|

시장보고서

상품코드

2038307

산업용 머신 비전 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Machine Vision Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

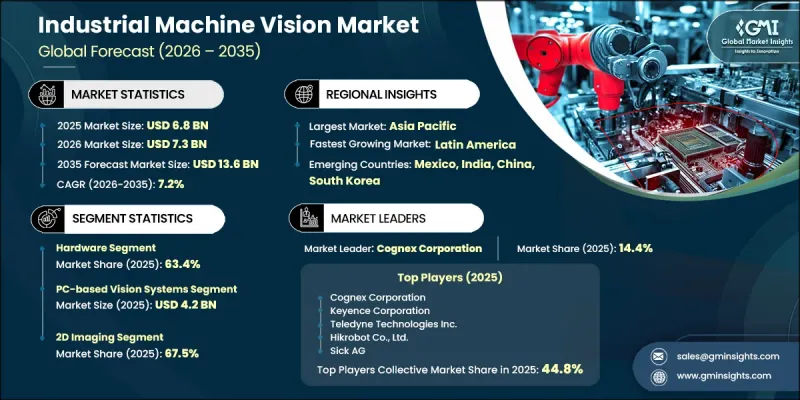

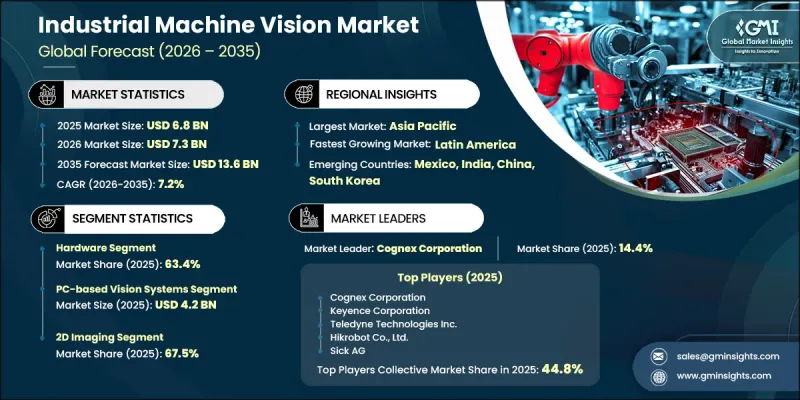

세계의 산업용 머신 비전 시장은 2025년에 68억 달러로 평가되었고, CAGR 7.2%로 성장할 전망이며, 2035년까지 136억 달러에 이를 것으로 추정되고 있습니다.

산업용 머신비전 산업의 성장은 이산형 및 공정형 제조 환경 모두에서 자동 검사 시스템의 도입 확대에 힘입어 성장하고 있습니다. 고정밀 품질 관리에 대한 수요 증가와 AI를 활용한 비전 기술의 급속한 발전이 맞물려 시장 확대에 박차를 가하고 있습니다. 엄격한 규정 준수가 요구되는 분야의 규제 요건도 제조업체들이 신뢰할 수 있는 검사 솔루션을 도입하도록 유도하고 있습니다. 또한, 스마트 제조 생태계와 인더스트리 4.0 프레임워크의 지속적인 발전으로 생산 라인에 머신비전 시스템의 통합이 가속화되고 있습니다. 이러한 기술은 업무 효율성 향상, 결함 감지 능력 향상 및 일관성 향상을 실현하여 산업용 머신비전 시장은 지속적이고 장기적인 성장 궤도에 올라서고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 68억 달러 |

| 예측 시장 규모 | 136억 달러 |

| CAGR | 7.2% |

산업용 머신비전 시장은 고정밀 산업에서 무결점 생산의 실현이 점점 더 중요해짐에 따라 더욱 확대되고 있습니다. 제조업체들은 제품 품질 향상, 운영 리스크 감소, 엄격한 기준 준수를 위해 첨단 검사 기술 도입에 박차를 가하고 있습니다. 인공지능(AI)의 통합으로 감지 능력이 크게 향상되어 기존 방식에 비해 시스템이 더 높은 정확도로 복잡한 결함을 식별할 수 있게 되었습니다. 이러한 기술적 변화는 현대 제조 공정에서 머신 비전의 역할을 강화하고 있습니다.

하드웨어 부문은 2025년 63.4%의 점유율을 차지했으며, 시각 데이터 수집 및 처리의 기본 역할로 인해 지배적인 지위를 유지하고 있습니다. 이러한 시스템은 자동화 환경에 필수적인 고속 검사 및 정밀 측정 기능을 지원하므로, 다양한 산업 분야에서 이미징 부품의 광범위한 사용은 지속적으로 안정적인 수요를 견인하고 있습니다.

PC 기반 비전 시스템 부문은 2025년 42억 달러에 달했습니다. 이 부문은 강력한 처리 능력, 유연성, 고급 데이터 처리가 필요한 복잡한 용도에 대한 적응성으로 인해 성장세를 보이고 있습니다. 확장 가능한 아키텍처와 맞춤형 구성을 지원하는 능력으로 인해 현대 산업 비전 도입에 필수적인 요소로 자리 잡았습니다.

