|

시장보고서

상품코드

2038331

부식 방지 포장 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Anti-Corrosion Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

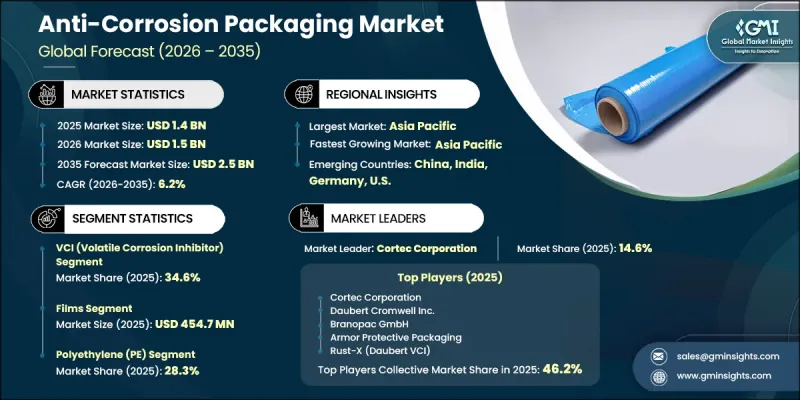

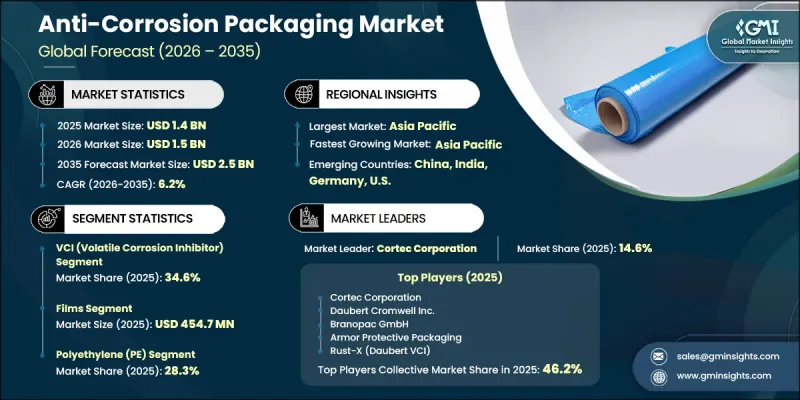

세계의 부식 방지 포장 시장은 2025년에 14억 달러로 평가되었고, CAGR 6.2%로 성장할 전망이며, 2035년까지 25억 달러에 이를 것으로 예측됩니다.

제조업 전반의 생산량 증가에 따라 보관 및 운송 중 금속 부품을 보호하는 효과적인 부식 방지 솔루션에 대한 수요가 증가하고 있습니다. 전 세계 물류 네트워크가 지속적으로 확대되면서 습기, 산화 등 환경적 요인으로부터 제품을 보호하는 포장의 필요성이 점점 더 중요해지고 있습니다. 각 업계는 제품 손상을 최소화하고, 운영 비용을 절감하고, 내구성 기준을 유지하는 데 중점을 두고 있으며, 이는 첨단 패키징 기술의 도입을 가속화하고 있습니다. 보호 재료와 포장 효율의 지속적인 개선으로 제품의 신뢰성이 더욱 높아지면서 부식 방지 솔루션은 현대 산업 공급망에서 없어서는 안 될 필수 요소로 자리 잡았습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 14억 달러 |

| 예측 시장 규모 | 25억 달러 |

| CAGR | 6.2% |

부식 방지 포장 시장은 열화에 대한 확실한 보호가 필요한 금속 부품, 기계, 전자 장비의 생산 및 유통 확대에 따라 더욱 촉진되고 있습니다. 세계 무역 네트워크가 확대됨에 따라 상품이 다양한 환경 조건에 노출될 기회가 많아지고, 운송 및 보관 중 부식 위험이 증가하고 있습니다. 이에 따라, 특히 복잡한 물류 요구사항이 있는 산업에서 제품의 무결성을 유지하고 수명을 연장하도록 설계된 고급 포장 솔루션에 대한 수요가 증가하고 있습니다.

