|

시장보고서

상품코드

2038304

항공기 예측 유지보수 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aircraft Predictive Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

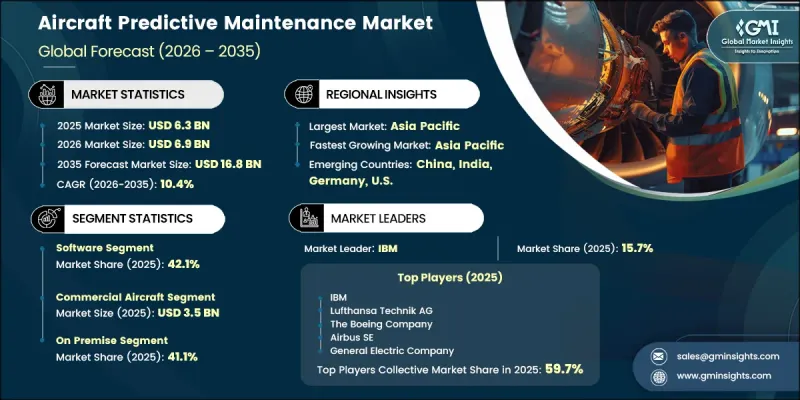

세계의 항공기 예측 유지보수 시장은 2025년에 63억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.4%로 성장할 전망이며, 168억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장은 운영의 복잡성 증가, 효율성에 대한 수요 증가, 항공기 시스템의 지속적인 디지털 전환에 의해 주도되고 있습니다. 항공사와 항공업계의 이해관계자들은 성능 향상, 다운타임 감소, 수명주기 관리 최적화를 위해 예지보전을 더욱 중요하게 여기고 있습니다. 커넥티드 항공기 기술, 통합 모니터링 시스템, 향상된 기내 진단 기술의 발전은 예방적 유지보수 방법의 도입을 촉진하고 있습니다. 고급 분석 기술의 사용 확대와 더불어 안전 기준의 발전과 전 세계 항공 교통량 증가는 다양한 항공 분야에서 예지 정비 솔루션의 확장을 지속적으로 촉진하고 있으며, 이는 항공기 예지 정비 시장의 장기적인 전망을 더욱 견고하게 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 63억 달러 |

| 예측 시장 규모 | 168억 달러 |

| CAGR | 10.4% |

항공기 예측 유지보수 산업은 항공 수요의 지속적인 증가와 함께 정확하고 시기적절한 보전에 대한 지식에 대한 요구가 높아지면서 성장세를 보이고 있습니다. 항공기 보유 대수가 늘어나고 운항 스케줄이 엄격해짐에 따라 항공사는 잠재적인 문제를 예측하고 효율성을 향상시킬 수 있는 첨단 모니터링 시스템에 대한 의존도가 높아지고 있습니다. 또한, 규제 프레임워크는 운항 신뢰성과 안전에 점점 더 중점을 두고 있으며, 모니터링 역량을 강화하고 항공 운항 전반의 기술적 위험을 최소화하는 데이터 기반 유지보수 시스템의 도입을 촉진하고 있습니다.

2025년에는 소프트웨어 부문이 42.1%의 점유율을 차지했습니다. 이 부문의 선도적 지위는 실시간 데이터 처리, 예측 분석, 자동화된 유지보수 스케줄링을 가능하게 하는 첨단 디지털 플랫폼에 대한 의존도가 높아짐에 따라 뒷받침되고 있습니다. 커넥티드 시스템과 디지털 통합 워크플로우로의 전환은 예지보전 업무에서 소프트웨어 기반 솔루션의 중요성을 더욱 강화시키고 있습니다.

민간 항공기 부문은 세계 항공기 보유 규모와 운영 밀도에 힘입어 2025년 35억 달러에 달했습니다. 높은 가동률을 유지하고 일관된 성능을 보장하기 위해 항공사는 스케줄링의 효율성을 높이고 운항 중단을 줄이기 위해 예지보전 솔루션을 도입하고 있습니다. 이 부문에서 선진 정비 기술을 적극적으로 도입하여 선도적인 지위를 유지하고 있습니다.

