|

시장보고서

상품코드

2038375

시험, 검사 및 인증(TIC) 서비스 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Testing, Inspection and Certification (TIC) Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

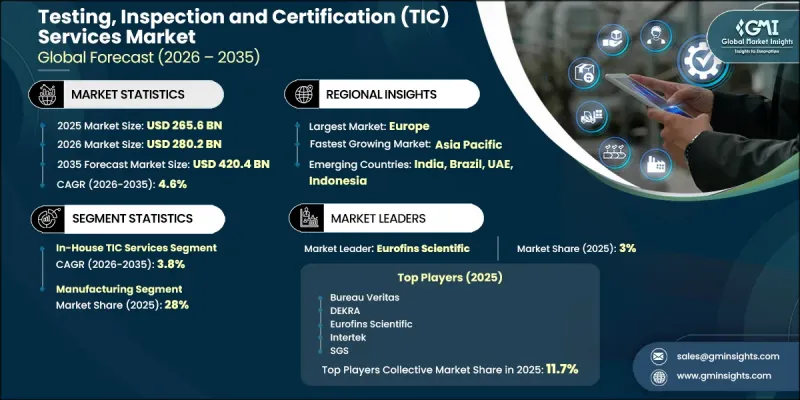

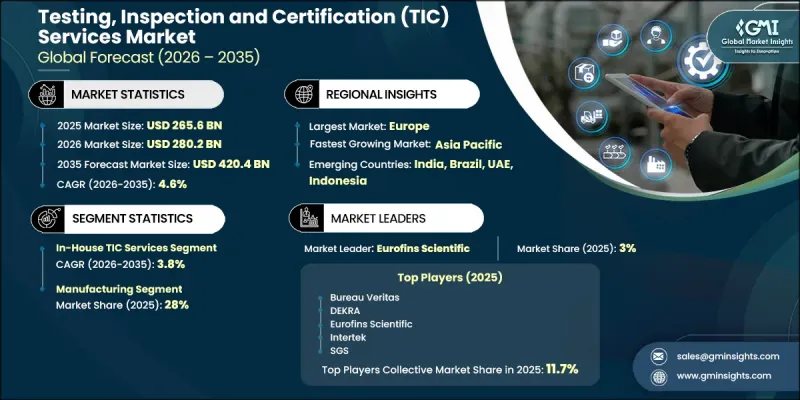

세계의 시험, 검사 및 인증(TIC) 서비스 시장은 2025년에 2,656억 달러로 평가되었고 CAGR 4.6%로 성장하여 2035년까지 4,204억 달러에 이를 것으로 추정되고 있습니다.

이 시장의 성장은 제조, 에너지, 운송, 소비재 등 주요 산업에서 제품 안전, 규제 준수, 품질 보증에 대한 전 세계적인 관심 증가에 힘입은 바 큽니다. TIC 서비스는 제품이 세계 공급망에 진입하기 전에 국내외 규제 요건을 충족하는지 확인하는 데 중요한 역할을 합니다. 무역의 세계화가 진행됨에 따라 표준화된 인증 및 독립적인 검증 프로세스의 필요성이 더욱 커지고 있습니다. 업계 전반에 걸쳐 규제가 복잡해지고 컴플라이언스 기준이 강화됨에 따라 조직은 공정한 평가와 문서화를 위해 제3자 TIC 제공업체에 대한 의존도가 높아지고 있습니다. 또한, 지속가능성 요건과 환경 규제의 확대도 시험 및 인증 건수 증가에 기여하고 있습니다. 위험 감소, 업무 투명성, 제품 신뢰성에 대한 중요성이 높아진 것도 수요를 더욱 촉진하고 있습니다. 지속적인 산업화, 기술 발전, 국경 간 무역 활동의 확대가 결합되어 TIC 서비스 산업 전체의 장기적인 성장 모멘텀을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 2,656억 달러 |

| 예측 규모 | 4,204억 달러 |

| CAGR | 4.6% |

2025년에는 시험 서비스 부문이 51%의 점유율을 차지했습니다. 이 부문은 정확한 제품 검증과 컴플라이언스 확인이 필수적인 제조업, 의료 산업, 소비재 산업에서 폭넓게 활용되고 있습니다. 시험 프로세스는 다양한 응용 분야에서 정확성, 일관성 및 필요한 표준 준수를 보장하기 위해 규제 당국에 의해 일상적으로 모니터링 및 검증되고 있습니다.

