|

시장보고서

상품코드

2038413

웨어러블 심장 디바이스 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Wearable Cardiac Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

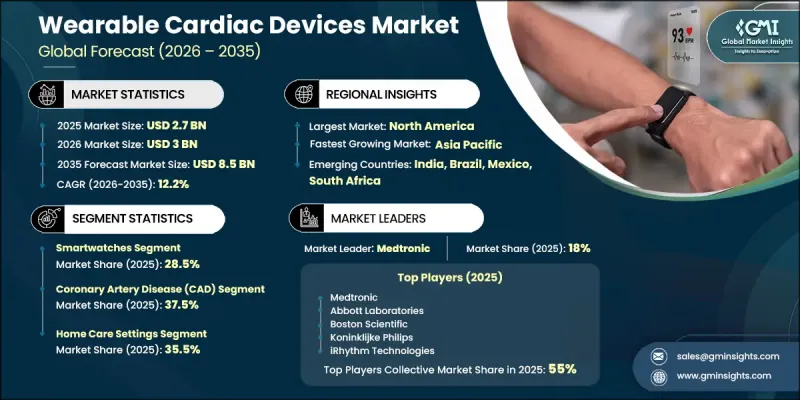

세계의 웨어러블 심장 디바이스 시장은 2025년에 27억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 12.2%로 성장하여 85억 달러에 이를 것으로 추정되고 있습니다.

이러한 시장 확대는 전 세계 심혈관 질환 부담 증가, 웨어러블 건강 모니터링 기술의 지속적인 발전, 저침습 및 비침습적 진단 솔루션에 대한 소비자 선호도 증가에 힘입어 성장세를 보이고 있습니다. 건강에 대한 인식이 높아지고 예방의학으로의 전환이 가속화되고 있는 것도 전체 환자층에 대한 도입을 촉진하고 있습니다. 웨어러블 심장 디바이스는 임상 환경 밖에서 심장 관련 질환을 지속적으로 추적, 진단, 관리할 수 있도록 설계된 첨단 의료 시스템입니다. 이 디바이스는 심전도 기능, 바이오 센서, 무선 통신 시스템 및 디지털 신호 처리 기술을 통합하여 심박수, 심박수 및 기타 심혈관 지표를 실시간으로 모니터링합니다. 이를 통해 부정맥, 심방세동, 허혈성 이상, 심부전 등의 병태를 조기에 파악하여 적시에 임상적 개입을 할 수 있습니다. 지속적인 모니터링은 맞춤 치료 접근법을 지원하고, 재입원을 줄이며, 환자의 결과와 삶의 질을 향상시킵니다. 환자와 의료진이 불편함과 시술에 따른 위험을 줄이면서 진단 효율을 높이고 비수술적이고 장기적인 모니터링 수단을 점점 더 선호함에 따라 저침습적 심장 모니터링 솔루션에 대한 수요가 증가함에 따라 시장 성장에 더욱 박차를 가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 27억 달러 |

| 예측 규모 | 85억 달러 |

| CAGR | 12.2% |

2025년에는 스마트 워치 부문이 28.5%의 점유율을 차지했습니다. 이 분야는 직관적인 인터페이스와 사용 편의성으로 인해 널리 보급되고 있으며, 지속적인 임상적 모니터링 없이도 개인이 자율적으로 심장 건강 상태를 추적할 수 있게 해줍니다. 이러한 디바이스에는 점점 더 많은 첨단 센서 시스템과 인공지능(AI) 기반 분석 기능이 탑재되어 지속적인 실시간 모니터링을 가능하게 하고, 정보에 입각한 임상적 의사결정을 지원합니다. 또한 고급 알고리즘 기능을 통해 심방세동을 포함한 부정맥의 조기 발견을 촉진하고, 적시에 경고 및 개입을 통해 심각한 심혈관 합병증 발생 위험을 줄이는 데 도움을 주고 있습니다.

