|

시장보고서

상품코드

2038351

방탄복 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Body Armor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

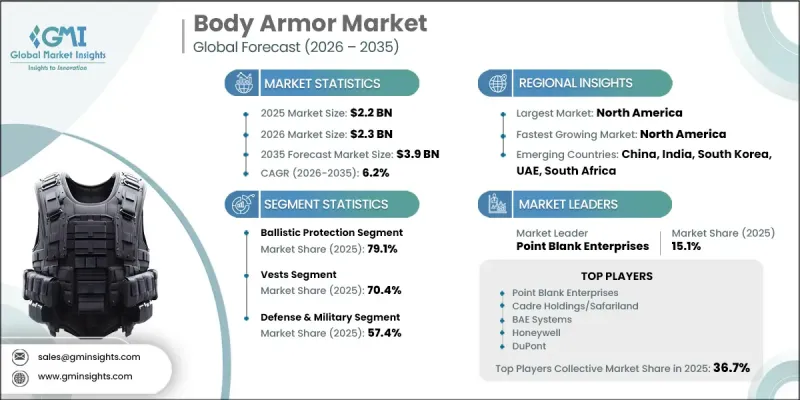

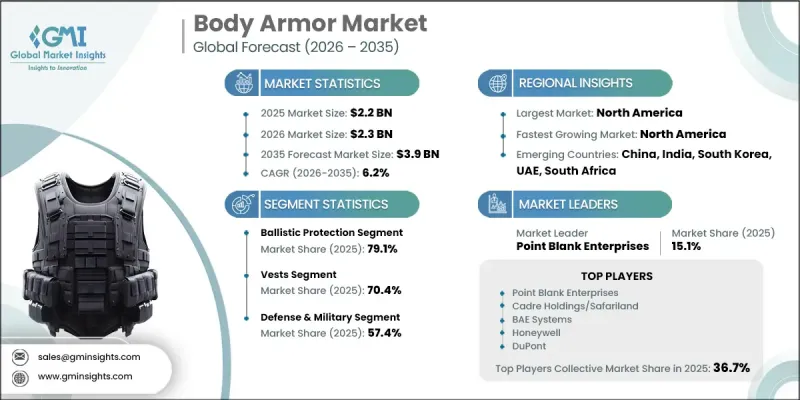

세계의 방탄복 시장은 2025년에 22억 달러로 평가되었고, CAGR 6.2%로 성장할 전망이며, 2035년까지 39억 달러에 이를 것으로 추정되고 있습니다.

세계 국방 및 치안 부대에서 인원의 안전과 작전 효율성에 대한 관심이 높아짐에 따라 시장은 계속 확대되고 있습니다. 군 조직 내 현대화 노력이 진행됨에 따라 기동성과 내구성을 높이기 위해 경량화를 유지하면서 더 높은 방탄 성능을 발휘하는 첨단 보호 장비의 도입이 촉진되고 있습니다. 테러 위험과 범죄 활동 증가 등 세계 안보에 대한 우려가 높아지면서 개인용 보호 장비에 대한 수요가 더욱 증가하고 있습니다. 법 집행 기관은 총기나 칼에 의한 위협으로부터 자신을 보호하기 위해 직원들에게 첨단 보호 솔루션을 장착하는 경우가 증가하고 있습니다. 동시에 일반 시민들의 개인 안전에 대한 인식이 높아진 것도 고위험 환경에서의 채용 확대에 기여하고 있습니다. 폭력 사건과 치안 위협의 빈번한 발생은 신뢰할 수 있는 보호 시스템의 중요성을 더욱 강조하고 있습니다. 재료 과학의 지속적인 혁신은 더 가볍고, 더 튼튼하며, 더 편안한 보호 솔루션의 개발을 가능하게 하여 사용 편의성과 보급률을 향상시키고 있습니다. 적절한 착용감, 인체공학적 디자인, 전신을 감싸는 구조는 제품의 효과와 시장 수용도에 영향을 미치는 중요한 요소로, 각 제조업체는 용도에 관계없이 사용자 맞춤화와 사용자 편의성 향상에 초점을 맞추었습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 22억 달러 |

| 예측 시장 규모 | 39억 달러 |

| CAGR | 6.2% |

2025년 기준 방탄 보호 부문은 시장 점유율의 79.1%를 차지했습니다. 이 부문은 총알과 고충격 투사체로부터 자신을 보호하는 데 필수적인 역할을 하기 때문에 꾸준한 수요를 유지하고 있습니다. 고위험 상황이 자주 발생하는 군사 및 법 집행 기관에서 널리 도입되고 있습니다. 이 부문의 성장은 경량 복합소재의 발전, 구조적 강도의 향상, 그리고 이동성 저하 없이 장시간 착용할 수 있는 착용자의 편안함 향상에 힘입어 성장세를 보이고 있습니다.