사내 TIC 서비스 부문은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 3.8%를 나타낼 것으로 예측됩니다. 많은 조직은 품질 보증 프로세스에 대한 관리를 강화하고, 데이터 기밀성을 높이고, 리드 타임을 단축하기 위해 사내 TIC 역량을 우선순위에 두고 있습니다. 사내 시험 인프라에 투자하는 기업은 일반적으로 고급 실험실, 전문 장비, 숙련된 기술자에게 자원을 배분합니다. 제약, 항공우주, 자동차 제조 등 엄격한 규제 프레임워크 하에서 사업을 영위하는 업계에서는 진화하는 안전 및 품질 기준을 충족하기 위해 내부적으로 컴플라이언스 대응 역량을 지속적으로 확장하고 있습니다.

미국의 시험, 검사 및 인증(TIC) 서비스 시장은 2025년 651억 달러 규모에 달했습니다. 이러한 견고한 수요는 제품의 신뢰성, 규제 준수 및 운영 효율성을 보장하기 위해 TIC 서비스가 필수적인 제조업에 의해 주도되고 있습니다. 전자, 자동차, 기계 등의 산업은 국내외 표준을 충족하기 위해 인증 및 검사 프로세스에 크게 의존하고 있습니다. 정부 기관의 규제 감독을 통한 컴플라이언스 요건이 지속적으로 강화되고 있으며, 이는 미국 전역의 TIC 서비스에 대한 지속적인 수요를 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 서비스별, 2022-2035년

제6장 시장 추산 및 예측 : 조달 형태별, 2022-2035년

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.05.29The Global Testing, Inspection and Certification (TIC) Services Market was valued at USD 265.6 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 420.4 billion by 2035.

The market growth is strongly supported by rising global emphasis on product safety, regulatory compliance, and quality assurance across key industries such as manufacturing, energy, transportation, and consumer goods. TIC services play a critical role in ensuring that products meet domestic and international regulatory requirements before entering global supply chains. Increasing globalization of trade has further strengthened the need for standardized certification and independent verification processes. Growing regulatory complexity and tightening compliance norms across industries are pushing organizations to rely more on third-party TIC providers for unbiased assessment and documentation. In addition, expanding sustainability requirements and environmental regulations are contributing to higher testing and certification volumes. The rising importance of risk mitigation, operational transparency, and product reliability is further reinforcing demand. Continuous industrialization, technological advancement, and expansion of cross-border trade activities are collectively sustaining long-term growth momentum across the TIC services industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $265.6 Billion |

| Forecast Value | $420.4 Billion |

| CAGR | 4.6% |

The testing services segment accounted for 51% share in 2025. This segment remains widely used across manufacturing, healthcare, and consumer goods industries, where accurate product validation and compliance verification are essential. Testing processes are routinely monitored and validated by regulatory bodies to ensure accuracy, consistency, and adherence to required standards across various applications.

The in-house TIC services segment is expected to grow at a CAGR of 3.8% from 2026 to 2035. Many organizations prefer internal TIC capabilities to maintain greater control over quality assurance processes, improve data confidentiality, and reduce turnaround time. Companies investing in in-house testing infrastructure typically allocate resources toward advanced laboratories, specialized equipment, and skilled technical personnel. Industries operating under strict regulatory frameworks, including pharmaceuticals, aerospace, and automotive manufacturing, continue to expand internal compliance capabilities to meet evolving safety and quality standards.

U.S. Testing, Inspection and Certification (TIC) Services Market generated USD 65.1 billion in 2025. Strong demand is driven by the manufacturing sector, where TIC services are essential for ensuring product reliability, regulatory compliance, and operational efficiency. Industries such as electronics, automotive, and machinery rely heavily on certification and inspection processes to meet domestic and international standards. Regulatory oversight by government bodies continues to reinforce compliance requirements, supporting sustained demand for TIC services across the country.

