|

시장보고서

상품코드

2027615

나노클레이 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Nanoclays Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

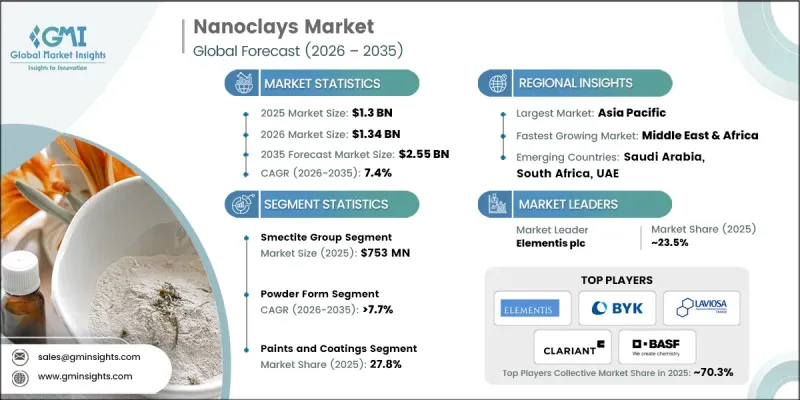

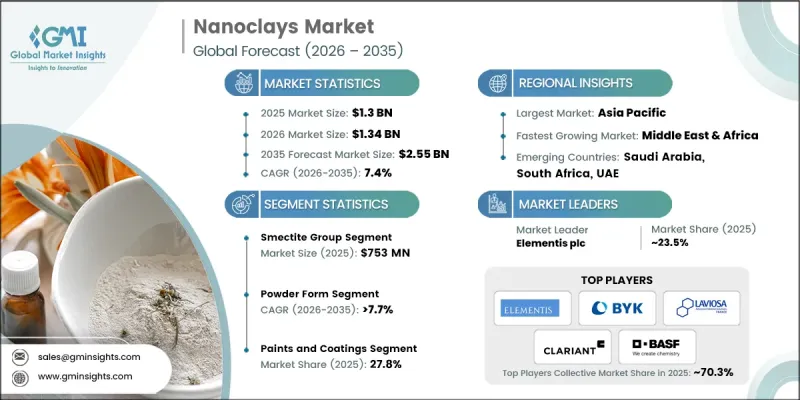

세계의 나노클레이 시장은 2025년에 13억 달러로 평가되었고 CAGR 7.4%를 나타내 2035년까지 25억 5,000만 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 폴리머 제품, 포장 솔루션, 자동차 부품, 건축자재 및 산업용 코팅에서 우수한 성능의 재료에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다. 나노클레이는 저농도에서도 기계적 강도, 열 안정성, 난연성 및 장벽 성능을 향상시키기 때문에 제조업체에서 점점 더 많이 채택하고 있습니다. 고분자 나노복합체 및 경량 소재의 배합은 비용 효율성과 기존 가공법과의 호환성으로 인해 여전히 인기를 얻고 있습니다. 나노클레이는 포장재의 가스 및 수분 차단성을 향상시켜 구조적 강도를 손상시키지 않으면서 자동차 경량화를 실현하고, 건축자재의 내구성과 수명을 연장시킵니다. 새롭게 등장한 고순도 및 개질 등급은 의료, 전자, 특수 코팅 분야에서 주목을 받고 있으며, 확장성, 성능 중심의 선택, 고도의 배합 기술이 시장의 꾸준한 확장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 13억 달러 |

| 예측액 | 25억 5,000만 달러 |

| CAGR | 7.4% |

스멕타이트 그룹 시장 규모는 2025년 7억 5,300만 달러로 평가되었고, 2026년부터 2035년까지 연평균 7.5% 성장할 것으로 예측됩니다. 그 인기는 높은 범용성, 폴리머와의 우수한 호환성, 그리고 우수한 차단성과 기계적 특성의 향상에 기인합니다. 카올리나이트 계열의 나노클레이는 특히 건설 및 코팅 분야에서 비용과 열 안정성이 요구되는 용도에 안정적인 수요를 유지하고 있습니다. 할로아이사이트는 독특한 관형 구조와 기능적 적응성으로 인해 특수 용도 및 첨단 용도에 대한 사용이 증가하고 있습니다. 세피오라이트, 파리고스키트 등 틈새 나노클레이는 유변학적 개질이나 특수 복합재료에 사용되어 대량생산보다는 시장의 다양성에 기여하고 있습니다.

페인트 및 코팅 분야는 2025년 3억 3,700만 달러 시장 규모로 27.8%의 점유율을 차지했으며 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.4%를 나타낼 것으로 예측됩니다. 나노 클레이는 내구성, 장벽성 향상 및 유변학 제어를 위해 이 분야에서 널리 채택되고 있습니다. 포장 및 자동차 산업에서는 재료의 성능 향상 및 경량화를 위해 활용되고 있으며, 수처리, 식품, 음료 분야에서는 흡착성 및 안정화 특성이 활용되고 있습니다. 바이오메디컬 분야가 혁신을 주도하는 한편, 다른 틈새 분야가 점진적인 성장을 가져와 시장 다변화를 촉진하고 있습니다.

