|

시장보고서

상품코드

2027633

선박용 오토파일럿 시스템 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Marine Autopilot System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

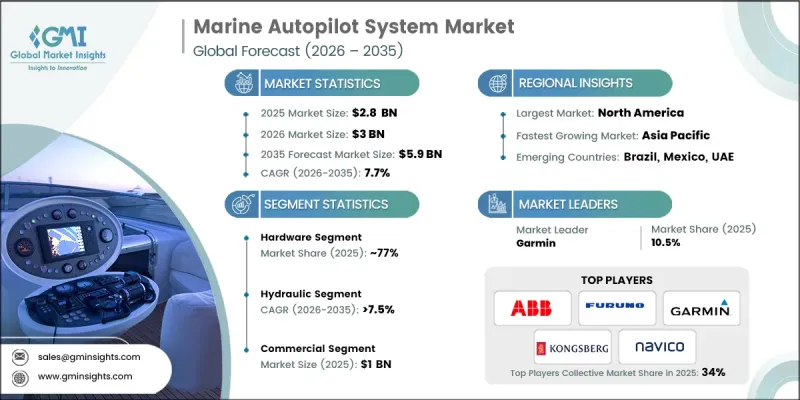

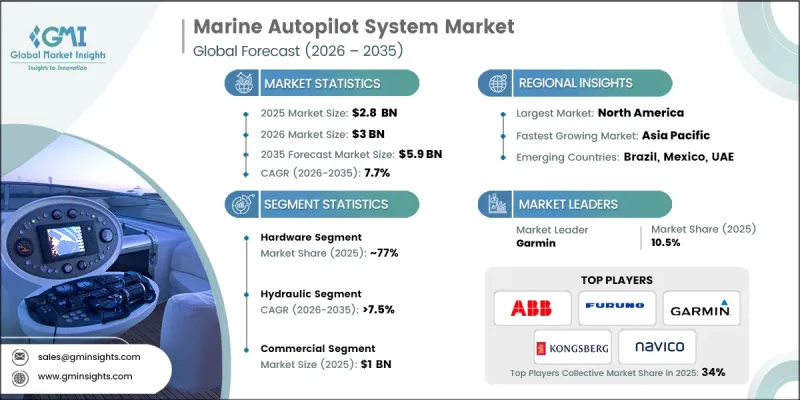

세계의 선박용 오토파일럿 시스템 시장은 2025년에 28억 달러로 평가되었고 CAGR 7.7%를 나타내 2035년까지 59억 달러에 이를 것으로 추정되고 있습니다.

이러한 확대는 첨단 항법 기술의 채택 확대, 멀티센서 오토파일럿의 통합, 상업용, 해군 및 레저용 선박의 실시간 선박 모니터링 및 연결성에 대한 수요 증가에 힘입어 이루어졌습니다. 조선사, 해양 사업자 및 해양 기술 제공업체들은 정밀한 항로 제어, 충돌 방지 및 자율 및 커넥티드 선박과의 원활한 통합을 가능하게 하는 첨단 자동 조종 솔루션에 대한 투자를 확대되고 있습니다. 선박 운영자는 실시간 의사결정을 지원하면서 효율성을 높이고, 승무원의 업무 부담을 줄이며, 항해의 정확성을 보장해야 한다는 압박을 받고 있습니다. 최신 오토파일럿 플랫폼은 중앙 집중식 항해 제어, AI를 활용한 항로 최적화, 원격 선박 모니터링, 지속적인 소프트웨어 업데이트를 제공하여 기존 시스템을 지능적이고 적응력이 높은 솔루션으로 전환하고 있습니다. 센서 통합 제어 장치, AI 기반 항법 알고리즘, 동적 포지셔닝 시스템, 소프트웨어에 의한 항로 최적화 등의 기술 발전은 선박용 오토파일럿 시스템의 운영을 재정의하고, 신뢰성을 향상시키며, 인적 오류를 최소화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 28억 달러 |

| 예측액 | 59억 달러 |

| CAGR | 7.7% |

하드웨어 부문은 2025년 77%의 점유율을 차지했으며, 2035년까지 연평균 7.9%의 성장률을 나타낼 것으로 전망됩니다. 하드웨어는 여전히 선박용 오토파일럿 시스템의 근간을 이루고 있으며, 정확한 항로 유지, 자율항해, 충돌회피를 지원하는 제어장치, 액추에이터, 센서, 조타기 제어장치 등 필수 구성요소를 제공합니다. 이러한 구성 요소는 상선, 조사선, 해군 함대 및 해양 에너지 사업에서 매우 중요하며, 전 세계 선단의 실시간 항해 및 원활한 소프트웨어 통합을 위한 물리적 기반을 형성합니다. 통합 브리지 시스템 및 자동 항법 솔루션에 하드웨어를 광범위하게 도입함으로써 시장 성장에 있어 핵심적인 역할을 더욱 공고히 하고 있습니다.

