|

시장보고서

상품코드

2027581

보호 포장 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Protective Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

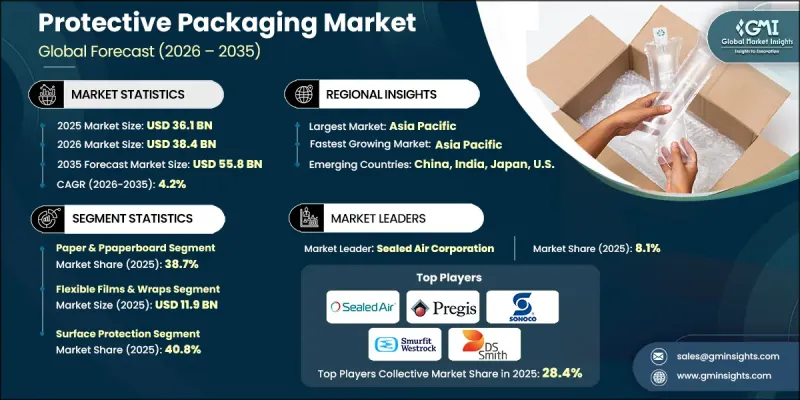

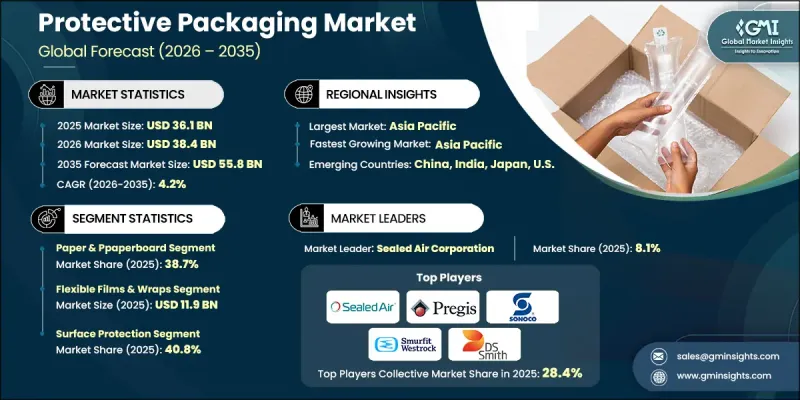

세계의 보호 포장 시장은 2025년에 361억 달러로 평가되었고 CAGR 4.2%를 나타내 2035년까지 558억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 전자상거래 활동의 급속한 확대와 전 세계 라스트마일 배송 업무의 급격한 증가에 의해 주도되고 있으며, 이에 따라 운송 중 제품을 안전하게 보호해야 할 필요성이 증가하고 있습니다. 또한, 세계 전자제품 무역의 지속적인 성장으로 인해 고가의 깨지기 쉬운 제품을 보호할 수 있는 고급 포장 솔루션에 대한 수요가 증가하고 있습니다. 또한, 파손 감소에 초점을 맞춘 물류 성능 기준의 강화로 인해 기업들은 보다 효율적인 포장 시스템을 도입해야 하는 상황에 직면해 있습니다. 재활용이 가능하고 친환경적인 소재로의 전환이 진행되고 있는 것도 업계의 관행을 더욱 변화시키고 있습니다. 한편, 물류 및 운송 네트워크 전반에 걸쳐 효율성, 추적 및 취급 정확도를 향상시키기 위한 자동화 및 스마트 포장 기술이 확산되고 있습니다. 이러한 요인들이 결합되어 현대 세계 공급망에서 중요한 구성 요소로서 보호 포장의 중요성이 더욱 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 361억 달러 |

| 예측액 | 558억 달러 |

| CAGR | 4.2% |

보호 포장 시장의 확대는 전자상거래 플랫폼의 급속한 성장과 라스트마일 배송에 따른 소포 취급량 증가에 의해 크게 뒷받침되고 있습니다. 온라인 소매업의 성장으로 운송 중 파손을 최소화하고 반품률을 낮추며 고객 만족도를 향상시킬 수 있는 안전한 포장 형태에 대한 요구가 크게 증가하고 있습니다. 특히 전자제품 분야에서 국경 간 운송 증가는 내구성이 뛰어난 보호 솔루션에 대한 수요를 더욱 증가시키고 있습니다. 시장 성장은 주요 경제권에서 지속 가능하고 재활용 가능한 대체 포장에 대한 인식이 높아지고 자동 창고 및 주문 처리 시스템에 대한 투자가 증가함에 따라 뒷받침되고 있습니다.

