|

시장보고서

상품코드

2038309

질화 알루미늄 반도체 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aluminum Nitride (AlN) Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

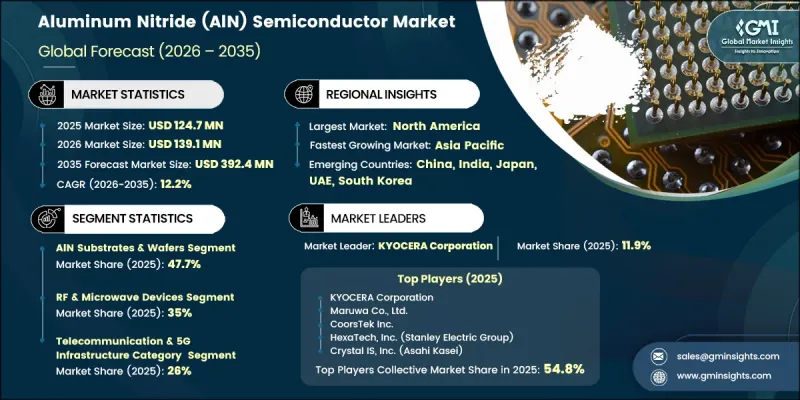

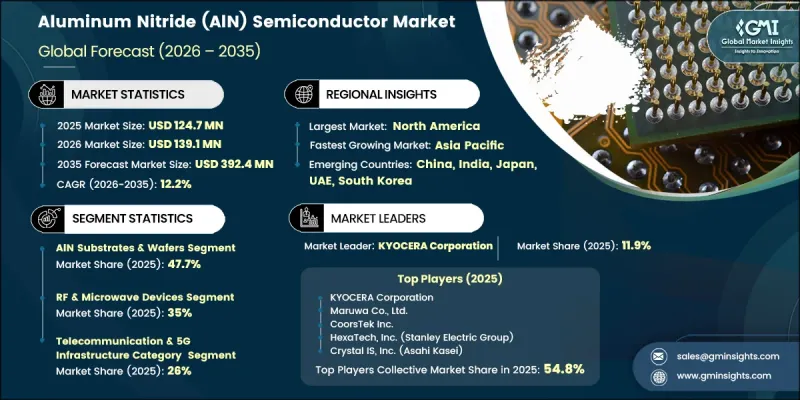

세계의 질화 알루미늄 반도체 시장은 2025년에 1억 2,470만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 12.2%로 성장할 전망이며, 3억 9,240만 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 파워 일렉트로닉스 분야의 첨단 열 관리 소재에 대한 수요 증가, 전기자동차 및 5G 인프라의 광대역 갭 반도체 기술 도입 확대, 고성능 RF 장치 및 광전자 장치의 통합이 주요 요인으로 작용하고 있습니다. 또한, 웨이퍼 제조 방법과 결정 성장 공정의 지속적인 개선은 반도체 용도 전반 시장 발전과 성능 향상에 중요한 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 1억 2,470만 달러 |

| 예측 시장 규모 | 3억 9,240만 달러 |

| CAGR | 12.2% |

질화 알루미늄 반도체 시장의 성장은 고출력 전자 시스템에서 효율적인 방열 솔루션에 대한 수요 증가에 크게 영향을 받고 있습니다. 파워 반도체 소자의 열 제어 개선 요구사항에 따라 열전도율이 높은 질화 알루미늄 기판과 세라믹 소재의 채택이 증가하고 있는 것이 주요한 추세입니다. 또 다른 중요한 추세는 차세대 RF 및 광전자 부품 제조에 단결정 질화 알루미늄 웨이퍼의 활용이 확대되고 있다는 점입니다. 이는 제조업체들이 결정 품질과 성능 특성 향상에 집중하면서 최근 몇 년 동안 더욱 활발해지고 있습니다.