유압 부문은 65%의 점유율을 차지하고 있으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.5%를 나타낼 것으로 예측됩니다. 유압식 조타 시스템은 높은 토크 성능, 정밀한 코스 제어, 가혹한 해양 환경에서의 안정적인 작동으로 대형 상선, 군함 및 해양 지원 선박에서 선호되고 있습니다. 통합 오토파일럿 솔루션, 충돌방지 시스템, 실시간 항법 등에 대한 수요가 증가함에 따라 센서, 액추에이터, 조타기 제어장치와 호환되는 소프트웨어 지원 모듈식 유압 플랫폼의 채택이 가속화되고 있습니다. 표준화된 유압식 오토파일럿 시스템은 확장 가능한 솔루션을 제공하고 일관된 성능을 지원하며 유럽, 북미 및 아시아태평양에서 시장에서의 선도적 입지를 강화하고 있습니다.

미국의 선박용 오토파일럿 시스템 시장은 82%의 점유율을 차지며, 2025년에는 7억 7,180만 달러 규모에 도달했습니다. 미국 시장은 활발한 상선 운송 활동, 선진적인 해군 함대 인프라, 그리고 확립된 해양 에너지 부문이 주도하고 있습니다. 자율운항선박 프로그램, 통합 브리지 시스템, 다기능 자동조종 솔루션에 대한 투자가 고성능 유압 및 전기 조타 시스템, AI 지원 항법 모듈, 복합형 트랜스듀서에 대한 수요를 견인하고 있습니다. 상선, 해군 함정, 연구용 선박 등 조사 및 방위 활동의 확대는 첨단 선박용 오토파일럿 솔루션의 채택을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 구성 요소별(2022-2035년)

제6장 시장 추산 및 예측 : 시스템별(2022-2035년)

제7장 시장 추산 및 예측 : 기술별(2022-2035년)

제8장 시장 추산 및 예측 : 선박별(2022-2035년)

제9장 시장 추산 및 예측 : 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

KTH 26.05.20The Global Marine Autopilot System Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 5.9 billion by 2035.

The expansion is fueled by rising adoption of advanced navigation technologies, multi-sensor autopilot integration, and the growing demand for real-time vessel monitoring and connectivity across commercial, naval, and recreational fleets. Shipbuilders, offshore operators, and marine technology providers are increasingly investing in sophisticated autopilot solutions that enable precise route control, collision avoidance, and seamless integration with autonomous and connected vessels. Operators are under growing pressure to enhance efficiency, reduce crew workload, and ensure navigational accuracy while supporting real-time decision-making. Modern autopilot platforms provide centralized navigation, AI-assisted course optimization, remote vessel monitoring, and continuous software updates, transforming traditional systems into intelligent, adaptive solutions. Technological advancements such as sensor-integrated control units, AI-driven navigation algorithms, dynamic positioning systems, and software-enabled route optimization are redefining marine autopilot operations, improving reliability and minimizing human error.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 7.7% |

The hardware segment accounted for 77% share in 2025 and is projected to grow at a CAGR of 7.9% through 2035. Hardware remains the backbone of marine autopilot systems, providing essential components such as control units, actuators, sensors, and rudder controllers that support precise course maintenance, autonomous navigation, and collision avoidance. These components are critical for commercial shipping, research vessels, naval fleets, and offshore energy operations, forming the physical foundation for real-time navigation and seamless software integration across global fleets. The widespread deployment of hardware in integrated bridge systems and automated navigation solutions reinforces its centrality to the market's growth.

The hydraulic segment held 65% share and is expected to grow at a CAGR of 7.5% between 2026 and 2035. Hydraulic steering systems are preferred for large commercial vessels, naval ships, and offshore support vessels due to their high torque capabilities, precise course control, and reliable operation in harsh marine conditions. The increasing demand for integrated autopilot solutions, collision avoidance, and real-time navigation has accelerated the adoption of software-enabled, modular hydraulic platforms compatible with sensors, actuators, and rudder controllers. Standardized hydraulic autopilot systems offer scalable solutions, supporting consistent performance and reinforcing market leadership across Europe, North America, and Asia Pacific.