북미의 나노클레이 시장은 2025년 2억 5,600만 달러 규모에 달했습니다. 이는 첨단 소재의 연구개발, 가볍고 내구성이 뛰어난 제품에 대한 수요, 그리고 자동차, 포장, 코팅 분야에서의 고분자 나노복합재 채택이 주도한 것입니다. 캐나다는 장수명 건축자재와 친환경 산업용 코팅에 집중하여 시장에 기여하고 있으며, 지역 시장의 성장을 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 형태별(2022-2035년)

제7장 시장 추산 및 예측 : 용도별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTH 26.05.20The Global Nanoclays Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 2.55 billion by 2035.

The growth is fueled by rising demand for materials with superior performance in polymer products, packaging solutions, automotive components, construction materials, and industrial coatings. Manufacturers are increasingly relying on nanoclays because they enhance mechanical strength, thermal stability, flame resistance, and barrier performance even at low concentrations. Polymer nanocomposites and lightweight material formulations remain popular due to cost efficiency and compatibility with traditional processing methods. Nanoclays provide packaging with improved gas and moisture barriers, enable lightweight automotive designs without compromising structural strength, and enhance the durability and lifespan of construction materials. Emerging high-purity and modified grades are gaining traction in healthcare, electronics, and specialty coatings, while scalability, performance-oriented selection, and advanced formulations are supporting steady market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.55 Billion |

| CAGR | 7.4% |

The smectite group segment was valued at USD 753 million in 2025 and is expected to grow at a CAGR of 7.5% from 2026 to 2035. Its popularity stems from versatility, strong polymer compatibility, and superior barrier and mechanical enhancements. Kaolinite group nanoclays maintain steady demand for cost-sensitive and thermally stable applications, especially in construction and coatings. Halloysite is increasingly used in specialty and advanced applications due to its unique tubular structure and functional adaptability. Niche nanoclays such as sepiolite and palygorskite are used for rheology modification and specialty composites, contributing to market variety rather than bulk volume.

The paints and coatings segment was valued at USD 337 million in 2025, holding a 27.8% share, and is expected to grow at a CAGR of 7.4% during 2026-2035. Nanoclays are widely adopted in this sector for durability, barrier improvement, and rheological control. Packaging and automotive industries utilize them for material enhancement and lightweighting, while water treatment, food, and beverage sectors rely on adsorption and stabilization properties. Biomedical applications drive innovation, whereas other niche uses contribute incremental growth, promoting overall market diversification.

North America Nanoclays Market accounted for USD 256 million in 2025, driven by advanced material R&D, demand for lightweight yet durable products, and adoption of polymer nanocomposites in automotive, packaging, and coatings. Canada contributes through its focus on long-lasting construction materials and environmentally sustainable industrial coatings, strengthening regional market development.

Key players operating in the Nanoclays Market include Elementis plc, BYK-Chemie (ALTANA), Laviosa Chimica Mineraria, Tolsa Group, BASF SE, Evonik Industries, Clariant AG, Mineral Technologies, FCC Inc., Nanografi, Nanoshel, and others. Companies in the Nanoclays Market strengthen their position through multiple strategies. They focus on expanding R&D capabilities to develop high-performance and application-specific nanoclays. Strategic partnerships, mergers, and acquisitions help increase global reach and product portfolio diversity. Investment in production capacity and adoption of advanced processing technologies ensure a scalable and cost-efficient supply. Firms prioritize developing modified and high-purity grades to address niche markets such as healthcare, electronics, and specialty coatings. Market leaders also enhance their presence through sustainable manufacturing practices, regulatory compliance, and technical support services for end-users, which build long-term customer trust and loyalty.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Smectite Group

- 5.3 Kaolinite Group

- 5.4 Halloysite

- 5.5 Others (sepiolite, palygorskite)

Chapter 6 Market Estimates and Forecast, By Form, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Powder Form

- 6.3 Masterbatch/Pre-dispersed

- 6.4 Gel/Suspension

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Water Treatment

- 7.3 Food and Beverage Packaging

- 7.4 Automotive

- 7.5 Biomedical

- 7.6 Paints and Coatings

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Elementis plc

- 9.2 BYK-Chemie (ALTANA)

- 9.3 Laviosa Chimica Mineraria

- 9.4 Tolsa Group

- 9.5 BASF SE

- 9.6 Evonik Industries

- 9.7 Clariant AG

- 9.8 Mineral Technologies

- 9.9 FCC Inc.

- 9.10 Nanografi

- 9.11 Nanoshel