|

시장보고서

상품코드

2027646

항공기 점화 시스템 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Aircraft Ignition System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

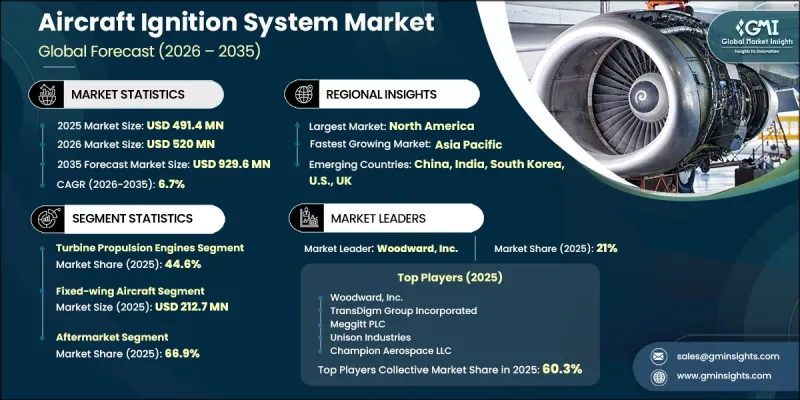

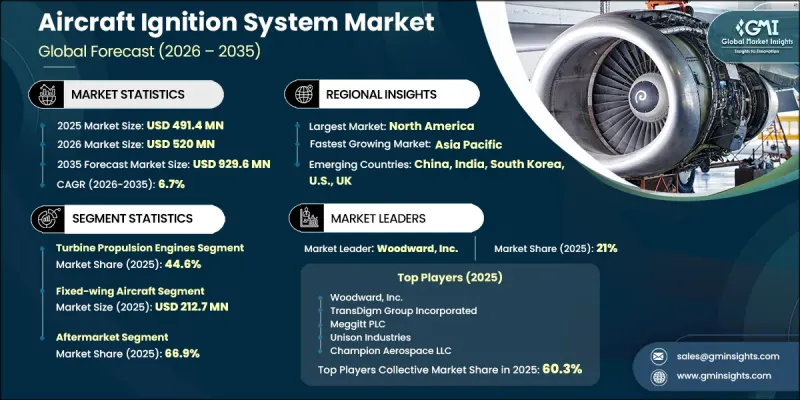

세계의 항공기 점화 시스템 시장은 2025년에 4억 9,140만 달러로 평가되었고 CAGR 6.7%를 나타내 2035년까지 9억 2,960만 달러에 이를 것으로 추정되고 있습니다.

항공업계의 이해관계자들이 엔진의 효율성, 운영 신뢰성 및 장기적인 성능 향상에 초점을 맞추면서 이 시장은 꾸준히 성장하고 있습니다. 협폭동체 항공기의 생산 증가와 항공기 가동률 상승이 결합되어 고급 점화 솔루션에 대한 안정적인 수요가 창출되고 있습니다. 항공사와 운항 사업자는 항공기 업그레이드에 우선순위를 두고 있으며, 그 결과 기존 점화 기술은 점차 더 효율적인 전자 시스템으로 대체되고 있습니다. 점화 시스템과 디지털 엔진 제어 아키텍처의 통합으로 시스템의 정확성과 응답성이 더욱 향상되었습니다. 또한, 전기화 된 항공기로의 전환은 기계적 복잡성을 줄이고 에너지 효율적인 운항을 지원하는 점화 시스템의 채택을 촉진하고 있습니다. 지속적인 유지보수 주기 및 부품 교체도 애프터마켓 수요의 지속에 기여하고 있습니다. 점화 설계의 기술 발전은 내구성 향상, 시스템 중량 감소, 연료 최적화 향상으로 이어져 항공기 점화 시스템 시장의 장기적인 전망을 더욱 견고하게 만들고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 4억 9,140만 달러 |

| 예측액 | 9억 2,960만 달러 |

| CAGR | 6.7% |

터빈 추진 엔진 부문은 2025년 44.6%의 점유율을 차지했으며, 고성능 점화 시스템을 필요로 하는 항공 플랫폼에 널리 도입되어 선도적 지위를 유지했습니다. 이 시스템은 가혹한 조건에서도 작동하도록 설계되어 일관되고 신뢰할 수 있는 엔진 점화를 보장합니다. 이 부문은 견고하고 내구성이 뛰어난 점화 부품에 대한 수요를 견인하는 지속적인 항공기 생산 및 운영 주기 증가로 인해 지속적인 수혜를 받고 있습니다. 높은 안전 기준과 엄격한 성능 요구 사항도 이 부문에서의 지속적인 채택을 더욱 촉진하고 있습니다.

