|

시장보고서

상품코드

2027673

일반의약품 : 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Over the Counter (OTC) Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

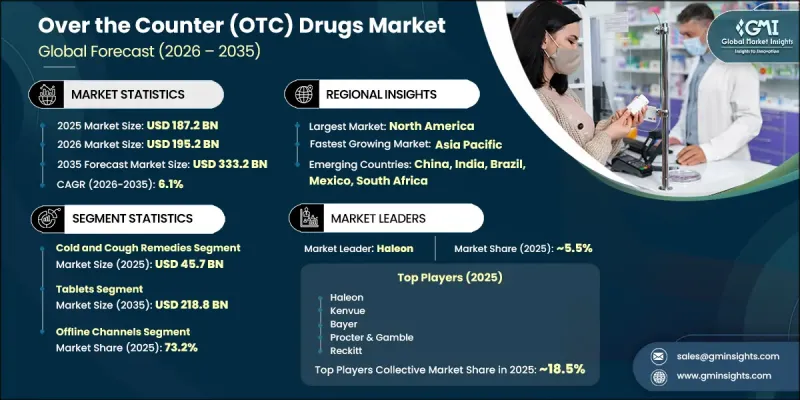

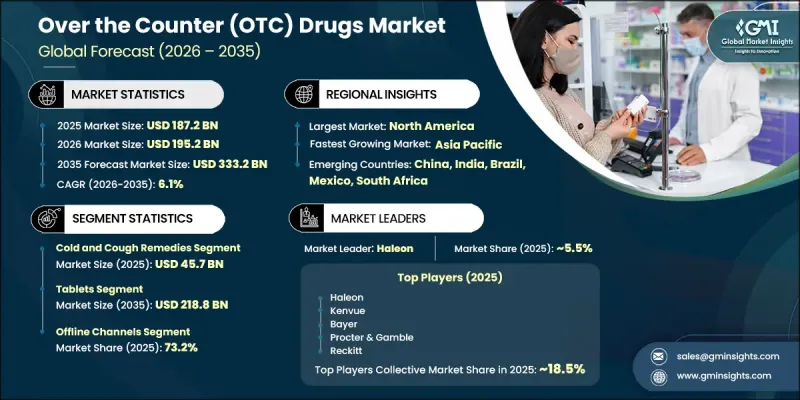

세계의 일반의약품 시장은 2025년에 1,872억 달러로 평가되었고 CAGR 6.1%를 나타내 2035년까지 3,332억 달러에 이를 것으로 추정되고 있습니다.

이 성장 궤도는 소비자가 일상적인 건강 문제를 해결하기 위해 일반의약품에 대한 의존도가 높아지면서 셀프 케어에 대한 뚜렷한 변화로 인해 형성되고 있습니다. 의료비 상승과 의료 정보에 대한 접근성 확대로 인해 개인은 임상적 개입 없이도 경미한 증상을 관리할 수 있는 방법을 모색하고 있습니다. 또한, 예방 의료 및 전반적인 건강 유지에 대한 인식이 높아진 데다 소비층이 확대되는 인구 통계학적 변화까지 더해져 수요는 더욱 증가하고 있습니다. 디지털 및 소매 플랫폼에서 제품의 가용성이 지속적으로 증가함에 따라 최종 사용자의 편의성과 접근성이 향상되면서 시장은 계속해서 혜택을 받고 있습니다. 또한, 처방약에서 일반의약품으로 전환할 수 있는 우호적인 규제 지원으로 제품 접근성이 확대되었고, 경쟁력 있는 가격 전략과 제네릭 의약품의 등장으로 저렴한 가격으로 쉽게 접근할 수 있게 되었습니다. 안전성과 유효성이 규제된 일반의약품은 셀프 케어 실천의 핵심 요소로, 시장의 꾸준한 성장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 1,872억 달러 |

| 예측액 | 3,332억 달러 |

| CAGR | 6.1% |

2025년 감기 및 기침 치료제 부문은 457억 달러로 전체 시장에서 선두를 유지했습니다. 수요는 신속하고 간편한 증상 관리가 필요한 호흡기 질환의 빈번한 발생에 의해 주도되고 있습니다. 소비자들은 여전히 빠른 효과가 있는 일반의약품을 선호하고 있으며, 이는 이 부문의 지속적인 성장에 기여하고 있습니다.

정제 부문은 2025년 1,198억 달러에 달했고, 2035년까지 2,188억 달러에 달할 것으로 예상되며, 제형 카테고리에서 우위를 점하고 있습니다. 정제는 편의성, 정확한 복용량, 보관의 용이성으로 인해 널리 선호되고 있으며, 자가 투약 치료에 있어 실용적인 선택이 되고 있습니다. 지속적인 신제품 출시와 규제 당국의 승인으로 다양한 치료 분야에서 정제의 가용성과 보급이 더욱 강화되고 있습니다.

북미의 일반의약품 시장은 2025년 31.9%의 점유율을 차지했으며, 이는 세계 시장에서의 확고한 입지를 반영했습니다. 이 지역은 잘 구축된 의료 시스템, 높은 자기 관리 의식, 다양한 일반의약품에 대한 광범위한 접근성 등의 이점을 누리고 있습니다. 만성질환과 생활습관병의 유병률 증가가 안정적인 수요를 뒷받침하는 한편, 첨단 소매 및 디지털 유통 채널이 제품 도달 범위와 소비자 참여를 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 의약품 카테고리별(2022-2035년)

제6장 시장 추산 및 예측 : 제제 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 유통 채널별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTH 26.05.20The Global Over the Counter Drugs Market was valued at USD 187.2 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 333.2 billion by 2035.