하이브리드 및 다층 시스템 부문은 2035년까지 연평균 복합 성장률(CAGR) 7.2%를 나타낼 것으로 예측됩니다. 이러한 포장 솔루션은 환경 요인에 대한 보호 성능이 강화되어 가혹한 물류 조건에 적합합니다. 다양한 조건에서도 일관된 성능을 발휘하는 능력으로 인해 높은 내구성이 요구되는 산업에서 점점 더 선호되고 있으며, 그 채택이 확대되고 있습니다.

종이 및 판지 부문은 2026-2035년 연평균 복합 성장률(CAGR) 8.7%를 나타낼 것으로 예측됩니다. 이러한 성장은 가볍고 재활용이 가능하며 친환경적인 포장 솔루션에 대한 업계의 관심이 높아짐에 따라 성장세를 보이고 있습니다. 종이 기반 부식 방지 재료는 효과적인 보호 능력과 지속가능성 목표와의 일치로 인해 주목을 받고 있습니다. 이러한 소재에 대한 수용이 확대되고 있는 것은 성능 기준을 유지하면서 환경에 미치는 영향을 줄이려는 보다 광범위한 흐름을 반영합니다.

북미의 부식 방지 포장 시장은 2025년 28.5%의 점유율을 차지했습니다. 이 지역의 성장은 활발한 산업 활동과 공급망을 통한 금속 제품의 지속적인 유통으로 인해 보호 포장 솔루션에 대한 수요가 증가하고 있습니다. 인프라 개발, 물류 역량 및 첨단 보관 시스템에 대한 투자가 시장 확대를 뒷받침하고 있습니다. 또한, 제품 품질, 자재 손실 감소 및 안전한 운송에 대한 규제에 대한 강조는 지역 전체에서 첨단 포장 기술의 채택을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기술별(2022-2035년)

제6장 시장 추산 및 예측 : 제품 형태별(2022-2035년)

제7장 시장 추산 및 예측 : 기재별(2022-2035년)

제8장 시장 추산 및 예측 : 최종 사용자 용도별(2022-2035년)

제9장 시장 추산 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Anti-Corrosion Packaging Market was valued at USD 1.4 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 2.5 billion by 2035.

Rising production volumes across manufacturing sectors are driving demand for effective corrosion prevention solutions that protect metal components during storage and transit. As global logistics networks continue to expand, the need for packaging that safeguards against environmental exposure, including moisture and oxidation, is becoming increasingly critical. Industries are placing greater emphasis on minimizing product damage, lowering operational costs, and maintaining durability standards, which is accelerating the adoption of advanced packaging technologies. Continuous improvements in protective materials and packaging efficiency are further enhancing product reliability, making anti-corrosion solutions an essential component of modern industrial supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 6.2% |

The anti-corrosion packaging market is further supported by the growing production and distribution of metal components, machinery, and electronic equipment that require reliable protection against degradation. The expansion of global trade networks has increased the exposure of goods to varying environmental conditions, raising the risk of corrosion during transit and storage. This has led to higher demand for advanced protective packaging solutions designed to maintain product integrity and extend lifespan, particularly across industries with complex logistics requirements.

The hybrid and multi-layer systems segment is expected to register a CAGR of 7.2% through 2035. These packaging solutions offer enhanced protection against environmental factors and are well-suited for demanding logistics conditions. Their ability to provide consistent performance under varying conditions has made them increasingly preferred across industries requiring high durability standards, supporting their growing adoption.

The papers and paperboards segment is projected to grow at a CAGR of 8.7% during 2026-2035. This growth is driven by increasing industry focus on lightweight, recyclable, and environmentally responsible packaging solutions. Paper-based anti-corrosion materials are gaining traction due to their effective protection capabilities and alignment with sustainability goals. Their growing acceptance reflects a broader shift toward reducing environmental impact while maintaining performance standards.