2025년, 베스트 부문은 70.4%의 점유율을 차지했습니다. 이는 중요한 상체를 보호하기 위한 광범위한 활용과 다양한 작전 환경에 대한 적응성 때문입니다. 이러한 보호 시스템은 국방 및 보안 요원들이 널리 사용하고 있습니다. 모듈식 구성, 인체공학적 디자인, 첨단 방탄 소재의 지속적인 개선으로 성능, 편안함, 전반적인 사용 편의성을 향상시켜 최종 사용자 그룹 전체에서 지속적인 수요를 창출하고 있습니다.

북미의 방탄복 시장은 2025년 35% 점유율을 차지했습니다. 이는 막대한 국방비, 첨단 제조 능력, 차세대 보호 기술의 지속적인 통합에 힘입은 것입니다. 군인과 법 집행관들의 안전을 향상시키기 위한 지속적인 투자와 보호 장비의 기술 발전으로 이 지역 시장 확대는 더욱 가속화될 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 방호 레벨별(2022-2035년)

제6장 시장 추산 및 예측 : 제품 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제8장 시장 추산 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

AJY 26.06.11The Global Body Armor Market was valued at USD 2.2 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 3.9 billion by 2035.

The market is experiencing expansion driven by increasing emphasis on personnel safety and operational effectiveness across defense and security forces worldwide. Growing modernization initiatives within military organizations are encouraging the adoption of advanced protective gear that delivers higher ballistic resistance while maintaining reduced weight for improved mobility and endurance. Rising global security concerns, including terrorism risks and increasing criminal activities, are further intensifying demand for personal protection equipment. Law enforcement agencies are increasingly equipping personnel with advanced protective solutions to safeguard against firearm and edged-weapon threats. At the same time, awareness among civilians regarding personal safety has contributed to growing adoption in high-risk environments. The rising frequency of violent incidents and security threats has reinforced the importance of reliable protective systems. Continuous innovation in materials science has enabled the development of lighter, stronger, and more comfortable protective solutions, improving usability and adoption rates. Proper fit, ergonomic design, and full-body coverage remain critical factors influencing product effectiveness and market acceptance, prompting manufacturers to focus on customization and improved user comfort across applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 6.2% |

The ballistic protection segment accounted for 79.1% share in 2025. This segment maintains strong demand due to its essential role in protecting against bullets and high-impact projectiles. It is widely deployed across military and law enforcement applications where high-risk exposure is common. Growth in this segment is supported by advancements in lightweight composites, improved structural strength, and enhanced wearer comfort that allow extended use without compromising mobility.

The vest segment represented 70.4% share in 2025, attributed to widespread use in protecting critical upper-body regions and its adaptability across multiple operational environments. These protective systems are extensively utilized by defense and security personnel. Continuous improvements in modular configurations, ergonomic design, and advanced ballistic materials are enhancing performance, comfort, and overall usability, supporting sustained demand across end-user groups.

North America Body Armor Market accounted for 35% share in 2025 supported by substantial defense spending, advanced manufacturing capabilities, and ongoing integration of next-generation protective technologies. Continuous investments in improving soldier and law enforcement safety, along with technological advancements in protective equipment, are expected to further strengthen regional market expansion.