Major players operating in the Global Testing, Inspection and Certification (TIC) Services Industry include Bureau Veritas, SGS, Intertek, TUV SUD, TUV Rheinland, DNV, Eurofins Scientific, UL Solutions, Applus+, and DEKRA. Companies in the Global Testing, Inspection And Certification (TIC) Services are focusing on expanding their global service networks to strengthen client accessibility and operational reach. Strategic investments in digital inspection technologies, automation, and data analytics are enhancing efficiency and accuracy in service delivery. Firms are also increasing laboratory capacity and upgrading testing infrastructure to meet rising demand across industries. Mergers and acquisitions are being actively pursued to broaden service portfolios and strengthen geographic presence. Additionally, organizations are prioritizing industry-specific certification expertise to cater to complex regulatory requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Sourcing

- 2.2.4 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing enforcement of stringent product safety and quality regulations

- 3.2.1.2 Rising industrialization and manufacturing output in emerging economies

- 3.2.1.3 Increased consumer awareness and demand for certified, sustainable products

- 3.2.1.4 Adoption of digital and remote inspection technologies (AI, IoT, blockchain)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operational and service costs for complex testing environments

- 3.2.2.2 Variability in certification standards across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of TIC services in renewable energy, EVs, and green technologies

- 3.2.3.2 Growing demand for cybersecurity and digital system certification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. OSHA Nationally Recognized Testing Laboratory (NRTL) program requirements

- 3.4.1.2 NIST and ANSI laboratory accreditation and metrology standards

- 3.4.1.3 EPA and FDA regulatory compliance frameworks for environmental and life sciences testing

- 3.4.1.4 CPSC safety standards and FCC electromagnetic compatibility (EMC) regulations

- 3.4.1.5 Canada Standards Council (SCC) accreditation and Health Canada product safety rules

- 3.4.2 Europe

- 3.4.2.1 EU Regulation (EC) No 765/2008 for accreditation and market surveillance

- 3.4.2.2 CE Marking directives (Machinery, Low Voltage, EMC, and Medical Devices)

- 3.4.2.3 EU Corporate Sustainability Reporting Directive (CSRD) and ESG verification mandates

- 3.4.2.4 REACH and RoHS chemical substances and hazardous material restrictions

- 3.4.2.5 EA (European Accreditation) multilateral agreements for cross-border laboratory validity

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC) and CNAS laboratory accreditation rules

- 3.4.3.2 Japan Industrial Standards (JIS) and PSE mark for electrical appliance safety

- 3.4.3.3 India BIS (Bureau of Indian Standards) and NABL accreditation frameworks

- 3.4.3.4 ASEAN harmonized regulatory regimes for cosmetics, electronics, and pharmaceuticals

- 3.4.3.5 Australia and New Zealand (AS/NZS) joint standards and safety certification codes

- 3.4.4 Latin America

- 3.4.4.1 Brazil Inmetro (National Institute of Metrology, Quality and Technology) certification rules

- 3.4.4.2 Mexico NOM (Normas Oficiales Mexicanas) and EMA accreditation standards

- 3.4.4.3 Argentina IRAM safety certification and OAA laboratory accreditation

- 3.4.4.4 Mercosur regional standardization agreements for industrial and consumer goods

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO) and G-Mark certification requirements

- 3.4.5.2 Saudi Arabia SASO and SABER platform conformity assessment regulations

- 3.4.5.3 UAE MoIAT (Ministry of Industry and Advanced Technology) product safety schemes

- 3.4.5.4 South Africa SANAS accreditation and SABS technical quality standards

- 3.4.5.5 African Organization for Standardisation (ARSO) intra-continental trade frameworks

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by primary research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Impact of AI and Generative AI on the Market

- 3.10.1 AI Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.10.3 Risks Limitations and Regulatory Considerations

