 Defense

- 8.6 Civil public safety

- 8.7 Media & entertainment

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 DJI (SZ DJI Technology Co., Ltd.)

- 10.1.2 Canon Inc.

- 10.1.3 Sony Group Corporation

- 10.1.4 Panasonic Corporation

- 10.1.5 Teledyne FLIR LLC

- 10.1.6 Intel Corporation

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Skydio Inc.

- 10.2.1.2 GoPro, Inc.

- 10.2.1.3 Kespry Inc.

- 10.2.1.4 Bayspec Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Autel Robotics

- 10.2.2.2 Guangzhou EHang Intelligent Technology Co. Ltd.

- 10.2.2.3 Yuneec International

- 10.2.2.4 Zen Technologies

- 10.2.3 Europe

- 10.2.3.1 Parrot SA

- 10.2.3.2 Quantum-Systems GmbH

- 10.2.3.3 Aerialtronics DV B.V.

- 10.2.3.4 AiDrones GmbH

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Controp Precision Technologies Ltd.

- 10.3.2 WSS