Key companies operating in the Global Body Armor Industry include DuPont de Nemours Inc., Safariland LLC, BAE Systems, Teijin Limited, Honeywell International Inc., 3M Company, and Point Blank Enterprises. Companies in the Body Armor Market are focusing on advanced material innovation to improve protection levels while reducing weight and enhancing flexibility. Strong investments in research and development are enabling the creation of next-generation composites with superior ballistic resistance and durability. Manufacturers are increasingly forming strategic partnerships with defense agencies and law enforcement organizations to ensure product customization and long-term supply contracts. Expansion of production capacities and adoption of automated manufacturing processes are helping improve efficiency and scalability. Firms are also prioritizing ergonomic improvements and modular armor designs to enhance user comfort and adaptability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Protection level trends

- 2.2.2 Product type trends

- 2.2.3 End-user trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global military expenditure

- 3.2.1.2 Rising threats of terrorism and criminal activities

- 3.2.1.3 Technological advancements in material science

- 3.2.1.4 Increased demand for customized and gender-specific armor

- 3.2.1.5 Expansion of the civilian market for personal protection

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and affordability issues

- 3.2.2.2 Body coverage issues

- 3.2.3 Market opportunities

- 3.2.3.1 Development of next-generation lightweight armor materials

- 3.2.3.2 Increasing adoption by law enforcement and homeland security agencies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Defense budget analysis

- 3.9 Global defense spending trends

- 3.10 Regional defense budget allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Pricing Analysis (Driven by Primary Research)

- 3.11.1 Historical Price Trend Analysis

- 3.11.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.12 Trade Data Analysis (Based on Paid Database)

- 3.12.1 Import/Export Volume & Value Trends

- 3.12.2 Key Trade Corridors & Tariff Impact

- 3.13 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.13.1 AI-Driven Disruption of Existing Business Models

- 3.13.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13.3 Risks, Limitations & Regulatory Considerations

- 3.14 Capacity & Production Landscape (Driven by Primary Research)

- 3.14.1 Production Capacity by Region & Key Producer

- 3.14.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia-Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Protection Level, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Ballistic protection

- 5.2.1 Level IIA

- 5.2.2 Level II

- 5.2.3 Level IIIA

- 5.2.4 Level III

- 5.2.5 Level IV

- 5.3 Stab & spike protection

- 5.3.1 Stab-resistant armor

- 5.3.2 Spike-resistant armor

- 5.3.3 Multi-threat protection (combined ballistic/stab/spike)

Chapter 6 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Vests

- 6.2.1 Covert/concealable vests

- 6.2.2 Overt/tactical vests

- 6.2.3 Plate carriers

- 6.2.4 Modular armor systems

- 6.3 Helmets

- 6.3.1 Combat helmets

- 6.3.2 Riot helmets

- 6.3.3 Ballistic face shields

- 6.4 Shields

- 6.4.1 Handheld ballistic shields

- 6.4.2 Breaching shields

- 6.5 Accessories & attachments

- 6.5.1 Groin protectors

- 6.5.2 Neck guards

- 6.5.3 Shoulder & deltoid protection

- 6.5.4 Ballistic inserts & soft armor panels

Chapter 7 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Defense & military

- 7.2.1 Army

- 7.2.2 Navy

- 7.2.3 Air force

- 7.2.4 Marines

- 7.2.5 Special operations forces

- 7.3 Law enforcement & security

- 7.3.1 Police departments

- 7.3.2 Correctional officers

- 7.3.3 Private security firms

- 7.3.4 Border patrol & customs

- 7.4 Civilian

- 7.4.1 Personal protection

- 7.4.2 Shooting sports & training

- 7.4.3 Journalists & NGO workers

- 7.4.4 High-risk professionals

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Point Blank Enterprises

- 9.1.2 BAE Systems

- 9.1.3 Safariland LLC

- 9.1.4 Honeywell International Inc.

- 9.1.5 DuPont de Nemours Inc.

- 9.1.6 3M Company

- 9.1.7 Teijin Limited

- 9.2 Regional Champions

- 9.2.1 U.S. Armor Corporation

- 9.2.2 Armor Express

- 9.2.3 AR500 Armor

- 9.2.4 Vestguard (UK)

- 9.2.5 Protection Group Danmark (Europe)

- 9.2.6 Indian Armour Systems

- 9.3 Emerging Players

- 9.3.1 Safe Life Defense

- 9.3.2 BulletSafe

- 9.3.3 Spartan Armor Systems

- 9.3.4 Hoplite Armor

- 9.3.5 RMA Armament

- 9.3.6 DFNDR Armor