|

시장보고서

상품코드

2027605

범퍼 센서 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Bumper Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

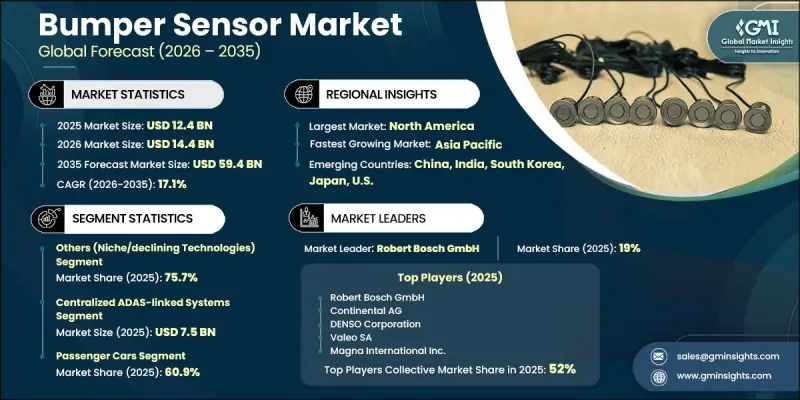

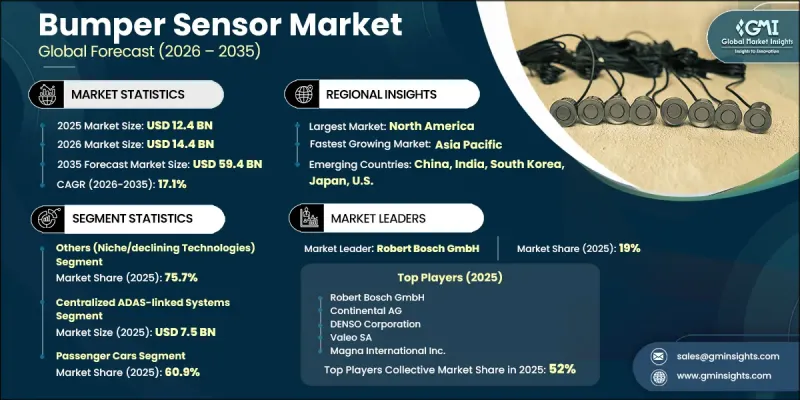

세계의 범퍼 센서 시장은 2025년에 124억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 17.1%를 나타내 594억 달러에 이를 것으로 추정되고 있습니다.

이 시장의 성장은 주요 경제권에서 자동차 안전 규제가 빠르게 강화되고, 현대 자동차에 커넥티드 및 무선 센싱 시스템이 통합되고 있는 것과 관련이 있습니다. 도심의 교통 체증 증가와 주차 공간 부족은 첨단 주차 보조 기술의 채택을 촉진하고 있으며, 이는 범퍼 센서 수요를 직접적으로 뒷받침하고 있습니다. 동시에 첨단 운전자 보조 시스템(ADAS)의 도입이 가속화되면서 충돌 방지 및 실시간 물체 감지 등 범퍼 기반 센싱의 역할이 강화되고 있습니다. 또한, 시장에서는 초음파, 레이더, 카메라 기반 입력을 결합하여 감지 정확도를 높이고 판단 오류를 줄이는 센서 융합으로의 구조적 변화도 나타나고 있습니다. 더 안전한 운전 경험을 원하는 소비자의 욕구가 높아지고, OEM의 자동화 차량 플랫폼에 대한 관심이 높아짐에 따라 제품 채택이 더욱 확대되고 있습니다. 승용차 생산 확대, OEM 및 애프터마켓 채널의 보급률 증가, 전자 제어 시스템의 지속적인 발전과 함께 세계 자동차 생태계 전체에서 이 산업은 강력한 장기 성장 궤도를 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 124억 달러 |

| 예측액 | 594억 달러 |

| CAGR | 17.1% |

중앙 집중식 ADAS 연계 시스템 부문은 2025년 75억 달러에 달했습니다. 이 시스템은 범퍼 센서, 레이더 유닛, 카메라 모듈의 입력을 통합하여 통합된 처리 아키텍처를 구축하여 협력적인 안전 대응을 가능하게 합니다. 이들은 충돌 방지, 긴급 제동 기능, 자동 주차 지원을 지원하기 위해 승용차 및 상용차에 널리 도입되고 있습니다. 전자제어장치(ECU)와의 통합을 통해 시스템의 신뢰성을 향상시키고, 진화하는 안전 표준을 준수할 수 있어 현대 자동차 플랫폼 전반에 걸쳐 지속적으로 확산되고 있습니다.

