|

시장보고서

상품코드

2027596

농업용 미량영양소 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Agricultural Micronutrients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

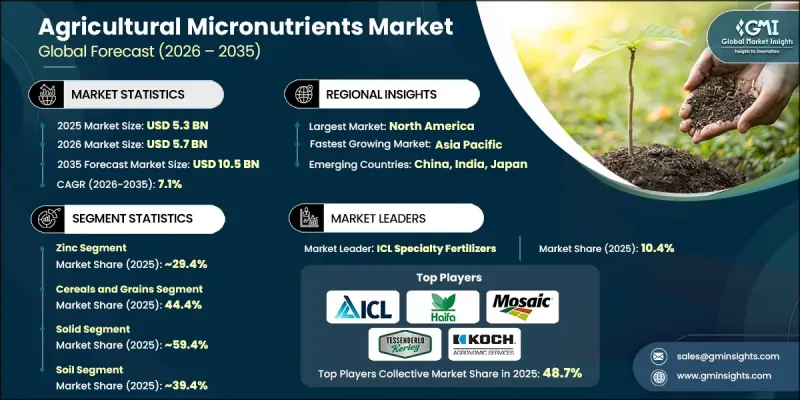

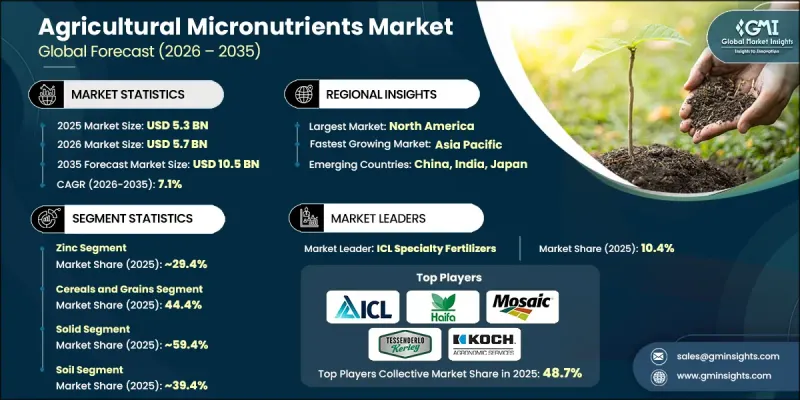

세계의 농업용 미량영양소 시장은 2025년에 53억 달러로 평가되었고 CAGR 7.1%를 나타내 2035년까지 105억 달러에 이를 것으로 추정되고 있습니다.

세계 농업에서 작물 생산성과 토양 건강 상태 개선에 대한 관심이 높아짐에 따라 이 시장은 확대되고 있습니다. 아연, 철, 망간, 붕소, 구리, 몰리브덴, 니켈 등의 농업용 미량영양소는 극미량이라도 식물의 성장에 매우 중요한 역할을 하며, 작물의 발육, 스트레스 저항성, 수확량에 큰 영향을 미칩니다. 토양의 영양 부족에 대한 농가의 인식이 높아지면서 미량영양소 비료의 보급을 촉진하고 있습니다. 신흥 경제국, 특히 광범위한 토양 황폐화에 직면한 지역에서는 이러한 재료의 채택이 빠르게 진행되고 있습니다. 생산자들이 환경 친화적인 방법으로 토양 비옥도를 높이기 위해 지속 가능한 유기 농업으로 전환하는 것도 수요를 더욱 증가시키고 있습니다. 생체 이용률이 향상된 킬레이트화 제품을 포함하여 영양소 배합 기술의 지속적인 발전으로 효율성과 작물 반응이 개선되고 있습니다. 이러한 미량영양소는 효소 활성화, 광합성, 영양소 흡수와 같은 중요한 생리적 기능을 지원하고, 가뭄이나 염해와 같은 환경적 스트레스에 대한 작물의 저항력을 높여 전반적인 농업 생산량과 품질 향상에 기여하고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 53억 달러 |

| 예측액 | 105억 달러 |

| CAGR | 7.1% |

곡물 부문은 2025년 44.4%의 점유율을 차지했으며, 2035년까지 연평균 6.7%의 성장률을 나타낼 것으로 예측됩니다. 그 우위는 주식 작물로서의 지위에 기인하며, 수확량 안정성과 작물의 내성을 향상시키기 위해서는 미량영양소 적용이 필수적입니다. 곡물 재배에 대한 채택 확대는 생산성을 높이고 세계 식량 안보의 목표를 뒷받침하고 있습니다.

고체 형태 부문은 2025년 59.4%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 6.8%의 성장률을 나타낼 것으로 전망됩니다. 액체 제제로의 전환이 진행되고 있음에도 불구하고, 고체 미량영양소는 저장 기간이 길고, 보관이 용이하며, 토양에 적용하기에 적합하기 때문에 여전히 널리 사용되고 있습니다. 그러나 액체 제제는 흡수 속도가 빠르고, 시비 관개 및 엽면 살포와 같은 현대식 영양 공급 시스템과 잘 어울리기 때문에 지지층이 확대되고 있습니다.

