|

시장보고서

상품코드

2038445

의료기기 유통 서비스 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Medical Device Distribution Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

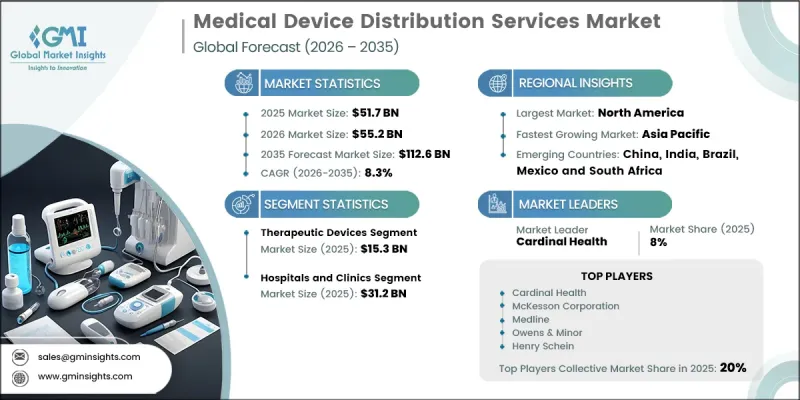

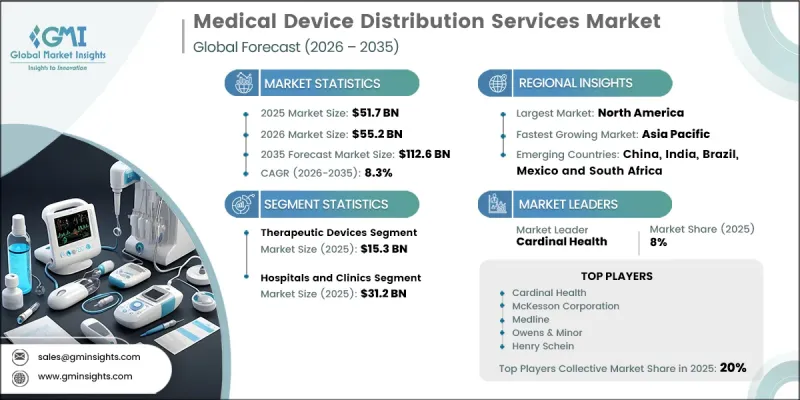

세계의 의료기기 유통 서비스 시장은 2025년에 517억 달러로 평가되었고, CAGR 8.3%로 성장할 전망이며, 2035년까지 1,126억 달러에 이를 것으로 예측됩니다.

시장 확대는 만성질환 부담 증가, 의료 혁신에 대한 투자 확대, 의료 생태계에 진입하는 의료기기의 승인 건수 증가에 의해 주도되고 있습니다. 원격 모니터링 및 홈케어 등 첨단 의료 솔루션에 대한 수요는 효율적인 유통 네트워크의 필요성을 더욱 가속화시키고 있습니다. 의료기술의 지속적인 발전으로 의료기기의 수량과 고도화가 진행되면서 전문 서비스 제공업체에 대한 의존도가 높아지고 있습니다. 민관 양측의 자금 지원 확대에 따라 진단, 치료, 모니터링 솔루션 개발이 가속화되고 있으며, 안정적인 신제품 파이프라인이 형성되고 있습니다. 공급망이 복잡해짐에 따라 컴플라이언스 요건, 물류 업무, 재고 관리 시스템 관리에 있어 유통 파트너의 존재가 필수적입니다. 제조업체와 의료 제공업체를 연결하는 그들의 역할은 점점 더 강화되고 있으며, 제품의 안정적인 공급을 지원하고 세계 시장의 지속적인 성장을 견인하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 517억 달러 |

| 예측 시장 규모 | 1,126억 달러 |

| CAGR | 8.3% |

치료용 의료기기 부문은 2025년 153억 달러 시장 규모를 기록했습니다. 이 부문에는 의료 시스템 전반의 치료, 장기 치료, 기능 지원을 위한 다양한 기술이 포함됩니다. 이러한 기기들은 다양한 의료 현장에서 널리 활용되고 있으며, 응급상황에서의 개입부터 지속적인 질병 관리에 이르기까지 매우 중요한 역할을 하고 있습니다. 이러한 제품의 유통은 엄격한 취급 요건과 규제 당국의 감독으로 인해 고도로 구조화된 공급망 프로세스가 필요합니다. 이러한 의료기기의 대부분은 더 높은 규제 분류에 속하며, 엄격한 규정 준수 기준이 요구됩니다. 따라서 유통 서비스 제공업체는 품질 및 안전 프로토콜을 준수하면서 적절한 보관, 운송 및 배송을 보장하는 데 있어 매우 중요한 역할을 담당합니다.

2025년 기준 병원 및 클리닉 부문 시장 규모는 312억 달러에 달했습니다. 의료시설은 필수 의료 장비에 대한 중단 없는 접근을 유지하고, 효율적인 의료 서비스 제공과 적시에 임상적 판단을 내릴 수 있도록 유통 서비스에 크게 의존하고 있습니다. 환자 수가 증가하고 치료 결과 중심의 치료 모델로 전환함에 따라 신뢰할 수 있는 공급망 지원의 필요성이 증가하고 있습니다. 유통업체는 의료 환경 내 제품 공급의 안정적 확보와 물류 업무의 최적화를 통해 크게 기여하고 있으며, 이는 환자 치료 서비스의 효율성과 연속성을 유지하는 데 필수적입니다.

