|

시장보고서

상품코드

2038454

포병 시스템 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Artillery Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

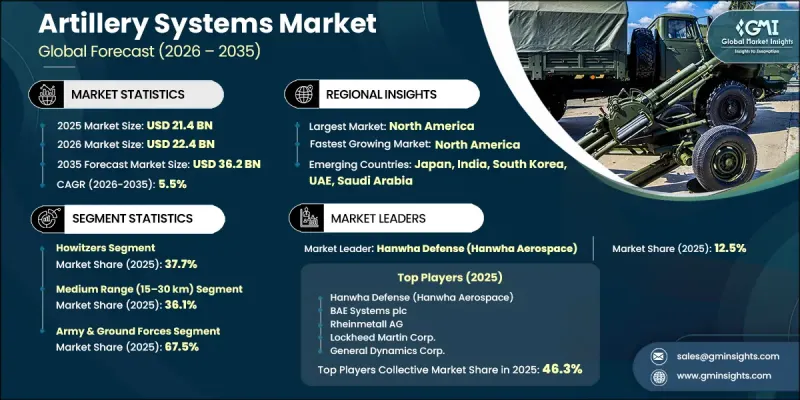

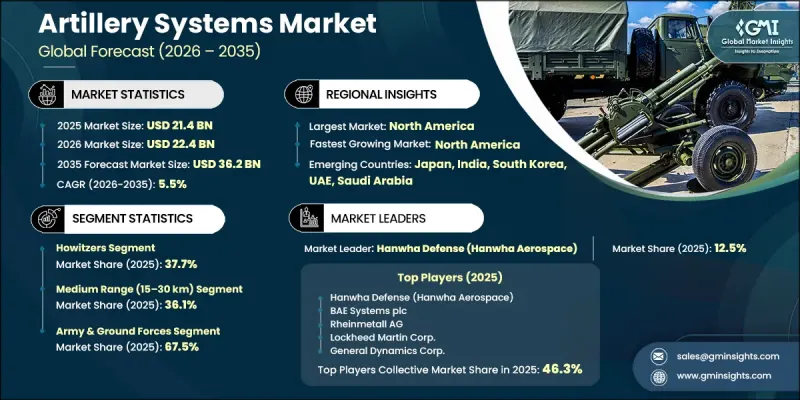

세계의 포병 시스템 시장은 2025년에 214억 달러로 평가되었고, CAGR 5.5%로 성장할 전망이며, 2035년까지 362억 달러에 이를 것으로 추정되고 있습니다.

시장 성장은 국방 현대화 노력 증가와 군사 기술 개발의 국제 협력 강화에 의해 뒷받침되고 있습니다. 각국 정부와 방산업체들은 첨단 포병 솔루션 개발을 가속화하기 위해 공동 프로그램, 파트너십, 기술 공유 협정에 점점 더 많이 참여하고 있습니다. 이러한 협력 관계는 개발 비용 절감, 혁신의 효율성, 그리고 차세대 시스템의 생산 기간 단축에 기여하고 있습니다. 또한, 지정학적 긴장이 고조되고 전투 시나리오가 변화함에 따라 보다 진보되고 적응력이 높은 포병 플랫폼에 대한 수요가 증가하고 있습니다. 기동성, 정확도, 기술을 활용한 무기체계로의 전환은 각국 국방부대의 조달 전략에 더 많은 영향을 미치고 있습니다. 또한 비대칭 전쟁의 위협이 작전 요건을 재구성하고 있으며, 유연하고 신속하게 대응할 수 있는 포병 능력에 대한 중요성이 커지고 있습니다. R&D에 대한 지속적인 투자와 여러 국가의 현대화 프로그램이 결합되어 장기적인 시장 확대를 촉진하고 세계 방위 태세를 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 214억 달러 |

| 예측 시장 규모 | 362억 달러 |

| CAGR | 5.5% |

2025년 기준, 곡사포 부문은 시장 점유율의 37.7%를 차지했습니다. 이 부문은 운용 유연성, 사거리 확장 능력, 다양한 전투 환경에서 효과적이라는 장점으로 인해 견고한 수요를 유지하고 있습니다. 표적 포착 정확도, 자동화, 기동성의 지속적인 향상에 힘입어 공격과 방어 임무 모두에서 널리 활용되고 있습니다. 이러한 개선을 통해 현대 전장 작전에서의 중요성이 강화되고 시장 내 선도적 지위를 유지하고 있습니다.