United States Marine Autopilot System Market held an 82% share, generating USD 771.8 million in 2025. The U.S. market is driven by extensive commercial shipping activity, advanced naval fleet infrastructure, and a well-established offshore energy sector. Investments in autonomous vessel programs, integrated bridge systems, and multi-functional autopilot solutions are driving demand for high-performance hydraulic and electric steering systems, AI-assisted navigation modules, and combination transducers. The growth of research and defense operations further reinforces the adoption of sophisticated marine autopilot solutions across commercial, naval, and research vessels.

Key companies in the Global Marine Autopilot System Industry include Kongsberg Maritime, Garmin, Furuno Electric, Raymarine, ABB, Navico, Teledyne Technologies, JRC / Alphatron Marine, Airmar Technology, and Tokyo Keiki. Companies in the Marine Autopilot System Market are enhancing their foothold through a combination of technological innovation, strategic collaborations, and global expansion initiatives. Many players are investing in AI-driven navigation, sensor integration, and software-enabled autopilot platforms to improve reliability and efficiency. Partnerships with shipbuilders, naval contractors, and offshore operators allow access to high-value projects and specialized vessels. Firms are expanding into emerging markets while optimizing supply chains to reduce installation and maintenance costs. They are also focusing on enhancing customer support, training programs, and remote monitoring services to build brand loyalty. Standardization, modularity, and scalable solutions are being prioritized to strengthen market position and capture long-term growth opportunities across commercial, defense, and recreational maritime sectors.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 System

- 2.2.4 Technology

- 2.2.5 Vessel

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of advanced navigation systems

- 3.2.1.2 Rising demand for real-time marine data

- 3.2.1.3 Growth in commercial and naval fleet operations

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and installation cost

- 3.2.2.2 Compatibility and regulatory constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Autonomous and connected vessel platforms

- 3.2.3.2 Emerging markets and recreational vessels

- 3.2.3.3 Integration with AI and IoT Platforms

- 3.2.3.4 Retrofit and upgrade opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: USCG, EPA, NMEA Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS Regulation

- 3.4.2 Europe

- 3.4.2.1 Germany: BSH, CE Compliance

- 3.4.2.2 France: Ministry of Transport, Naval Safety Regulations

- 3.4.2.3 UK: MCA, CE & UKCA Standards

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, Maritime Safety

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Regulations

- 3.4.3.3 South Korea: MOLIT, KS Standards

- 3.4.3.4 India: MoRTH, BIS Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazil: ANTAQ, DENATRAN & CONAMA Standards

- 3.4.4.2 Mexico: SCT, Mexican Maritime Safety Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Company Tier Benchmarking

- 4.7.1 Tier Classification Criteria & Qualifying Thresholds

- 4.7.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Control units

- 5.2.2 Actuators

- 5.2.3 Sensor

- 5.2.4 Rudder controllers

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Navigation

- 5.3.2 Path planning

- 5.3.3 Collision avoidance

- 5.3.4 Remote monitoring and control

Chapter 6 Market Estimates & Forecast, By System, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Hydraulic

- 6.3 Electric

- 6.4 Mechanical

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Integrated autopilot

- 7.3 Standalone autopilot

Chapter 8 Market Estimates & Forecast, By Vessel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Recreational Vessels

- 8.4 Naval & Defense Vessels

- 8.5 Fishing Vessels

- 8.6 Passenger Vessels

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Course maintenance

- 9.3 Navigation assistance

- 9.4 Collision avoidance

- 9.5 Autonomous operations

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 ABB

- 11.1.2 Airmar Technology

- 11.1.3 Furuno Electric

- 11.1.4 Garmin

- 11.1.5 JRC / Alphatron Marine

- 11.1.6 Kongsberg Maritime

- 11.1.7 Navico

- 11.1.8 Raymarine

- 11.1.9 Teledyne Technologies

- 11.1.10 Tokyo Keiki

- 11.2 Regional Player

- 11.2.1 Northrop grumman sperry marine

- 11.2.2 Sperry marine

- 11.2.3 Wartsila

- 11.2.4 Comnav marine

- 11.2.5 Autonav marine systems

- 11.2.6 Humminbird

- 11.2.7 SI-TEX Marine Electronics

- 11.2.8 NKE marine electronics

- 11.2.9 Navis engineering

- 11.2.10 Raytheon Anschutz