북미의 항공기 예측 유지보수 시장은 첨단 항공기술의 빠른 도입과 높은 기체 연결성을 바탕으로 2025년 36.5%의 점유율을 차지했습니다. 이 지역 시장 성장은 운영 효율성에 대한 수요 증가와 디지털 항공 인프라에 대한 적극적인 투자에 의해 주도되고 있습니다. 항공업계의 이해관계자들은 예측 분석을 통한 정비 프로세스 강화에 집중하고 있으며, 이는 지역 전체의 지속적인 시장 확대에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 컴포넌트별(2022-2035년)

제6장 시장 추산 및 예측 : 항공기 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 전개 형태별(2022-2035년)

제8장 시장 추산 및 예측 : 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

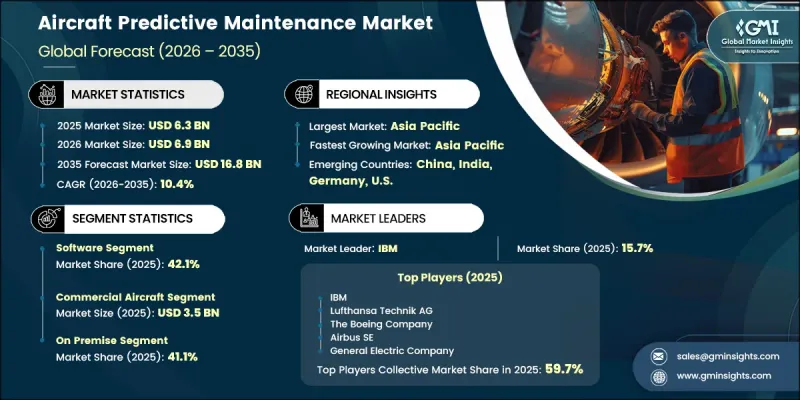

AJY 26.06.11The Global Aircraft Predictive Maintenance Market was valued at USD 6.3 billion in 2025 and is estimated to grow at a CAGR of 10.4% to reach USD 16.8 billion by 2035.

The growth is driven by increasing operational complexity, rising demand for efficiency, and the ongoing digital transformation of aircraft systems. Airlines and aviation stakeholders are placing greater emphasis on predictive maintenance to improve performance, reduce downtime, and optimize lifecycle management. Advancements in connected aircraft technologies, integrated monitoring systems, and enhanced onboard diagnostics are strengthening the adoption of proactive maintenance approaches. The increasing use of advanced analytics, combined with evolving safety standards and rising global air traffic, continues to support the expansion of predictive maintenance solutions across various aviation segments, reinforcing the long-term outlook of the aircraft predictive maintenance market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.3 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 10.4% |

The aircraft predictive maintenance industry is gaining traction due to the continuous rise in air travel demand, which is intensifying the need for accurate and timely maintenance insights. Expanding aircraft fleets and tighter operational schedules are encouraging aviation operators to rely on advanced monitoring systems that can anticipate potential issues and improve efficiency. Additionally, regulatory frameworks are increasingly focusing on operational reliability and safety, promoting the adoption of data-driven maintenance systems that enhance monitoring capabilities and minimize technical risks across aviation operations.

The software segment accounted for 42.1% share in 2025. This segment's leadership is supported by the growing reliance on advanced digital platforms that enable real-time data processing, predictive analytics, and automated maintenance scheduling. The shift toward connected systems and digitally integrated workflows continues to reinforce the importance of software-driven solutions in predictive maintenance operations.

The commercial aircraft segment reached USD 3.5 billion in 2025, driven by the scale and operational intensity of global aviation fleets. The need to maintain high utilization rates and ensure consistent performance is encouraging operators to adopt predictive maintenance solutions that enhance scheduling efficiency and reduce operational disruptions. Strong adoption of advanced maintenance technologies within this segment continues to support its leading position.

North America Aircraft Predictive Maintenance Market accounted for 36.5% share in 2025, supported by rapid adoption of advanced aviation technologies and high levels of fleet connectivity. Market growth in the region is being fueled by increasing demand for operational efficiency, along with strong investment in digital aviation infrastructure. Aviation stakeholders are focusing on enhancing maintenance processes through predictive analytics, contributing to sustained market expansion across the region.