발포 폴리머 부문은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5.3%를 나타낼 것으로 예측됩니다. 발포 폴리머 소재는 경량 구조, 높은 내충격성 및 높은 사용자 정의 가능성으로 인해 전자기기, 의약품, 정밀 소비재 등 섬세한 상품의 포장에 널리 활용되고 있습니다. 우수한 완충 성능과 복잡한 제품 형태에 대한 적응성으로 인해 포장 설계에서 신뢰할 수 있는 보호와 작업 효율성을 모두 원하는 제조업체들이 선호하는 선택이 되었습니다.

표면 보호 부문은 2025년 40.8%의 점유율을 차지했습니다. 이 부문은 보관 및 운송 중 긁힘, 마모, 오염 등의 표면 손상을 방지하기 위해 전자제품, 자동차 부품, 가구의 물류에 널리 사용되고 있습니다. 이러한 수요 증가는 전체 공급망, 특히 소매 중심의 유통망에서 제품의 외관과 기능을 유지해야 할 필요성에 의해 주도되고 있습니다. 또한, 지속가능성에 대한 요구가 높아짐에 따라 재활용 가능한 보호 필름의 채택이 증가하고 있으며, 이는 전 세계 물류 운영에서 이 부문의 성장을 더욱 촉진하고 있습니다.

2025년 미국의 보호 포장 시장은 52억 달러 규모에 달했습니다. 미국 시장의 성장은 인프라 현대화 및 경제 발전을 지원하기 위한 정부 주도의 노력과 밀접한 관련이 있습니다. 미국 환경보호청(EPA)과 같은 규제 당국과 주정부 차원의 환경기관은 순환 경제 모델과 포장 폐기물 감소 프로그램을 적극적으로 추진하고 있으며, 지속 가능한 재료의 채택을 장려하고 있습니다. 전자상거래의 급속한 성장과 지속적인 물류 현대화와 함께 이러한 요인들은 고급 포장 및 내구성 있는 보호 포장 솔루션에 대한 강력한 수요를 주도하고 있으며, 미국은 북미에서 주요 지역 리더로 자리 매김하고 있습니다.

세계의 보호 포장 시장에서 사업을 전개하는 주요 기업으로는 Pregis LLC, Sealed Air Corporation, Smurfit WestRock, Berry Global Inc. Huhtamaki Oyj(Huhtamaki Oyj), 인터내셔널 페이퍼 컴퍼니(International Paper Company), 란팩 홀딩스(Ranpak Holdings Corp.), 프로앰팩 홀딩스( ProAmpac Holdings Inc.), DS 스미스(DS Smith Plc), 인터테이프 폴리머 그룹(Intertape Polymer Group Inc.), 네팹 그룹(Nefab Group), 그리고 스토로팩 한스 라이헨네커( Storopack Hans Reichenecker GmbH) 등이 있습니다. 보호 포장 시장 기업들이 채택하고 있는 주요 전략은 재활용 및 생분해성 소재 개발을 통해 지속가능성에 대한 노력을 강화하는 동시에 첨단 완충 기술에 대한 투자를 확대하는 데 초점을 맞추었습니다. 시장 진출기업들은 효율성 향상과 운영 비용 절감을 위해 포장 업무의 자동화 기능을 적극적으로 강화하고 있습니다. 지리적 확장 및 제품 포트폴리오를 확대하기 위해 전략적 합병 및 인수를 추진하고 있습니다. 또한, 기업들은 전자상거래 및 전자기기 용도에 맞는 가볍고 고성능의 보호재를 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 공급망 통합 및 맞춤형 포장 솔루션을 개선하기 위해 물류 기업 및 소매 기업과의 제휴도 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 소재 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 제품 형태별(2022-2035년)

제7장 시장 추산 및 예측 : 기능별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.05.20The Global Protective Packaging Market was valued at USD 36.1 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 55.8 billion by 2035.

Market expansion is driven by the rapid rise of e-commerce activity and the surge in last-mile delivery operations worldwide, which are increasing the need for reliable product protection during transit. The continuous growth in global electronics trade is also strengthening demand for advanced protective packaging solutions that can safeguard high-value and fragile goods. In addition, stricter logistics performance benchmarks focused on damage reduction are pushing companies to adopt more efficient packaging systems. The increasing shift toward recyclable and eco-friendly materials is further reshaping industry practices, while automation and smart packaging technologies are gaining traction across logistics and shipping networks to improve efficiency, tracking, and handling precision. Collectively, these factors are reinforcing the importance of protective packaging as a critical component of modern global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.1 Billion |

| Forecast Value | $55.8 Billion |

| CAGR | 4.2% |

The expansion of the protective packaging market is strongly supported by the rapid acceleration of e-commerce platforms and rising parcel volumes associated with last-mile deliveries. The growth of online retail has significantly increased the need for secure packaging formats that minimize transit damage, reduce return rates, and improve customer satisfaction. Rising cross-border shipments, particularly in electronics, are further intensifying the demand for durable protective solutions. Market growth is additionally supported by increased investments in automated warehousing and fulfillment systems, alongside rising awareness regarding sustainable and recyclable packaging alternatives across major economies.