2025년 기준 북미의 농업용 미량영양소 시장은 전 세계 점유율의 34.9%를 차지했습니다. 이 지역의 성장은 선진적인 농업 방식과 정밀 농업 기술의 적극적인 도입으로 뒷받침되고 있습니다. 지속 가능한 영양 관리와 환경 효율성에 대한 관심이 높아지면서 수요가 더욱 증가하고 있습니다. 미국과 캐나다는 특히 고부가가치 작물 및 특용작물에서 킬레이트화 및 액체 미량영양소 솔루션의 도입을 주도하고 있으며, 유기농에 대한 관심이 높아지면서 친환경 농자재로의 전환을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 작물 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 형태별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

KTH 26.05.20The Global Agricultural Micronutrients Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 10.5 billion by 2035.

The market is witnessing expansion as global agriculture intensifies its focus on improving crop productivity and soil health. Agricultural micronutrients such as zinc, iron, manganese, boron, copper, molybdenum, and nickel play a crucial role in supporting plant growth in extremely small quantities, yet they significantly influence crop development, resistance to stress, and yield performance. Rising awareness among farmers regarding soil nutrient deficiencies is encouraging wider adoption of micronutrient-based fertilizers. Emerging economies, particularly in regions facing widespread soil depletion, are showing strong uptake of these inputs. The shift toward sustainable and organic farming practices is further boosting demand as growers aim to improve soil fertility using environmentally responsible methods. Continuous advancements in nutrient formulation technologies, including chelated products with enhanced bioavailability, are improving efficiency and crop response. These micronutrients also support essential physiological functions such as enzyme activation, photosynthesis, and nutrient absorption, helping improve crop resilience against environmental stressors like drought and salinity while enhancing overall agricultural output and quality.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 7.1% |

The cereals and grains segment accounted for 44.4% share in 2025 and is expected to grow at a CAGR of 6.7% through 2035. Their dominance is attributed to their status as staple food crops, where micronutrient application is essential to improve yield stability and crop resilience. Increasing adoption in grain cultivation is enhancing productivity and supporting food security objectives globally.

The solid form segment held a 59.4% share in 2025 and is projected to grow at a CAGR of 6.8% during 2026-2035. Despite the growing shift toward liquid formulations, solid micronutrients continue to be widely used due to their longer shelf life, ease of storage, and suitability for soil-based applications. However, liquid formulations are gaining traction due to faster absorption rates and compatibility with modern nutrient delivery systems such as fertigation and foliar application.

North America Agricultural Micronutrients Market accounted for 34.9% of the global share in 2025. Growth in the region is supported by advanced farming practices and strong adoption of precision agriculture technologies. Increasing focus on sustainable nutrient management and environmental efficiency is further driving demand. The United States and Canada are leading adopters of chelated and liquid micronutrient solutions, particularly for high-value and specialty crops, while growing interest in organic farming practices is reinforcing the shift toward eco-friendly agricultural inputs.

Key companies operating in the Global Agricultural Micronutrients Market include Haifa Group, The Mosaic Company, Koch Agronomic Services, ICL Specialty Fertilizers, Helena Agri-Enterprises, Tessenderlo Kerley, Brandt Consolidated, Miller Chemical, AgroLiquid, NACHURS Alpine Solutions, SAN Agrow, Agricen, Atlantica Agricola, Micromix Plant Health, and WUXAL. Companies in the Global Agricultural Micronutrients Market are strengthening their competitive position through innovation in formulation technologies and expansion of product portfolios. Significant investments are being directed toward developing chelated and highly bioavailable micronutrient solutions that improve crop efficiency and soil absorption. Strategic collaborations with distributors and agricultural service providers are enhancing market penetration. Firms are also focusing on expanding production capacities to meet rising global demand. Increasing emphasis on sustainable agriculture is driving companies to develop eco-friendly and organic-compatible products. Additionally, businesses are leveraging digital agriculture platforms and agronomic advisory services to improve farmer engagement and promote precision nutrient application practices, thereby enhancing long-term customer loyalty and market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Crop type

- 2.2.4 Form

- 2.2.5 Application

- 2.2.6 End user

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Zinc

- 5.3 Boron

- 5.4 Manganese

- 5.5 Iron

- 5.6 Molybdenum

- 5.7 Copper

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Crop Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cereals and grains

- 6.3 Oilseeds and pulses

- 6.4 Fruits and vegetables

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Solid

- 7.3 Liquid

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Soil

- 8.3 Foliar

- 8.4 Fertigation

Chapter 9 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Commercial farms/large-scale agriculture

- 9.3 Small & medium farms

- 9.4 Greenhouse & controlled environment agriculture

- 9.5 Turf & ornamentals

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Agricen

- 11.2 AgroLiquid

- 11.3 Atlantica Agricola

- 11.4 Brandt Consolidated

- 11.5 Haifa Group

- 11.6 Helena Agri-Enterprises

- 11.7 ICL Specialty Fertilizers

- 11.8 Koch Agronomic Services

- 11.9 Micromix Plant Health

- 11.10 Miller Chemical

- 11.11 NACHURS Alpine Solutions

- 11.12 SAN Agrow

- 11.13 Tessenderlo Kerley

- 11.14 The Mosaic Company

- 11.15 WUXAL