센서 융합(아키텍처 기반 통합) 부문은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 16.8%를 나타낼 것으로 예측됩니다. 이 부문의 성장은 여러 센싱 기술을 단일 의사결정 프레임워크에 통합한 통합 ADAS 에코시스템의 도입 확대에 의해 주도되고 있습니다. 이 접근 방식은 물체 감지 정확도를 높이고, 응답 시간을 단축하며, 차량의 반자동 운전 기능을 지원합니다. 또한, 오감지 신호를 줄이고 전체 시스템의 신뢰성을 향상시키는데 기여하고 있으며, 이를 통해 자동차 제조업체들은 미드레인지 및 프리미엄 차량 카테고리 모두에서 융합형 센서 아키텍처의 표준화를 추진하고 있습니다.

북미의 범퍼 센서 시장은 엄격한 차량 안전 규제와 첨단 자동차 기술을 통한 교통 사고 감소에 대한 강조에 힘입어 2025년 36.3%의 점유율을 차지했습니다. 미국의 규제 프레임워크는 첨단 운전자 보조 시스템(ADAS)에 대한 감독을 강화하는 방향으로 계속 진화하고 있으며, 차량에 대한 안전 모니터링 시스템의 광범위한 도입을 촉진하고 있습니다. 충돌 방지 및 지능형 모빌리티 솔루션에 초점을 맞춘 연구 프로그램에 대한 정부 기관 및 업계 관계자들의 지속적인 투자도 이 지역의 범퍼 센서 기술 채택을 촉진하고 있습니다.

범퍼 센서 업계에는 ZF Friedrichshafen AG, Robert Bosch GmbH, NXP Semiconductors, Sensata Technologies, Valeo SA, Analog Devices, Continental AG, Denso, 현대모비스, Aptive, Magna International, Murata Manufacturing, Hitachi Automotive Systems, Infineon Technologies, Leda Tech. 마그나 인터내셔널, 무라타제작소, 히타치 오토모티브 시스템즈, 인피니언 테크놀로지스, 레다테크 등이 있습니다. 범퍼 센서 시장에서 사업을 전개하는 기업들은 첨단 운전자 보조 시스템(ADAS) 통합 및 차세대 센서 융합 플랫폼에 대한 적극적인 투자를 통해 자사의 입지를 강화하는 데 주력하고 있습니다. 각 업체들은 제품 포트폴리오에 고도로 통합된 초음파, 레이더 및 카메라 기반 감지 솔루션을 추가하여 감지 정확도를 높이고 시스템 복잡성을 줄이며, 제품 포트폴리오에 추가하고 있습니다. 향후 차량 플랫폼에 조기 설계 통합을 보장하기 위해 자동차 OEM과의 전략적 제휴를 우선시하고 있습니다. 또한, 각 업체들은 소프트웨어 기반 센싱 인텔리전스에 투자하여 실시간 데이터 처리 및 예측 안전 기능을 구현하고 있습니다. 반도체의 발전과 소형화된 센서 설계를 통한 비용 최적화도 중요한 중점 분야로, 제조업체가 효율적으로 생산 규모를 확대할 수 있도록 돕고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기술별(2022-2035년)

제6장 시장 추산 및 예측 : 시스템 아키텍처별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 차종별(2022-2035년)

제9장 시장 추산 및 예측 : 판매 채널별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

KTHThe Global Bumper Sensor Market was valued at USD 12.4 billion in 2025, and it is estimated to grow at a CAGR of 17.1% to reach USD 59.4 billion by 2035.

The market growth is linked to the rapid strengthening of vehicle safety regulations across major economies, alongside the rising integration of connected and wireless sensing systems in modern vehicles. Increasing urban congestion and limited parking space availability are also pushing the adoption of advanced parking assistance technologies, which directly support bumper sensor demand. At the same time, the accelerated deployment of Advanced Driver Assistance Systems (ADAS) is reinforcing the role of bumper-based sensing in collision prevention and real-time object detection. The market is also witnessing a structural shift toward sensor fusion, where ultrasonic, radar, and camera-based inputs are combined to improve detection accuracy and reduce errors in judgment. Growing consumer preference for safer driving experiences, combined with OEM focus on automation-ready vehicle platforms, is further strengthening product adoption. Expanding passenger vehicle production, increasing penetration in both OEM and aftermarket channels, and continuous advancements in electronic control systems are collectively shaping a strong long-term growth trajectory for the industry across global automotive ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.4 Billion |

| Forecast Value | $59.4 Billion |

| CAGR | 17.1% |

The centralized ADAS-linked systems segment reached USD 7.5 billion in 2025. These systems consolidate inputs from bumper sensors, radar units, and camera modules into a unified processing architecture that enables coordinated safety responses. They are widely implemented across passenger and commercial vehicles to support collision avoidance, emergency braking functions, and automated parking assistance. Their integration into electronic control units improves system reliability and ensures compliance with evolving safety standards, which continues to drive their widespread adoption across modern automotive platforms.