미국의 의료기기 유통 서비스 시장은 견조한 의료비 지출과 첨단 의료 기술의 광범위한 도입에 힘입어 2025년 186억 달러에 달할 것으로 예측됩니다. 만성질환의 유병률 증가는 효율적인 유통망에 대한 수요를 더욱 부추기고 있습니다. 또한, 엄격한 규제 요건과 의료 시스템의 복잡성으로 인해 컴플라이언스, 재고 관리, 적시 배송을 관리하고 업무 효율성과 환자 치료의 연속성을 보장할 수 있는 전문 서비스 제공업체에 대한 요구가 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별(2022-2035년)

제6장 시장 추산 및 예측 : 최종 용도별(2022-2035년)

제7장 시장 추산 및 예측 : 지역별(2022-2035년)

제8장 기업 개요

AJY 26.06.11The Global Medical Device Distribution Services Market was valued at USD 51.7 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 112.6 billion by 2035.

Market expansion is driven by the rising burden of chronic conditions, increasing investments in medical innovation, and a growing number of device approvals entering the healthcare ecosystem. Demand for advanced healthcare solutions, including remote monitoring and home-based care, is further accelerating the need for efficient distribution networks. Continuous progress in medical technology is increasing the volume and sophistication of devices, which in turn is intensifying reliance on specialized service providers. Growing financial support from public and private sectors is enabling faster development of diagnostic, therapeutic, and monitoring solutions, leading to a steady pipeline of new products. As the complexity of supply chains increases, distribution partners are becoming essential in managing compliance requirements, logistics operations, and inventory systems. Their role in bridging manufacturers and healthcare providers continues to strengthen, supporting consistent product availability and driving sustained global market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $51.7 Billion |

| Forecast Value | $112.6 Billion |

| CAGR | 8.3% |

The therapeutic devices segment generated USD 15.3 billion in 2025. This segment encompasses a wide range of technologies designed for treatment, long-term care, and functional support across healthcare systems. These devices are extensively utilized in various care settings and are critical for both immediate interventions and ongoing disease management. The distribution of such products involves highly structured supply chain processes due to strict handling requirements and regulatory oversight. A large proportion of these devices falls under higher regulatory classifications, which demand rigorous compliance standards. As a result, distribution service providers play a vital role in ensuring proper storage, transportation, and delivery while maintaining adherence to quality and safety protocols.

The hospitals and clinics segment accounted for USD 31.2 billion in 2025. Healthcare facilities rely heavily on distribution services to maintain uninterrupted access to essential medical equipment, enabling efficient care delivery and timely clinical decisions. Increasing patient volumes and the transition toward outcome-focused care models are amplifying the need for reliable supply chain support. Distribution providers contribute significantly by ensuring consistent product availability and optimizing logistics operations within healthcare environments, which is critical for maintaining efficiency and continuity in patient care services.

U.S. Medical Device Distribution Services Market reached USD 18.6 billion in 2025 supported by strong healthcare expenditure and widespread adoption of advanced medical technologies. The growing prevalence of chronic health conditions is further driving demand for efficient distribution networks. Additionally, stringent regulatory requirements and the complexity of healthcare systems are increasing the need for specialized service providers that can manage compliance, inventory, and timely delivery, ensuring operational efficiency and uninterrupted patient care.

Key players operating in the Global Medical Device Distribution Services Market include McKesson Corporation, Cardinal Health, Owens & Minor, Medline, Henry Schein, Patterson Companies, Bunzl, Avantor, Alfresa Holdings Corporation, KEBOMED Europe, CAN-med Healthcare, Meditek Systems, Soquelec, Southmedic, and The Stevens Company Limited. Companies in the Medical Device Distribution Services Market are strengthening their market position through strategic investments in technology, infrastructure, and partnerships. Businesses are focusing on enhancing supply chain efficiency by adopting digital tools, automation, and advanced inventory management systems. Collaborations with manufacturers and healthcare providers are helping expand distribution networks and improve service capabilities. Firms are also investing in compliance frameworks to meet stringent regulatory standards and ensure safe handling of medical devices. Geographic expansion into emerging markets is another key strategy to capture new growth opportunities.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.1.1 Key market trends

- 2.1.2 Product trends

- 2.1.3 End use trends

- 2.1.4 Regional trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic diseases

- 3.2.1.2 Surge in investments for research and growth in medical device approvals

- 3.2.1.3 Rising demand for home healthcare and remote monitoring

- 3.2.1.4 Advancements in medical device technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Requirement for high initial capital expenditure

- 3.2.2.2 Presence of stringent regulatory compliance

- 3.2.3 Market opportunity

- 3.2.3.1 Growth in online distribution services and digital ordering system

- 3.2.3.2 Increasing public private partnership to strengthen supply chain

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Artificial intelligence (AI) and automation in supply chain

- 3.5.1.2 Internet of things (IoT) for real-time tracking

- 3.5.1.3 Digital twins for supply chain simulation

- 3.5.2 Emerging technologies

- 3.5.2.1 5G-enabled logistics and remote monitoring

- 3.5.2.2 Autonomous delivery systems

- 3.5.1 Current technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Pricing analysis, 2025 (Driven by Primary Research)

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostic devices

- 5.3 Therapeutic devices

- 5.4 Patient monitoring devices

- 5.5 Home healthcare devices

- 5.6 Other device distribution services

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals and clinics

- 6.3 Diagnostic centers

- 6.4 Ambulatory surgical centers (ASCs)

- 6.5 Long-term care facilities

- 6.6 Homecare settings

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Alfresa Holdings Corporation

- 8.2 Avantor

- 8.3 Bunzl

- 8.4 CAN-med Healthcare

- 8.5 Cardinal Health

- 8.6 Henry Schein

- 8.7 KEBOMED Europe

- 8.8 McKesson Corporation

- 8.9 Meditek Systems

- 8.10 Medline

- 8.11 Owens & Minor

- 8.12 Patterson Companies

- 8.13 Soquelec

- 8.14 Southmedic

- 8.15 The Stevens Company Limited