- 3.11 Sustainability & environmental aspects

- 3.11.1 Carbon Footprint Assessment

- 3.11.2 Circular Economy Integration

- 3.11.3 E-Waste Management Requirements

- 3.11.4 Green Manufacturing Initiatives

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Testing Services

- 5.2.1 Electromagnetic compatibility testing

- 5.2.2 Electrical safety and performance testing

- 5.2.3 Mechanical and materials testing

- 5.2.4 Others

- 5.3 Inspection Services

- 5.3.1 Pre-shipment and consignment inspection

- 5.3.2 Industrial site and equipment inspection

- 5.3.3 Construction and infrastructure inspection

- 5.3.4 Others

- 5.4 Certification Services

- 5.4.1 Product certification

- 5.4.2 Management system certification

- 5.4.3 Personnel certification

- 5.4.4 Others

- 5.5 Calibration Services

- 5.5.1 Instrument calibration

- 5.5.2 Metrology and measurement standards

- 5.5.3 Others

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Sourcing, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 In-House TIC Services

- 6.2.1 Internal testing and quality control laboratories

- 6.2.2 Captive inspection and certification departments

- 6.2.3 Corporate R&D and compliance testing centers

- 6.2.4 Others

- 6.3 Outsourced TIC Services

- 6.3.1 Independent third-party TIC providers

- 6.3.2 Contract-based testing laboratories

- 6.3.3 External inspection and certification bodies

- 6.3.4 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Manufacturing

- 7.2.1 Industrial machinery and equipment testing

- 7.2.2 Quality control and factory audits

- 7.2.3 Supply chain and component verification

- 7.3 Energy and Utilities

- 7.3.1 Renewable energy system testing

- 7.3.2 Smart grid and battery certification

- 7.3.3 Nuclear plant safety inspection

- 7.3.4 Oil and gas asset integrity assessments

- 7.4 Food and Beverages

- 7.4.1 Food safety and hygiene testing

- 7.4.2 Packaging and labeling compliance

- 7.4.3 Supply chain traceability and origin verification

- 7.4.4 Organic and sustainability certifications

- 7.5 Automotive

- 7.5.1 Electric vehicle testing and certification

- 7.5.2 Autonomous vehicle validation

- 7.5.3 Connected car cybersecurity testing

- 7.5.4 Vehicle inspection and homologation

- 7.6 Chemicals

- 7.6.1 Chemical composition and purity testing

- 7.6.2 Hazardous material certification

- 7.6.3 Environmental and regulatory compliance audits

- 7.7 Construction and Infrastructure

- 7.7.1 Building materials testing

- 7.7.2 Structural integrity inspections

- 7.7.3 Green building and sustainability certification

- 7.8 Healthcare and Life Sciences

- 7.8.1 Biocompatibility and sterilization testing

- 7.8.2 Pharmaceutical and clinical trial validation

- 7.8.3 Medical device and software validation

- 7.9 Aerospace and Defense

- 7.9.1 Aviation component certification

- 7.9.2 Defense system and military standards testing

- 7.9.3 Space system qualification

- 7.10 Consumer Products

- 7.10.1 Electrical appliance safety testing

- 7.10.2 Toy, textile, and cosmetic certification

- 7.10.3 Consumer protection and quality assurance

- 7.11 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Bureau Veritas

- 9.1.2 DEKRA

- 9.1.3 DNV

- 9.1.4 Eurofins Scientific

- 9.1.5 Intertek

- 9.1.6 SGS

- 9.1.7 TUV Rheinland

- 9.1.8 TUV SUD

- 9.2 Regional Champions

- 9.2.1 APAVE

- 9.2.2 BSI

- 9.2.3 Centre Testing International

- 9.2.4 CCIC

- 9.2.5 CSA

- 9.2.6 Lloyd's Register

- 9.2.7 SOCOTEC

- 9.2.8 UL Solutions

- 9.3 Emerging Players & Specialists

- 9.3.1 ALS

- 9.3.2 Applus+ Services

- 9.3.3 Element Materials Technology Group

- 9.3.4 Kiwa

- 9.3.5 NSF International

- 9.3.6 QIMA

- 9.3.7 RINA