질화 알루미늄 기판 및 웨이퍼 부문은 고출력 및 고주파 전자시스템의 기판으로 중요한 역할을 하고 있어 2025년 47.7%의 점유율을 차지했습니다. 이러한 재료는 우수한 열전도율, 높은 전기 절연성 및 격자 적합성으로 인해 RF 기술, 전력 전자 및 자외선 광전자 용도 분야에서 널리 사용되고 있습니다. 단결정 웨이퍼 제조 기술의 지속적인 발전은 반도체 가치사슬 전반 수요를 더욱 강화하여 첨단 전자 시스템에 대한 광범위한 채택을 뒷받침하고 있습니다.

RF 및 마이크로파 디바이스 분야는 고주파 및 고출력 통신 기술에 대한 강한 수요로 인해 2025년 35%의 점유율을 차지했습니다. 질화 알루미늄 소재는 높은 열 안정성, 높은 항복 전압 및 열악한 조건에서 우수한 신호 성능으로 인해 RF 증폭기, 기지국 인프라, 위성 통신 시스템에 널리 사용되고 있습니다. 첨단 통신 네트워크의 급속한 확산과 국방 통신 시스템에 대한 수요 증가는 이 부문의 성장을 더욱 촉진하고, 고성능 전자 플랫폼 전반에 걸쳐 채택을 가속화하고 있습니다.

북미의 질화 알루미늄 반도체 시장은 2025년 31.1%의 점유율을 차지했습니다. 지역적 성장은 전력전자, 5G 인프라, 전기자동차(EV) 용도에서 고효율 열관리 소재에 대한 수요 증가에 힘입어 성장세를 보이고 있습니다. RF 부품, 질화갈륨(GaN) 기반 전력 시스템 및 첨단 전자 장치의 사용 확대는 미국과 캐나다 전역에서 고주파 및 고출력 용도에 질화 알루미늄 기판 및 웨이퍼의 채택을 크게 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 최종 이용 산업별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJY 26.06.11The Global Aluminum Nitride Semiconductor Market was valued at USD 124.7 million in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 392.4 million by 2035.

Market expansion is driven by rising demand for advanced thermal management materials in power electronics, increasing deployment of wide bandgap semiconductor technologies in electric vehicles and 5G infrastructure, and growing integration of high-performance RF and optoelectronic devices. Continuous improvements in wafer fabrication methods and crystal growth processes are also playing a critical role in supporting market advancement and performance enhancement across semiconductor applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $124.7 Million |

| Forecast Value | $392.4 Million |

| CAGR | 12.2% |

The growth of the aluminum nitride semiconductor market is strongly influenced by the rising need for efficient heat dissipation solutions in high-power electronic systems. Increasing adoption of high thermal conductivity aluminum nitride substrates and ceramic materials is a key trend, driven by the requirement for improved thermal control in power semiconductor devices. Another important development is the rising use of single-crystal aluminum nitride wafers in next-generation RF and optoelectronic component manufacturing, which gained momentum in recent years as manufacturers focused on enhancing crystal quality and performance characteristics.

The aluminum nitride substrates and wafers segment held a 47.7% share in 2025, due to its critical role as a base material in high-power and high-frequency electronic systems. These materials are widely utilized in RF technologies, power electronics, and ultraviolet optoelectronic applications because of their superior thermal conductivity, strong electrical insulation, and lattice compatibility properties. Ongoing advancements in single-crystal wafer production techniques are further strengthening demand across the semiconductor value chain, supporting broader adoption in advanced electronic systems.

The RF and microwave devices segment held a 35% share in 2025, due to strong demand for high-frequency and high-power communication technologies. Aluminum nitride materials are extensively used in RF amplifiers, base station infrastructure, and satellite communication systems because of their high thermal stability, strong breakdown voltage, and excellent signal performance under extreme conditions. The rapid rollout of advanced communication networks and increasing demand for defense communication systems are further supporting segment growth and accelerating adoption across high-performance electronic platforms.

North America Aluminum Nitride Semiconductor Market accounted for 31.1% share in 2025. Regional growth is supported by increasing demand for highly efficient thermal management materials across power electronics, 5G infrastructure, and electric vehicle applications. Expanding use of RF components, gallium nitride-based power systems, and advanced electronic devices is significantly driving the adoption of aluminum nitride substrates and wafers in high-frequency and high-power applications across the United States and Canada.