The sensor fusion (architecture-driven integration) segment is projected to grow at a CAGR of 16.8% during 2026-2035. Growth in this segment is driven by increasing deployment of integrated ADAS ecosystems that combine multiple sensing technologies into a single decision-making framework. This approach enhances object detection accuracy, strengthens response time, and supports semi-automated driving capabilities in vehicles. It also helps reduce false detection signals and improves overall system reliability, which is encouraging automotive manufacturers to standardize fused sensor architectures across both mid-range and premium vehicle categories.

North America Bumper Sensor Market accounted for 36.3% share in 2025, supported by strict vehicle safety enforcement and a strong emphasis on reducing road accidents through advanced automotive technologies. Regulatory frameworks in the United States continue to evolve toward enhanced oversight of driver assistance technologies, encouraging wider deployment of safety monitoring systems in vehicles. Continuous investment from government bodies and industry participants in research programs focused on crash prevention and intelligent mobility solutions is also strengthening the regional adoption of bumper sensor technologies.

The Bumper Sensor Industry includes several key players such as ZF Friedrichshafen AG, Robert Bosch GmbH, NXP Semiconductors, Sensata Technologies, Valeo SA, Analog Devices, Inc., Continental AG, DENSO Corporation, Hyundai Mobis, Aptiv PLC, Magna International Inc., Murata Manufacturing Co., Ltd., Hitachi Automotive Systems, Infineon Technologies AG, and LeddarTech Inc. Companies operating in the Bumper Sensor Market are focusing on strengthening their position through aggressive investment in ADAS integration and next-generation sensor fusion platforms. They are expanding product portfolios to include highly integrated ultrasonic, radar, and camera-based sensing solutions that improve detection accuracy and reduce system complexity. Strategic partnerships with automotive OEMs are being prioritized to secure early design integration in upcoming vehicle platforms. Firms are also investing in software-driven sensing intelligence, enabling real-time data processing and predictive safety functions. Cost optimization through semiconductor advancements and miniaturized sensor designs is another key focus area, helping manufacturers scale production efficiently.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 System architecture trends

- 2.2.3 Application trends

- 2.2.4 Vehicle type trends

- 2.2.5 Sales channel trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global NCAP safety compliance requirements

- 3.2.1.2 Increasing ADAS penetration in mid-range vehicles

- 3.2.1.3 Growing urban parking constraints boosting sensor adoption

- 3.2.1.4 OEM integration of ultrasonic sensors as standard features

- 3.2.1.5 Expansion of autonomous driving feature pipelines

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Sensor performance degradation in extreme weather conditions

- 3.2.2.2 Integration complexity with multi-sensor ADAS architectures

- 3.2.3 Market opportunities

- 3.2.3.1 Transition toward software-defined vehicle sensor ecosystems

- 3.2.3.2 Increasing aftermarket retrofitting demand in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Ultrasonic sensors

- 5.3 Radar sensors (short-range)

- 5.4 Sensor fusion (architecture-driven integration)

- 5.5 Others (niche/declining technologies)

Chapter 6 Market Estimates and Forecast, By System Architecture, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Standalone sensors

- 6.3 Integrated bumper sensor systems

- 6.4 Centralized ADAS-linked systems

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Parking assistance systems (PAS)

- 7.3 Blind spot detection (BSD)

- 7.4 Rear cross traffic alert (RCTA)

- 7.5 Low-speed collision avoidance

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.3 Commercial vehicles

Chapter 9 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 OEM (original equipment manufacturer)

- 9.3 Aftermarket

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Robert Bosch GmbH

- 11.1.2 Continental AG

- 11.1.3 DENSO Corporation

- 11.1.4 Valeo SA

- 11.1.5 Magna International Inc.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Aptiv PLC

- 11.2.1.2 LeddarTech Inc.

- 11.2.1.3 Sensata Technologies

- 11.2.2 Asia Pacific

- 11.2.2.1 Hyundai Mobis

- 11.2.2.2 Hitachi Automotive Systems

- 11.2.2.3 Murata Manufacturing Co., Ltd.

- 11.2.2.4 NXP Semiconductors

- 11.2.3 Europe

- 11.2.3.1 ZF Friedrichshafen AG

- 11.2.3.2 Infineon Technologies AG

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Analog Devices, Inc.