관상동맥 질환 부문은 2025년 37.5%의 점유율을 차지하고, 2035년까지 33억 달러에 달할 것으로 예측됩니다. 관상동맥 질환은 여전히 전 세계적으로 가장 흔한 심혈관 질환 중 하나이며, 심장 관련 사망과 이환율의 상당 부분을 차지합니다. 비만, 운동 부족, 불건강한 식습관, 흡연과 같은 위험 요인 증가는 질병 부담 증가에 기여하고 있습니다. 이러한 위험 요인이 계속 증가함에 따라 지속적인 심장 모니터링 솔루션에 대한 수요가 증가하고 있으며, 이에 따라 조기 발견 및 지속적인 질병 관리를 위한 웨어러블 심장 디바이스의 도입이 가속화되고 있습니다.

2025년 북미 웨어러블 심장 디바이스 시장은 40.4%의 점유율을 차지했습니다. 이 지역은 특히 미국에서 심혈관 질환의 발병률이 높은 지역으로 확고한 입지를 구축하고 있습니다. 잘 정비된 의료 시스템, 첨단 의료 인프라, 그리고 디지털 헬스 기술의 강력한 통합은 시장 성장을 더욱 촉진하고 있습니다. 현대식 의료시설의 광범위한 보급, 유리한 보험 환급 제도, 환자의 인식이 높아지면서 지역 전체에서 조기 진단, 원격 모니터링 및 장기적인 질병 관리를 위한 웨어러블 심장 디바이스의 도입이 촉진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022-2035년

제6장 시장 추산 및 예측 : 용도별, 2022-2035년

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

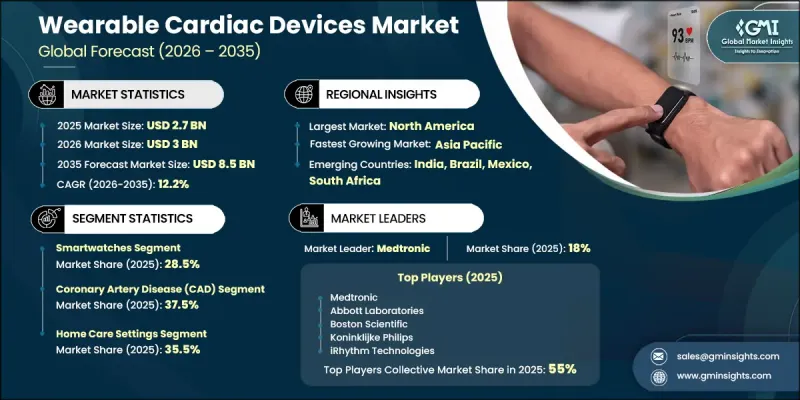

JHS 26.05.29The Global Wearable Cardiac Devices Market was valued at USD 2.7 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 8.5 billion by 2035.

The market expansion is driven by a rising global burden of cardiovascular diseases, continuous advancements in wearable health monitoring technologies, and increasing consumer preference for minimally invasive and non-invasive diagnostic solutions. Growing health awareness and a stronger shift toward preventive healthcare are also reinforcing adoption across patient populations. Wearable cardiac devices are advanced medical systems designed to continuously track, diagnose, and manage heart-related conditions outside clinical environments. These devices integrate electrocardiography capabilities, biosensors, wireless communication systems, and digital signal processing technologies to monitor heart rhythm, heart rate, and other cardiovascular indicators in real time. They enable early identification of conditions such as arrhythmias, atrial fibrillation, ischemic abnormalities, and heart failure, allowing timely clinical intervention. Continuous monitoring supports personalized treatment approaches, reduces hospital readmissions, and improves patient outcomes and quality of life. The rising demand for minimally invasive cardiac monitoring solutions is further strengthening market growth as patients and healthcare providers increasingly prefer non-surgical, long-duration monitoring options that reduce discomfort and procedural risks while improving diagnostic efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.7 Billion |

| Forecast Value | $8.5 Billion |

| CAGR | 12.2% |

The smartwatches segment accounted for 28.5% share in 2025. This segment is widely adopted due to its intuitive interface and ease of use, enabling individuals to independently track cardiac health without continuous clinical supervision. These devices are increasingly equipped with advanced sensor systems and artificial intelligence based analytics, which allow continuous real-time monitoring and support informed clinical decision-making. Advanced algorithmic capabilities also enhance early detection of abnormal cardiac rhythms, including atrial fibrillation, helping reduce the likelihood of severe cardiovascular complications through timely alerts and interventions.