North America Anti-Corrosion Packaging Market accounted for 28.5% share in 2025. Growth in the region is driven by strong industrial activity and the continuous movement of metal goods across supply chains, which increases the demand for protective packaging solutions. Investments in infrastructure development, logistics capabilities, and advanced storage systems are supporting market expansion. Additionally, regulatory emphasis on product quality, reduced material loss, and safe transportation is reinforcing the adoption of advanced anti-corrosion packaging technologies across the region.

Key companies operating in the Anti-Corrosion Packaging Market include Cortec Corporation, 3M Company, NTIC (Northern Technologies International Corporation), Zerust (NTIC brand), Daubert Cromwell Inc., Rust-X (Daubert VCI), Branopac GmbH, Armor Protective Packaging, MetPro Group, Aicello Corporation, Oji F-Tex Co. Ltd., Transilwrap Company Inc., Protective Packaging Corporation, Haver Plastics, and Green Packaging Inc. Companies in the Anti-Corrosion Packaging Market are strengthening their competitive position by focusing on innovation in material technology and product performance. They are investing in advanced barrier solutions and multi-layer packaging systems to enhance durability and protection efficiency. Sustainability is becoming a key priority, with increased development of recyclable and environmentally friendly materials. Strategic partnerships and global distribution expansion are helping companies improve market reach and customer accessibility. Businesses are also emphasizing customization to meet specific industry requirements, enabling tailored solutions for different applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology trends

- 2.2.2 Product format trends

- 2.2.3 Base material trends

- 2.2.4 End-user application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising industrial and manufacturing activity across automotive, metals, and heavy machinery

- 3.2.1.2 Expansion of global supply chains and long-distance material movement

- 3.2.1.3 Growth in electronics and semiconductor shipments requiring corrosion-safe handling

- 3.2.1.4 Rising focus on asset protection and reduction of maintenance costs in industrial sectors

- 3.2.1.5 Increasing regulatory emphasis on reducing material waste and product rejection rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of specialized anti-corrosion materials

- 3.2.2.2 Dependence on limited suppliers of corrosion-inhibiting chemicals

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of export-oriented manufacturing in emerging markets

- 3.2.3.2 Growing adoption of advanced VCI chemistries and multi-layer barrier technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 VCI (volatile corrosion inhibitor)

- 5.3 Non-VCI barrier

- 5.4 Desiccant-based

- 5.5 Hybrid / multi-layer systems

Chapter 6 Market Estimates and Forecast, By Product Format, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Films

- 6.3 Bags & pouches

- 6.4 Foils

- 6.5 Papers & paperboards

- 6.6 Emitters & devices

Chapter 7 Market Estimates and Forecast, By Base Material, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Polyethylene (PE)

- 7.3 Polypropylene (PP)

- 7.4 Aluminum / metal foil

- 7.5 Paper

- 7.6 Bio-based polymers

Chapter 8 Market Estimates and Forecast, By End-User Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Automotive manufacturing

- 8.3 Aerospace & defense

- 8.4 Electronics manufacturing

- 8.5 Heavy machinery & equipment

- 8.6 Metal fabrication & processing

- 8.7 Construction materials

- 8.8 Medical devices & instruments

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Cortec Corporation

- 10.1.2 Daubert Cromwell Inc.

- 10.1.3 Branopac GmbH

- 10.1.4 Armor Protective Packaging

- 10.1.5 Rust-X (Daubert VCI)

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 NTIC (Northern Technologies International Corporation)

- 10.2.1.2 Zerust (NTIC brand)

- 10.2.1.3 Transilwrap Company Inc.

- 10.2.1.4 Protective Packaging Corporation

- 10.2.1.5 3M Company

- 10.2.2 Asia Pacific

- 10.2.2.1 Aicello Corporation

- 10.2.2.2 Oji F-Tex Co. Ltd.

- 10.2.2.3 Green Packaging Inc.

- 10.2.3 Europe

- 10.2.3.1 MetPro Group

- 10.2.3.2 Haver Plastics

- 10.2.1 North America