|

시장보고서

상품코드

2027590

건축용 판유리 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Architectural Flat Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

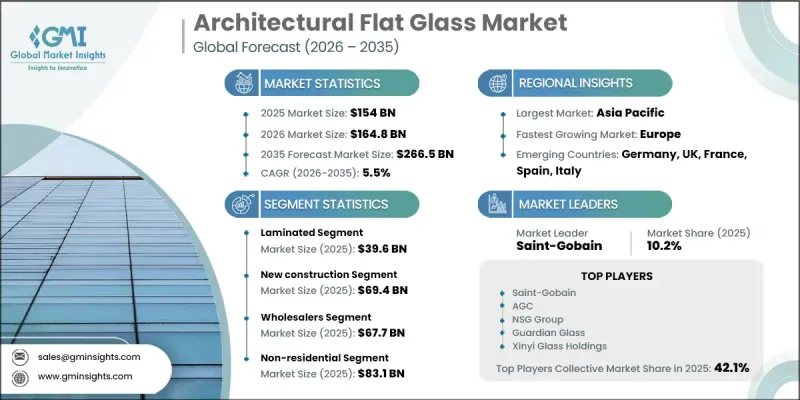

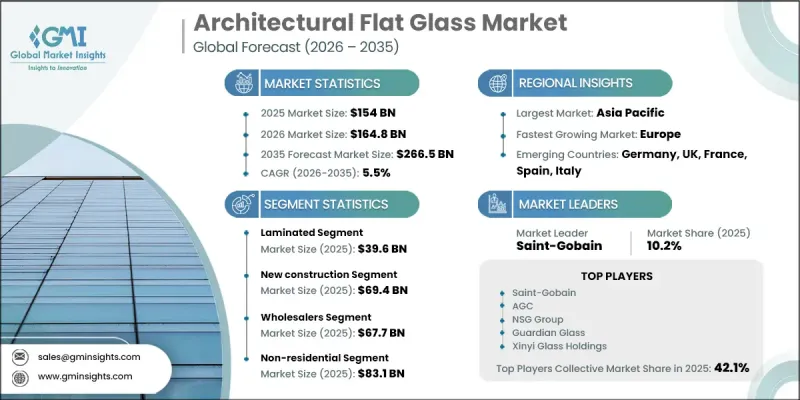

세계의 건축용 판유리 시장은 2025년에 1,540억 달러로 평가되었고 CAGR 5.5%를 나타내 2035년까지 2,665억 달러에 이를 것으로 추정되고 있습니다.

현대 건축에서 성능, 디자인, 에너지 효율의 균형을 갖춘 첨단 소재가 점점 더 많이 도입됨에 따라 이 시장은 계속 성장하고 있습니다. 균일한 시트 형태로 생산되는 건축용 판유리는 투명성, 구조적 적응성 및 시각적 매력을 향상시키는 능력으로 현대 건축에서 중요한 역할을 하고 있습니다. 그 보급은 자연광 최적화, 단열성 향상, 미적으로 세련된 건축 외피에 대한 수요 증가에 의해 주도되고 있습니다. 코팅 기술과 제조 공정의 발전으로 단열 성능, 일사량 조절, 차음성이 크게 향상되어 건축용 판유리는 진화하는 건축 디자인에서 선호되는 솔루션이 되었습니다. 이 소재는 주거용 및 상업용 인프라 모두에 널리 사용되고 있으며, 에너지 효율이 뛰어나고 지속 가능한 건물의 개발을 지원하고 있습니다. 또한, 도시화의 진전과 인프라 투자 확대가 수요를 더욱 촉진하는 한편, 유리 시스템의 지속적인 혁신과 설계 유연성은 건축용 판유리 시장의 경쟁 환경과 장기적인 성장 궤도를 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 1,540억 달러 |

| 예측액 | 2,665억 달러 |

| CAGR | 5.5% |

2025년에는 세계 인프라 개발이 증가함에 따라 신축 부문이 694억 달러를 차지했습니다. 건설업체들은 신축 구조물에서 내구성, 효율성 및 장기적인 운영 가치를 보장하는 고성능 소재를 우선시하고 있습니다. 건축용 판유리는 건물의 성능 향상과 거주자의 경험 향상에 기여함으로써 이러한 목표를 달성하는 데 핵심적인 역할을 하고 있습니다. 신규 개발뿐만 아니라, 부동산 소유주들이 에너지 효율을 높이고 기존 구조물을 현대화하기 위해 개보수 및 리노베이션 프로젝트도 수요를 견인하고 있습니다. 판유리의 다재다능함은 다양한 구조적 요소에 적용이 가능하여 건설 프로젝트에서 기능적 측면과 시각적 측면을 모두 향상시킬 수 있도록 지원합니다.

도매 부문은 2025년 677억 달러 시장 규모를 기록했습니다. 도매업체는 복잡한 건설 활동에 필요한 다양한 유리 사양을 항상 확보하여 대규모 유통을 촉진하고 있습니다. 재고 관리, 물류 및 적시 납품 능력은 계약자 및 가공업체가 프로젝트의 납기 및 품질 기준을 충족할 수 있도록 지원합니다. 이 유통 네트워크는 시장 접근성을 강화하고 제조업체와 최종 사용자 간의 효율적인 협업을 가능하게 함으로써 산업 전반의 성장을 지원하고 있습니다.