고정익 항공기 부문은 전 세계 항공기 fleet에 널리 보급된 것을 배경으로 2025년 2억 1,270만 달러 시장 규모를 기록했습니다. 이 부문은 높은 항공기 생산량, 지속적인 납품, 그리고 신뢰할 수 있는 점화 시스템을 필요로 하는 빈번하고 장시간의 운항으로 인한 혜택을 누리고 있습니다. 일관된 엔진 성능에 대한 요구, 엄격한 항공 규정 준수, 진화하는 엔진 기술과의 호환성에 대한 수요는 이러한 수요를 더욱 촉진하고 있습니다. 이 부문은 운항 규모와 지속적인 기술 업그레이드로 인해 시장 성장의 중심적인 역할을 하고 있습니다.

북미의 항공기 점화 시스템 시장은 2025년 36.3%의 점유율을 차지했으며, 이는 규제 발전과 기술 도입에 힘입어 이 지역의 견조한 수요를 반영했습니다. 이 지역 시장은 엔진 효율, 배기가스 저감 및 유지보수 최적화에 대한 관심이 높아짐에 따라 시장이 확대되고 있습니다. 항공사들은 성능 향상, 마모 감소, 연료 효율성 향상을 위해 첨단 점화 시스템으로 전환하고 있습니다. 항공 인프라 및 현대화 프로그램에 대한 지속적인 투자는 이 지역 시장 성장을 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 시스템 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 구성 요소별(2022-2035년)

제7장 시장 추산 및 예측 : 엔진 유형별(2022-2035년)

제8장 시장 추산 및 예측 : 플랫폼별(2022-2035년)

제9장 시장 추산 및 예측 : 기술 성숙도별(2022-2035년)

제10장 시장 추산 및 예측 : 용도별(2022-2035년)

제11장 시장 추산 및 예측 : 지역별(2022-2035년)

제12장 기업 개요

KTH 26.05.20The Global Aircraft Ignition System Market was valued at USD 491.4 million in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 929.6 million by 2035.

The market is witnessing steady expansion as aviation stakeholders focus on improving engine efficiency, operational reliability, and long-term performance. Increasing production of narrow-body aircraft, combined with rising aircraft utilization rates, is creating consistent demand for advanced ignition solutions. Airlines and operators are prioritizing fleet upgrades, leading to the gradual replacement of conventional ignition technologies with more efficient electronic systems. The integration of ignition systems with digital engine control architectures is further enhancing system precision and responsiveness. Additionally, the transition toward more electric aircraft is encouraging the adoption of ignition systems that reduce mechanical complexity and support energy-efficient operations. Continuous maintenance cycles and component replacements are also contributing to sustained aftermarket demand. Technological advancements in ignition design are improving durability, reducing system weight, and enabling better fuel optimization, which collectively strengthen the long-term outlook of the aircraft ignition system market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $491.4 Million |

| Forecast Value | $929.6 Million |

| CAGR | 6.7% |

The turbine propulsion engines segment held a share of 44.6% in 2025, maintaining its leading position due to its widespread deployment across aviation platforms requiring high-performance ignition systems. These systems are designed to operate under demanding conditions, ensuring consistent and reliable engine ignition. The segment continues to benefit from ongoing aircraft production and increasing operational cycles, which drive the need for robust and durable ignition components. High safety standards and stringent performance requirements further support continuous adoption within this segment.