Major players operating in the Global Aluminum Nitride Semiconductor Industry include KYOCERA Corporation, CeramTec GmbH, CoorsTek Inc., Morgan Advanced Materials, Maruwa Co., Ltd., Tokuyama Corporation, Surmet Corporation, HexaTech, Inc. (Stanley Electric Group), Crystal IS, Inc. (Asahi Kasei Corporation), American Elements, Fraunhofer IISB, Stanford Advanced Materials, Kyma Technologies, Inc., Xiamen Innovacera Advanced Materials Co., Ltd., XI'AN FUNCTION MATERIAL GROUP CO., LTD., and Nishimura Advanced Ceramics Co., Ltd. Key strategies adopted by companies in the Aluminum Nitride Semiconductor Market focus on strengthening crystal growth technologies, expanding high-quality wafer production capacity, and improving thermal conductivity performance for advanced electronic applications. Firms are heavily investing in R&D to enhance single-crystal fabrication techniques and reduce production defects. Strategic collaborations with semiconductor manufacturers and electronics OEMs are helping accelerate commercialization of AlN-based solutions. Companies are also expanding global supply chains to ensure material availability and cost efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 End-use Industry trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-performance thermal management in power electronics

- 3.2.1.2 Increasing adoption of GaN-based devices in EV and 5G infrastructure

- 3.2.1.3 Expanding use of AlN substrates in RF and high-frequency applications

- 3.2.1.4 Growing investments in advanced semiconductor manufacturing ecosystems

- 3.2.1.5 Rising demand for miniaturized, high-power density electronic devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited industrial composting infrastructure in emerging economies

- 3.2.2.2 Performance limitations in moisture and oxygen barrier properties

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AlN-based advanced packaging in high-power semiconductor modules

- 3.2.3.2 Integration of AlN in next-generation wide bandgap semiconductor ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends (Based on paid Database)

- 3.7.1 Historical Price Analysis (2022-2025)

- 3.7.2 Price Trend Drivers

- 3.7.3 Regional Price Variations

- 3.7.4 Price Forecast (2026-2035)

- 3.8 Trade Data Analysis (Based on Paid Database)

- 3.8.1 Import/Export Volume & Value Trends

- 3.8.2 Key Trade Corridors & Tariff Impact

- 3.9 Impact of AI & Generative AI on the Market

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 AlN substrates & wafers

- 5.3 AlN epitaxial films & layers

- 5.4 AlN-based semiconductor devices

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Power electronics

- 6.3 RF & microwave devices

- 6.4 Deep UV optoelectronics

- 6.5 Piezoelectric & acoustic wave devices

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Telecommunications & 5G infrastructure

- 7.3 Automotive & electric vehicles

- 7.4 Healthcare & life sciences

- 7.5 Industrial & energy

- 7.6 Consumer electronics & IT

- 7.7 Defense & aerospace

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 KYOCERA Corporation

- 9.1.2 Tokuyama Corporation

- 9.1.3 CoorsTek Inc.

- 9.1.4 CeramTec GmbH

- 9.1.5 Morgan Advanced Materials

- 9.1.6 Maruwa Co., Ltd.

- 9.2 Regional Players

- 9.2.1 HexaTech, Inc. (Stanley Electric Group)

- 9.2.2 Crystal IS, Inc. (Asahi Kasei Corporation)

- 9.2.3 Kyma Technologies, Inc.

- 9.2.4 Nishimura Advanced Ceramics Co., Ltd.

- 9.2.5 Surmet Corporation

- 9.2.6 Fraunhofer IISB

- 9.3 Local Players

- 9.3.1 Xiamen Innovacera Advanced Materials Co., Ltd.

- 9.3.2 Stanford Advanced Materials

- 9.3.3 American Elements

- 9.3.4 XI'AN FUNCTION MATERIAL GROUP CO., LTD.