The coronary artery disease segment held a 37.5% share in 2025 and is expected to reach USD 3.3 billion by 2035. Coronary artery disease remains one of the most prevalent cardiovascular conditions globally and is responsible for a significant proportion of heart-related mortality and morbidity. The increasing prevalence of risk factors such as obesity, sedentary lifestyles, unhealthy dietary habits, and tobacco consumption is contributing to a higher disease burden. As these risk factors continue to rise, demand for continuous cardiac monitoring solutions is increasing, thereby accelerating adoption of wearable cardiac devices for early detection and ongoing disease management.

North America Wearable Cardiac Devices Market accounted for 40.4% share in 2025. The region holds a strong position due to the high incidence of cardiovascular diseases, particularly in the U.S. A well-developed healthcare system, advanced medical infrastructure, and strong integration of digital health technologies further support market growth. Widespread availability of modern healthcare facilities, favorable reimbursement structures, and increasing patient awareness are driving the adoption of wearable cardiac devices for early diagnosis, remote monitoring, and long-term disease management across the region.

Major companies operating in the Global Wearable Cardiac Devices Industry include Medtronic, Abbott Laboratories, Koninklijke Philips, Boston Scientific, iRhythm Technologies, ZOLL Medical Corporation, VitalConnect, Cardiac Insight, CardiacSense, Qardio, Welch Allyn, Cardiac Rhythm, Integra LifeSciences, Zimmer Biomet, and Proteus Digital Health. Companies in the Wearable Cardiac Devices Market are focusing on strengthening their competitive position through continuous innovation in sensor accuracy, device miniaturization, and real-time data analytics capabilities. Significant investments in artificial intelligence and machine learning are enabling enhanced predictive diagnostics and improved patient monitoring outcomes. Firms are also expanding cloud-based connectivity features to ensure seamless data transfer between patients and healthcare providers. Strategic collaborations with hospitals, telehealth platforms, and digital health ecosystems are helping improve product integration and market reach. In addition, companies are prioritizing regulatory compliance and clinical validation to enhance product credibility.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of patients suffering from cardiovascular diseases

- 3.2.1.2 Rapid technological advancements in wearable cardiac devices

- 3.2.1.3 Growing preference of minimally invasive devices

- 3.2.1.4 Rising health consciousness and preventive care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy issues

- 3.2.2.2 Stringent regulatory policies

- 3.2.3 Market opportunities

- 3.2.3.1 Rapid expansion of home-use wearable cardiac devices

- 3.2.3.2 Integration with AI and advanced analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Continuous ECG and patch based wearable cardiac monitoring devices

- 3.5.1.2 Cloud integrated remote cardiac monitoring platforms

- 3.5.2 Emerging technologies

- 3.5.2.1 Non invasive optical and multimodal biosensing cardiac diagnostics

- 3.5.2.2 Smart, connected, and personalized wearable cardiac devices

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing analysis, 2025

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Holter monitors

- 5.3 Smartwatches

- 5.4 Patch

- 5.5 Defibrillators

- 5.6 Pulse oximeters

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease (CAD)

- 6.3 Cardiomyopathies

- 6.4 Post-myocardial infarction

- 6.5 Congenital heart diseases

- 6.6 Post-surgical cardiac care

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty centers

- 7.4 Home care settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 UK

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Boston Scientific

- 9.3 Cardiac Insight

- 9.4 CardiacSense

- 9.5 Cardiac Rhythm

- 9.6 iRhythm Technologies

- 9.7 Integra LifeSciences

- 9.8 Koninklijke Philips

- 9.9 Medtronic

- 9.10 Proteus Digital Health

- 9.11 Qardio

- 9.12 ZOLL Medical Corporation

- 9.13 Welch Allyn

- 9.14 VitalConnect

- 9.15 Zimmer Biomet