The fixed-wing aircraft segment generated USD 212.7 million in 2025, driven by its extensive presence across global aviation fleets. The segment benefits from high aircraft volumes, continuous deliveries, and frequent long-duration operations that necessitate dependable ignition systems. Demand is reinforced by the need for consistent engine performance, compliance with strict aviation regulations, and compatibility with evolving engine technologies. The segment remains central to market growth due to its operational scale and continuous technological upgrades.

North America Aircraft Ignition System Market accounted for 36.3% share in 2025, reflecting strong regional demand supported by regulatory advancements and technological adoption. The market in this region is expanding due to increasing focus on engine efficiency, emissions reduction, and maintenance optimization. Operators are transitioning toward advanced ignition systems that deliver improved performance, reduced wear, and enhanced fuel efficiency. Continued investments in aviation infrastructure and modernization programs further strengthen regional market growth.

Key companies operating in the Aircraft Ignition System Industry include Honeywell International Inc., TransDigm Group Incorporated, Woodward, Inc., Unison Industries, Meggitt PLC, Champion Aerospace LLC, Hartzell Engine Technologies, Kelly Aerospace, Inc., Aero Accessories, Inc., Continental Aerospace Technologies, Electroair, Tempest Aero Group, G3i Ignition, Sky Dynamics Corporation, and SureFly Partners Ltd. Companies in the Aircraft Ignition System Market are focusing on innovation, strategic partnerships, and product advancement to strengthen their competitive position. Many players are investing in the development of lightweight, high-efficiency ignition systems that integrate seamlessly with digital engine platforms. Expanding aftermarket services and maintenance solutions is another key strategy to ensure recurring revenue streams. Companies are also forming collaborations with aircraft manufacturers and engine developers to secure long-term supply agreements. Geographic expansion into emerging aviation markets is helping firms capture new growth opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Component trends

- 2.2.3 Engine type trends

- 2.2.4 Platform trends

- 2.2.5 Technology maturity trends

- 2.2.6 End-use trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising narrow-body aircraft production across global OEMs

- 3.2.1.2 Fleet modernization replacing legacy magneto ignition systems

- 3.2.1.3 Growth in low-cost carriers boosting flight frequencies

- 3.2.1.4 Expansion of regional aviation in Asia-Pacific markets

- 3.2.1.5 FADEC integration increasing demand for advanced ignition systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High certification barriers delaying new product approvals

- 3.2.2.2 Long OEM contract cycles limiting supplier entry

- 3.2.3 Market opportunities

- 3.2.3.1 Solid-state ignition systems replacing traditional magneto systems

- 3.2.3.2 Aftermarket demand from aging global aircraft fleet

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Electronic ignition system

- 5.3 Magneto ignition system

- 5.4 Plasma ignition system

- 5.5 Hybrid / others

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Exciters

- 6.3 Ignition control units

- 6.4 Turbine igniters

- 6.5 Piston spark plugs

- 6.6 Ignition leads / cables

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Engine Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Turbine propulsion engines

- 7.3 Reciprocating propulsion engines

- 7.4 Auxiliary power systems

Chapter 8 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Fixed-wing aircraft

- 8.3 Rotary-wing aircraft

- 8.4 Unmanned aerial vehicles (UAVs) - engine-based

Chapter 9 Market Estimates and Forecast, By Technology Maturity, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Conventional ignition systems

- 9.3 Advanced ignition systems

Chapter 10 Market Estimates and Forecast, By End-use, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Original equipment manufacturer (OEM)

- 10.3 Aftermarket

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Honeywell International Inc.

- 12.1.2 Woodward, Inc.

- 12.1.3 TransDigm Group Incorporated

- 12.1.4 Meggitt PLC

- 12.1.5 Unison Industries

- 12.1.6 Champion Aerospace LLC

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Electroair

- 12.2.1.2 Hartzell Engine Technologies

- 12.2.1.3 Kelly Aerospace, Inc.

- 12.2.1.4 G3i Ignition

- 12.2.2 Asia Pacific

- 12.2.2.1 Sky Dynamics Corporation

- 12.2.3 Europe

- 12.2.3.1 Continental Aerospace Technologies

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Tempest Aero Group

- 12.3.2 SureFly Partners Ltd.

- 12.3.3 Aero Accessories, Inc.