북미의 산업용 머신비전 시장은 제조 기술의 급속한 발전과 정밀 생산에 대한 관심이 높아짐에 따라 2025년 19.7%의 점유율을 차지했습니다. 이 지역에서는 생산성과 업무 효율성을 높이기 위해 자동화 솔루션과 통합된 지능형 비전 시스템 도입이 빠르게 진행되고 있습니다. 첨단 제조 인프라에 대한 투자 확대와 완전 자동화된 생산 환경에 대한 수요 증가는 북미 전역 시장 성장을 더욱 촉진하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 컴포넌트별(2022-2035년)

제6장 시장 추산 및 예측 : 제품 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 이미징 기술별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자 산업별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJYThe Global Industrial Machine Vision Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 13.6 billion by 2035.

Growth in the industrial machine vision industry is being supported by the rising adoption of automated inspection systems across both discrete and process manufacturing environments. Increasing demand for high-accuracy quality control, combined with rapid progress in AI-enabled vision technologies, is strengthening market expansion. Regulatory requirements in sectors that demand strict compliance are also pushing manufacturers to implement reliable inspection solutions. In addition, the ongoing development of smart manufacturing ecosystems and Industry 4.0 frameworks is accelerating the integration of machine vision systems into production lines. These technologies are enabling enhanced operational efficiency, improved defect detection, and greater consistency, positioning the industrial machine vision market for sustained long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $13.6 Billion |

| CAGR | 7.2% |

The industrial machine vision market is further driven by the growing emphasis on achieving defect-free production across high-precision industries. Manufacturers are increasingly adopting advanced inspection technologies to enhance product quality, reduce operational risks, and maintain compliance with strict standards. The integration of artificial intelligence is significantly improving detection capabilities, enabling systems to identify complex defects with greater accuracy compared to traditional approaches. This technological shift is reinforcing the role of machine vision in modern manufacturing processes.

The hardware segment accounted for 63.4% share in 2025, maintaining a dominant position due to its fundamental role in capturing and processing visual data. The widespread use of imaging components across various industries continues to drive consistent demand, as these systems support high-speed inspection and precise measurement capabilities essential for automated environments.

The PC-based vision systems segment reached USD 4.2 billion in 2025. This segment is gaining traction due to its strong processing capabilities, flexibility, and suitability for complex applications that require advanced data handling. Its ability to support scalable architectures and customized configurations makes it a critical component in modern industrial vision deployments.

North America Industrial Machine Vision Market held a 19.7% share in 2025, driven by rapid advancements in manufacturing technologies and increasing focus on precision-driven production. The region is experiencing strong adoption of intelligent vision systems integrated with automation solutions to improve productivity and operational efficiency. Growing investments in advanced manufacturing infrastructure and increasing demand for fully automated production environments are further supporting market growth across North America.

Key companies operating in the Global Industrial Machine Vision Market include Cognex Corporation, Keyence Corporation, Basler AG, Teledyne Technologies Inc., Omron Corporation, Zebra Technologies Corp., Allied Vision Technologies GmbH, Sick AG, STEMMER IMAGING AG, Hikrobot Co., Ltd., Matrox Imaging, National Instruments Corporation, LUCID Vision Labs Inc., JAI A/S, and Hermary Opto Electronics Inc. Companies in the industrial machine vision market are focusing on technological innovation, partnerships, and global expansion to strengthen their market position. They are investing in AI-driven vision solutions and advanced imaging technologies to enhance accuracy, speed, and efficiency. Strategic collaborations with automation providers and system integrators are enabling broader deployment across industries. Many companies are also expanding into emerging markets to capture new growth opportunities. Additionally, continuous improvements in hardware and software integration, along with the development of scalable and customizable solutions, are helping companies meet diverse industrial requirements while maintaining competitiveness and supporting long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Component trends

- 2.2.2 Product type trends

- 2.2.3 Imaging technology trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation in discrete and process manufacturing

- 3.2.1.2 Increasing demand for zero-defect quality inspection

- 3.2.1.3 AI-powered vision improving defect detection accuracy

- 3.2.1.4 Stringent regulatory standards in pharmaceuticals and food

- 3.2.1.5 Rising adoption of smart factories and Industry 4.0

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial deployment and integration costs

- 3.2.2.2 Complexity in handling unstructured visual environments

- 3.2.3 Market opportunities

- 3.2.3.1 AI-based deep learning vision system advancements

- 3.2.3.2 Integration with edge computing and real-time analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 PC-based vision systems

- 6.3 Smart camera systems

Chapter 7 Market Estimates and Forecast, By Imaging Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 2D imaging

- 7.3 3D imaging

- 7.4 Hyperspectral & multispectral imaging

Chapter 8 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Electronics & semiconductors

- 8.4 Food & beverage

- 8.5 Healthcare & pharmaceutical

- 8.6 Logistics & E-commerce

- 8.7 Aerospace & defense

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Cognex Corporation

- 10.1.2 Keyence Corporation

- 10.1.3 Teledyne Technologies Inc.

- 10.1.4 Omron Corporation

- 10.1.5 Sick AG

- 10.1.6 Zebra Technologies Corp.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 National Instruments Corporation

- 10.2.1.2 LUCID Vision Labs Inc.

- 10.2.1.3 Hermary Opto Electronics Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Hikrobot Co., Ltd.

- 10.2.3 Europe

- 10.2.3.1 Basler AG

- 10.2.3.2 Allied Vision Technologies GmbH

- 10.2.3.3 STEMMER IMAGING AG

- 10.2.3.4 JAI A/S

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Matrox Imaging