The foam polymers segment is projected to register a CAGR of 5.3% during 2026-2035 Foam polymer materials are widely utilized for packaging sensitive goods such as electronics, pharmaceuticals, and precision consumer products due to their lightweight structure, high impact resistance, and customization flexibility. Their superior cushioning performance and adaptability to complex product geometries make them a preferred choice among manufacturers seeking reliable protection combined with operational efficiency in packaging design.

The surface protection segment held a share of 40.8% in 2025. This segment is extensively used across electronics, automotive components, and furniture logistics to prevent surface damage such as scratches, abrasion, and contamination during storage and transportation. Strong demand is driven by the need to preserve product appearance and functionality throughout the supply chain, particularly in retail-focused distribution networks. Additionally, increasing sustainability requirements are encouraging the adoption of recyclable protective films, further supporting segment growth across global logistics operations.

U.S. Protective Packaging Market captured USD 5.2 billion in 2025. Market growth in the United States is closely tied to government-led initiatives supporting infrastructure modernization and economic development. Regulatory bodies such as the EPA, along with state-level environmental agencies, are actively promoting circular economy models and packaging waste reduction programs, encouraging the adoption of sustainable materials. Combined with the rapid growth of e-commerce and ongoing logistics modernization, these factors are driving strong demand for advanced, durable, and environmentally compliant protective packaging solutions, positioning the U.S. as a key regional leader in North America.

The major companies operating in the Global Protective Packaging Market include Pregis LLC, Sealed Air Corporation, Smurfit WestRock, Berry Global Inc., Mondi Group, Sonoco Products Company, Cascades Inc., Huhtamaki Oyj, International Paper Company, Ranpak Holdings Corp., ProAmpac Holdings Inc., DS Smith Plc, Intertape Polymer Group Inc., Nefab Group, and Storopack Hans Reichenecker GmbH. Key strategies adopted by companies in the Protective Packaging Market focus on strengthening sustainability initiatives through recyclable and biodegradable material development while expanding investments in advanced cushioning technologies. Market players are actively enhancing automation capabilities in packaging operations to improve efficiency and reduce operational costs. Strategic mergers and acquisitions are being pursued to expand geographic presence and product portfolios. Companies are also investing heavily in research and development to create lightweight, high-performance protective materials tailored for e-commerce and electronics applications. Partnerships with logistics and retail firms are increasing to improve supply chain integration and customized packaging solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Product format trends

- 2.2.3 Function trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-commerce growth increasing last-mile product protection demand

- 3.2.1.2 Rising electronics shipments requiring anti-static cushioning solutions

- 3.2.1.3 Strict damage-reduction KPIs in global logistics operations

- 3.2.1.4 Automation in warehouses demanding standardized protective formats

- 3.2.1.5 Growth in cross-border trade increasing transit risk exposure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in polymer and pulp raw material prices

- 3.2.2.2 Sustainability regulations restricting single-use plastic packaging formats

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of biodegradable foam and molded fiber solutions

- 3.2.3.2 Integration of smart packaging for shock and temperature monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Paper & paperboard

- 5.3 Plastic-based

- 5.4 Foam polymers

- 5.5 Other materials

Chapter 6 Market Estimates and Forecast, By Product Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Flexible films & wraps

- 6.3 Protective mailers & envelopes

- 6.4 Loose fill & void fill

- 6.5 Engineered protective solutions

- 6.6 Rigid containers & structural packaging

Chapter 7 Market Estimates and Forecast, By Function, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Cushioning & shock absorption

- 7.3 Void fill & stabilization

- 7.4 Surface protection

- 7.5 Barrier & environmental protection

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 E-commerce, retail & consumer goods

- 8.3 Electronics & electrical

- 8.4 Automotive

- 8.5 Healthcare & pharmaceuticals

- 8.6 Food & beverage

- 8.7 Industrial & manufacturing

- 8.8 Logistics & 3pl providers

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Sealed Air Corporation

- 10.1.2 DS Smith Plc

- 10.1.3 International Paper Company

- 10.1.4 Mondi Group

- 10.1.5 Berry Global Inc.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Pregis LLC

- 10.2.1.2 Sonoco Products Company

- 10.2.1.3 Intertape Polymer Group Inc.

- 10.2.1.4 ProAmpac Holdings Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Huhtamaki Oyj

- 10.2.2.2 Ranpak Holdings Corp.

- 10.2.3 Europe

- 10.2.3.1 Smurfit WestRock

- 10.2.3.2 Storopack Hans Reichenecker GmbH

- 10.2.3.3 Nefab Group

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Cascades Inc.