중거리(15-30km) 구간은 2025년 36.1%의 점유율을 차지했습니다. 이 부문은 사거리, 정확도, 전술적 효율성을 겸비한 균형 잡힌 성능 특성으로 인해 지속적으로 성장하고 있습니다. 다양한 군사 작전에 적응할 수 있어 다양한 임무 요건에 적합합니다. 다양한 전투 상황에서 이 부문의 높은 작전적 유용성은 전 세계 방위군에서 꾸준히 채택되는 데 기여하고 있습니다.

2025년 북미 포병 시스템 시장은 35.7%의 점유율을 차지했습니다. 이 지역의 우위는 첨단 국방 인프라, 강력한 기술력, 군사 현대화 프로그램에 대한 정부의 지속적인 투자에 의해 뒷받침되고 있습니다. 사거리와 정확도가 향상된 시스템을 포함한 차세대 포병 플랫폼의 지속적인 개발이 조달 활동을 주도하고 있습니다. 주요 방산업체들의 적극적인 진출은 세계 시장에서 이 지역의 입지를 더욱 공고히 하고 포병 기술의 지속적인 발전을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 시스템 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 플랫폼별(2022-2035년)

제7장 시장 추산 및 예측 : 사정거리별(2022-2035년)

제8장 시장 추산 및 예측 : 컴포넌트별(2022-2035년)

제9장 시장 추산 및 예측 : 구경별(2022-2035년)

제10장 시장 추산 및 예측 : 최종 사용자별(2022-2035년)

제11장 시장 추산 및 예측 : 지역별(2022-2035년)

제12장 기업 개요

AJY 26.06.11The Global Artillery Systems Market was valued at USD 21.4 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 36.2 billion by 2035.

Market growth is supported by increasing defense modernization initiatives and stronger international collaboration in military technology development. Governments and defense manufacturers are increasingly engaging in joint programs, partnerships, and technology-sharing agreements to accelerate the development of advanced artillery solutions. These collaborations help reduce development costs, improve innovation efficiency, and shorten production timelines for next-generation systems. Rising geopolitical tensions and evolving combat scenarios are also pushing demand for more advanced and adaptable artillery platforms. The shift toward highly mobile, precise, and technology-enabled weapon systems is further influencing procurement strategies across defense forces. Additionally, asymmetric warfare threats are reshaping operational requirements, leading to greater emphasis on flexible and responsive artillery capabilities. Continuous investment in research and development, combined with modernization programs across multiple countries, is reinforcing long-term market expansion and strengthening global defense readiness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.4 Billion |

| Forecast Value | $36.2 Billion |

| CAGR | 5.5% |

The howitzers segment accounted for 37.7% share in 2025. This segment maintains strong demand due to its operational flexibility, extended range capabilities, and effectiveness across multiple combat environments. It is widely used for both offensive and defensive missions, supported by continuous advancements in targeting precision, automation, and mobility. These improvements have strengthened its relevance in modern battlefield operations and sustained its leadership position within the market.

The medium-range (15-30 km) segment held 36.1% share in 2025. This segment continues to grow due to its balanced performance characteristics, offering a combination of range, accuracy, and tactical efficiency. Its adaptability across diverse military operations makes it suitable for a wide range of mission requirements. The segment's strong operational utility in varied combat conditions is contributing to its steady adoption across defense forces globally.

North America Artillery Systems Market accounted for 35.7% share in 2025. The region's dominance is supported by advanced defense infrastructure, strong technological capabilities, and sustained government investment in military modernization programs. Continuous development of next-generation artillery platforms, including systems with enhanced range and precision capabilities, is driving procurement activity. Strong participation from leading defense manufacturers further strengthens the region's position in the global market and supports ongoing advancements in artillery technology.