The growth trajectory is shaped by a clear shift toward self-directed healthcare, where consumers increasingly rely on non-prescription medications to address routine health concerns. Rising healthcare costs and broader access to medical information have encouraged individuals to manage minor conditions without clinical intervention. Demand has also strengthened due to heightened awareness around preventive care and general wellness, alongside demographic shifts that expand the consumer base. The market continues to benefit from the growing availability of products across digital and retail platforms, improving accessibility and convenience for end users. In addition, favorable regulatory support enabling prescription-to-non-prescription transitions has widened product availability, while competitive pricing strategies and generic alternatives have improved affordability. Over the counter drugs, regulated for safety and effectiveness, remain a core component of self-care practices, supporting consistent market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $187.2 Billion |

| Forecast Value | $333.2 Billion |

| CAGR | 6.1% |

The cold and cough remedies segment accounted for USD 45.7 billion in 2025, maintaining a leading position within the overall market. Demand is driven by the frequent occurrence of respiratory-related conditions that require quick and accessible symptom management. Consumers continue to prefer readily available non-prescription solutions that provide immediate relief, contributing to sustained segment growth.

The tablets segment generated USD 119.8 billion in 2025 and is projected to reach USD 218.8 billion by 2035, reinforcing its dominance in the dosage form category. Tablets are widely preferred due to their convenience, precise dosage, and ease of storage, making them a practical choice for self-administered treatment. Continuous product introductions and regulatory approvals have further strengthened their availability and adoption across various therapeutic categories.

North America Over the Counter Drugs Market held a share of 31.9% in 2025, reflecting its strong position in the global landscape. The region benefits from well-established healthcare systems, high awareness of self-care practices, and widespread access to a diverse range of non-prescription medications. The increasing prevalence of chronic and lifestyle-related conditions continues to support consistent demand, while advanced retail and digital distribution channels enhance product reach and consumer engagement.

Key companies operating in the Over The Counter Drugs Market include Abbott Laboratories, Bayer, Cipla, Haleon, Kenvue, Reckitt, Sanofi, Perrigo Company, Procter & Gamble Company, Teva Pharmaceutical, Dr. Reddy's Laboratories, Sun Pharma, Glenmark Pharmaceuticals, Himalaya Wellness Company, Piramal Pharma, Alkem Laboratories, Taisho Pharmaceutical, Stada Arzneimittel, and Alinamin Pharmaceutical (The Blackstone Group). Companies in the Over the Counter Drugs Market are strengthening their competitive position through continuous product innovation, portfolio expansion, and strategic regulatory approvals. They are investing in research and development to introduce advanced formulations that enhance efficacy, safety, and convenience for consumers. Expanding digital presence through e-commerce platforms and pharmacy applications is improving product accessibility and customer engagement. Firms are also leveraging branding, targeted marketing, and consumer education initiatives to build trust and increase awareness. Strategic partnerships, mergers, and acquisitions enable companies to broaden their geographic footprint and distribution networks. Additionally, a strong focus on cost optimization, private-label offerings, and sustainable packaging solutions is helping organizations align with evolving consumer preferences and regulatory expectations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Business trends

- 2.2.2 Regional trends

- 2.2.3 Drug category trends

- 2.2.4 Formulation type trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing consumer awareness for self-medication and disease management

- 3.2.1.2 High cost of prescription drugs leading to shift towards OTC drugs

- 3.2.1.3 Favorable regulatory support for OTC drug approvals

- 3.2.1.4 Expanding product accessibility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Concerns regarding misuse or drug abuse

- 3.2.2.2 Potential side effects and drug interactions

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets expansion

- 3.2.3.2 Increasing penetration and adoption of e-pharmacies and online platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology/innovation landscape

- 3.5.1 Novel drug delivery systems for OTC products

- 3.5.2 Smart packaging & patient adherence technologies

- 3.6 Prescription to nonprescription switch list

- 3.7 Patent landscape (Driven by Primary Research)

- 3.8 Self-care & consumer health behavior trends

- 3.9 Future market trends (Driven by Primary Research)

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Category, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cold and cough remedies

- 5.3 Vitamins and supplements

- 5.4 Digestive and intestinal remedies

- 5.5 Skin treatment

- 5.6 Analgesics

- 5.7 Sleeping aids

- 5.8 Other drug categories

Chapter 6 Market Estimates and Forecast, By Formulation Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Tablets

- 6.3 Liquids

- 6.4 Ointments

- 6.5 Sprays

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Online channels

- 7.3 Offline channels

- 7.3.1 Hospital pharmacies

- 7.3.2 Retail pharmacies

- 7.3.3 Other offline channels

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Alinamin Pharmaceutical (The Blackstone Group)

- 9.3 Alkem Laboratories

- 9.4 Bayer

- 9.5 Cipla

- 9.6 Dr. Reddy’s Laboratories

- 9.7 Glenmark Pharmaceuticals

- 9.8 Haleon

- 9.9 Himalaya Wellness Company

- 9.10 Kenvue

- 9.11 Perrigo Company

- 9.12 Piramal Pharma

- 9.13 Procter & Gamble Company

- 9.14 Reckitt

- 9.15 Sanofi

- 9.16 Stada Arzneimittel

- 9.17 Sun Pharma

- 9.18 Taisho Pharmaceutical

- 9.19 Teva Pharmaceutical