북미의 건축용 판유리 시장은 2025년 184억 달러로 평가되었으며 2035년까지 314억 달러에 달할 것으로 예측됩니다. 이 지역에서는 에너지 효율과 건물 성능을 향상시키는 첨단 유리 시스템에 대한 수요가 증가하고 있습니다. 혁신적인 파사드 디자인과 고성능 코팅 유리의 채택 확대가 지역 전체의 건설 트렌드를 형성하고 있습니다. 미국은 단열 개선, 채광 최적화, 현대적 디자인 통합에 중점을 둔 주택 리노베이션 및 상업용 개발 프로젝트가 지속적으로 진행되면서 지역 수요를 주도하고 있습니다. 지속 가능한 건축 방식과 규제 기준에 대한 인식이 높아지면서 기술적으로 진보된 판유리 솔루션의 채택이 더욱 가속화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별(2022-2035년)

제6장 시장 추산 및 예측 : 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 판매 채널별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

KTH 26.05.20The Global Architectural Flat Glass Market was valued at USD 154 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 266.5 billion by 2035.

The market continues to gain momentum as modern construction increasingly integrates advanced materials that balance performance, design, and energy efficiency. Architectural flat glass, manufactured in uniform sheet form, plays a critical role in contemporary buildings due to its ability to deliver transparency, structural adaptability, and enhanced visual appeal. Its widespread adoption is driven by the growing need for natural light optimization, improved insulation, and aesthetically refined building envelopes. Advancements in coating technologies and fabrication processes have significantly improved thermal performance, solar control, and acoustic insulation, making flat glass a preferred solution in evolving architectural designs. The material is extensively utilized across both residential and commercial infrastructure, supporting the development of energy-efficient and sustainable buildings. In addition, rising urbanization and infrastructure investments are further reinforcing demand, while continuous innovation in glazing systems and design flexibility continues to shape the competitive landscape and long-term growth trajectory of the architectural flat glass market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $154 Billion |

| Forecast Value | $266.5 Billion |

| CAGR | 5.5% |

The new construction segment accounted for USD 69.4 billion in 2025 owing to the increasing volume of global infrastructure development. Builders prioritize high-performance materials that ensure durability, efficiency, and long-term operational value in newly developed structures. Architectural flat glass plays a central role in achieving these objectives by contributing to improved building performance and enhanced occupant experience. Alongside new developments, renovation and upgrade projects are also contributing to demand as property owners seek to enhance energy efficiency and modernize existing structures. The versatility of flat glass enables its application across various structural elements, supporting both functional and visual enhancements in construction projects.

The wholesaler segment generated USD 67.7 billion in 2025. Wholesalers facilitate large-scale distribution by ensuring consistent availability of diverse glass specifications required for complex construction activities. Their ability to manage inventory, logistics, and timely delivery supports contractors and fabricators in meeting project deadlines and quality standards. This distribution network strengthens market accessibility and enables efficient coordination between manufacturers and end users, thereby supporting overall industry growth.

North America Architectural Flat Glass Market was valued at USD 18.4 billion in 2025 and is anticipated to reach USD 31.4 billion by 2035. The region is witnessing rising demand for advanced glazing systems that enhance energy efficiency and building performance. Increasing adoption of innovative facade designs and high-performance coated glass is shaping construction trends across the region. The United States continues to drive regional demand, supported by ongoing residential upgrades and commercial development projects that emphasize improved insulation, daylight optimization, and modern design integration. Growing awareness of sustainable construction practices and regulatory standards is further accelerating the adoption of technologically advanced flat glass solutions.

Key companies operating in the Global Architectural Flat Glass Industry include Saint-Gobain, AGC, Guardian Glass, NSG Group, Xinyi Glass Holdings, Asahi India Glass, Central Glass, China Glass Holdings, CSG Holding, and Cardinal Glass Industries. Companies in the Architectural Flat Glass Market are strengthening their competitive position through continuous investment in advanced manufacturing technologies and product innovation. Many players are focusing on developing energy-efficient and high-performance glass solutions that align with evolving building standards and sustainability requirements. Strategic collaborations with construction firms and real estate developers are enabling companies to expand their project pipelines and enhance market reach. In addition, businesses are optimizing supply chain operations and expanding production capacities to meet rising global demand. Geographic expansion into emerging markets and diversification of product portfolios are also key approaches. Furthermore, companies are prioritizing research in coatings, smart glass technologies, and recyclable materials to maintain long-term competitiveness and reinforce their market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Application

- 2.2.3 Sales Channel

- 2.2.4 End Use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for daylight-focused designs

- 3.2.1.2 Rising use in modern building facades

- 3.2.1.3 Expanding renovation activities using new glazing

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 High energy-loss without proper insulation

- 3.2.2.2 Breakage risk during transport and installation

- 3.2.3 Opportunities

- 3.2.3.1 Growing interest in smart glazing solutions

- 3.2.3.2 Adoption of energy-efficient building materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Laminated

- 5.3 Tempered

- 5.4 Basic Float

- 5.5 Insulating

- 5.6 Decorative

- 5.7 Reflective

- 5.8 Prism & low-emissivity glass

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 New construction

- 6.3 Refurbishment

- 6.4 Interior construction

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Wholesalers

- 7.3 Online

- 7.4 Retailer

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Non-Residential

- 8.3.1 Offices

- 8.3.2 Retail Spaces

- 8.3.3 Hospitality

- 8.3.3.1 Institutional

- 8.3.3.2 Healthcare facilities

- 8.3.3.3 Educational institutes

- 8.3.3.4 Transport facilities

- 8.3.3.5 Entertainment facilities

- 8.3.3.6 Others

- 8.4 Industrial

- 8.4.1 Manufacturing Facilities

- 8.4.2 Warehouses

- 8.4.3 Flex Space Buildings

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGC

- 10.2 Asahi India Glass

- 10.3 Cardinal Glass Industries

- 10.4 Central Glass

- 10.5 China Glass Holdings

- 10.6 CSG Holding

- 10.7 Saint-Gobain

- 10.8 Guardian Glass

- 10.9 NSG Group

- 10.10 Xinyi Glass Holdings