Key companies operating in the Global Artillery Systems Market include Lockheed Martin Corporation, BAE Systems plc, Rheinmetall AG, Hanwha Defense, Nexter Systems (KNDS Group), General Dynamics Corporation, and Elbit Systems Ltd. Companies in the Artillery Systems Market are focusing on technological innovation, strategic partnerships, and defense collaboration agreements to strengthen their competitive position. Significant investments are being directed toward research and development to enhance system accuracy, mobility, and automation capabilities. Firms are actively engaging in joint ventures and international defense programs to share expertise and reduce development costs. Expansion of production capacities and modernization of manufacturing facilities are also key priorities to meet rising demand. Additionally, companies are integrating advanced digital systems, including fire control technologies and precision-guided solutions, to improve operational efficiency. Strengthening long-term government contracts and expanding global defense networks are further supporting sustained market positioning and growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Platform trends

- 2.2.3 Range trends

- 2.2.4 Component trends

- 2.2.5 Caliber trends

- 2.2.6 End-user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased defense collaboration

- 3.2.1.2 Rising asymmetric warfare

- 3.2.1.3 Adoption of network-centric warfare

- 3.2.1.4 Enhanced mobility and deployment

- 3.2.1.5 Focus on indigenous defense production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory and compliance issues

- 3.2.2.2 Supply chain disruptions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of precision-guided artillery systems

- 3.2.3.2 Growth in defense modernization programs in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Defense budget analysis

- 3.9 Global defense spending trends

- 3.10 Regional defense budget allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Pricing Analysis (Driven by Primary Research)

- 3.11.1 Historical Price Trend Analysis

- 3.11.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.12 Trade Data Analysis (Based on Paid Database)

- 3.12.1 Import/Export Volume & Value Trends

- 3.12.2 Key Trade Corridors & Tariff Impact

- 3.13 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.13.1 AI-Driven Disruption of Existing Business Models

- 3.13.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.13.3 Risks, Limitations & Regulatory Considerations

- 3.14 Capacity & Production Landscape (Driven by Primary Research)

- 3.14.1 Production Capacity by Region & Key Producer

- 3.14.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia-Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Howitzers

- 5.2.1 Towed howitzers

- 5.2.2 Self-propelled howitzers

- 5.2.3 Wheeled self-propelled howitzers

- 5.2.4 Others

- 5.3 Mortars

- 5.3.1 Light mortars (below 100mm)

- 5.3.2 Medium mortars (100mm-120mm)

- 5.3.3 Heavy mortars (above 120mm)

- 5.4 Rocket artillery

- 5.4.1 Multiple launch rocket systems (MLRS)

- 5.4.2 Guided rocket artillery

- 5.4.3 Unguided rocket artillery

- 5.5 Anti-aircraft guns

- 5.5.1 Short-range air defense (SHORAD) artillery

- 5.5.2 Medium-range air defense artillery

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Towed artillery

- 6.2.1 Lightweight towed systems

- 6.2.2 Medium towed systems

- 6.2.3 Heavy towed systems

- 6.3 Self-propelled artillery

- 6.3.1 Tracked self-propelled

- 6.3.2 Wheeled self-propelled

- 6.3.3 Amphibious self-propelled

- 6.4 Naval artillery

- 6.4.1 Surface vessel artillery

- 6.4.2 Coastal defense systems

- 6.5 Rail-based artillery

Chapter 7 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Short range (up to 15 km)

- 7.3 Medium range (15-30 km)

- 7.4 Long range (above 30 km)

Chapter 8 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Gun system

- 8.3 Fire control system

- 8.4 Ammunition

- 8.5 Auxiliary systems

Chapter 9 Market Estimates and Forecast, By Caliber, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Small caliber (below 100mm)

- 9.3 Medium caliber (100mm-155mm)

- 9.4 Large caliber (above 155mm)

Chapter 10 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Army & ground forces

- 10.2.1 Armored brigade combat teams

- 10.2.2 Infantry divisions

- 10.2.3 Others

- 10.3 Naval forces

- 10.3.1 Surface warfare vessels

- 10.3.2 Coastal defense units

- 10.3.3 Others

- 10.4 Air defense forces

- 10.4.1 Integrated air defense systems

- 10.4.2 Mobile air defense units

- 10.4.3 Others

- 10.5 Border security & paramilitary

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.3.7 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Rest of MEA

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 BAE Systems plc

- 12.1.2 Lockheed Martin Corporation

- 12.1.3 Rheinmetall AG

- 12.1.4 Hanwha Defense

- 12.1.5 Nexter Systems (KNDS Group)

- 12.1.6 General Dynamics Corporation

- 12.1.7 Elbit Systems Ltd.

- 12.2 Regional Champions

- 12.2.1 Bharat Forge Limited (Kalyani Group)

- 12.2.2 PT Pindad (Indonesia)

- 12.2.3 Denel SOC Ltd. (South Africa)

- 12.3 Emerging Players

- 12.3.1 Military Industry Corporation (Iraq)

- 12.3.2 Yugoimport SDPR (Serbia)