Key players in the Global Aircraft Predictive Maintenance Market include Microsoft Corporation, The Boeing Company, IBM, Airbus SE, Honeywell International Inc., Lufthansa Technik AG, General Electric Company, Thales Group, SAP SE, Safran Aircraft Engines, Rolls-Royce Holdings plc, Pratt & Whitney, Delta TechOps, Air France KLM Engineering & Maintenance, ST Engineering Aerospace, Swiss Aviation Software, CAMP Systems International Inc., Aviation Intertec Services Inc., Veryon, and Wingops. Companies operating in the aircraft predictive maintenance market are strengthening their competitive position through a combination of technological innovation, strategic alliances, and global expansion initiatives. They are focusing on developing advanced analytics platforms powered by artificial intelligence and machine learning to improve predictive accuracy and operational efficiency. Partnerships with aviation stakeholders are enabling companies to integrate their solutions across broader ecosystems and enhance service capabilities. Organizations are also expanding their presence in high-growth regions to capture emerging opportunities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Aircraft type trends

- 2.2.3 Deployment trends

- 2.2.4 Application trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising air traffic and fleet expansion

- 3.2.1.2 Expansion of connected aircraft and digital aviation infrastructure

- 3.2.1.3 Regulatory emphasis on safety, reliability, and maintenance transparency

- 3.2.1.4 Rising demand for real-time aircraft health monitoring

- 3.2.1.5 Growing adoption of AI, machine learning, and digital twins in aviation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High integration cost of predictive maintenance systems

- 3.2.2.2 Limited availability of high-quality, standardized aircraft operational data

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of next-generation connected aircraft programs

- 3.2.3.2 Increasing adoption of digital-twin and simulation technology by airlines and OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge Computing Devices

- 5.2.2 Sensors & IoT Devices

- 5.2.3 Flight Data Recorders & Health Monitoring Units

- 5.2.4 Connectivity modules

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Predictive analytics software

- 5.3.2 Condition-based monitoring platforms

- 5.3.3 Digital Twin Solutions

- 5.3.4 Data Management & Integration Software

- 5.3.5 Others

- 5.4 Services

- 5.4.1 System Integration & Implementation

- 5.4.2 Consulting & Advisory Services

- 5.4.3 Training & Enablement

- 5.4.4 Support & Maintenance

- 5.4.5 Others

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Commercial Aircraft

- 6.2.1 Narrow-body aircraft

- 6.2.2 Wide-body aircraft

- 6.2.3 Regional jets

- 6.3 Military Aircraft

- 6.3.1 Fighter Jets & Combat Aircraft

- 6.3.2 Transport & Tanker Aircraft

- 6.3.3 Surveillance & Reconnaissance Aircraft

- 6.3.4 Others

- 6.4 Business Jets

- 6.5 Rotary-Wing Aircraft

Chapter 7 Market Estimates and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 On premise

- 7.3 Cloud

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Engine Health Monitoring

- 8.2.1 Turbofan & Turbojet Engines

- 8.2.2 Turboprop Engines

- 8.2.3 Auxiliary Power Units (APU)

- 8.2.4 Others

- 8.3 Airframe Health Monitoring

- 8.3.1 Structural Integrity Monitoring

- 8.3.2 Environmental Control Systems

- 8.3.3 Hydraulic Systems

- 8.3.4 Others

- 8.4 Avionics & Systems Monitoring

- 8.4.1 Flight Control Systems

- 8.4.2 Navigation & Communication Systems

- 8.4.3 Cockpit Instrumentation

- 8.4.4 Others

- 8.5 Landing Gear Monitoring

- 8.5.1 Brakes & Wheels

- 8.5.2 Shock Absorbers & Actuation Systems

- 8.5.3 Others

- 8.6 Connectivity & Data Transmission Systems

- 8.7 Other

Chapter 9 Market Estimates and Forecast, By End-user, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Original Equipment Manufacturers (OEMs)

- 9.3 Airlines & Operators

- 9.4 MRO Service Providers

- 9.5 Lessors & Fleet Managers

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 IBM

- 11.1.2 Lufthansa Technik AG

- 11.1.3 The Boeing Company

- 11.1.4 Airbus SE

- 11.1.5 General Electric Company

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Honeywell International Inc.

- 11.2.1.2 Pratt & Whitney

- 11.2.1.3 Delta TechOps

- 11.2.1.4 Microsoft Corporation

- 11.2.1.5 CAMP Systems International Inc.

- 11.2.1.6 Aviation Intertec Services Inc.

- 11.2.1.7 Veryon

- 11.2.2 Asia Pacific

- 11.2.2.1 ST Engineering Aerospace

- 11.2.3 Europe

- 11.2.3.1 Thales Group

- 11.2.3.2 Safran Aircraft Engines

- 11.2.3.3 Air France KLM Engineering & Maintenance

- 11.2.3.4 Rolls-Royce Holdings plc

- 11.2.3.5 SAP SE

- 11.2.3.6 Swiss Aviation Software

- 11.2.3.7 Wingops

- 11.2.1 North America