|

시장보고서

상품코드

2038468

산업용 발전기 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

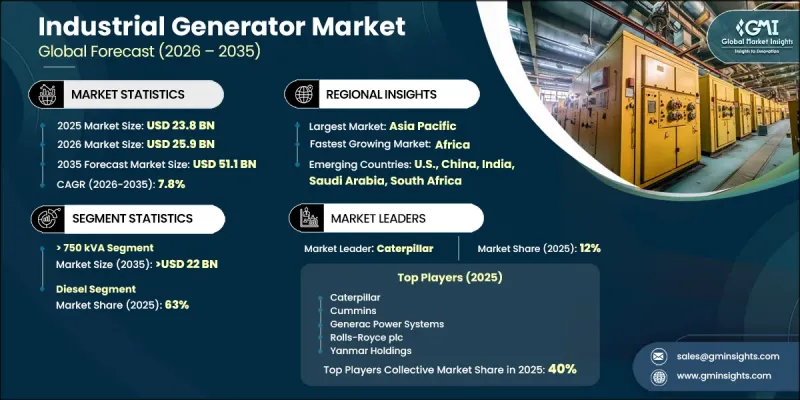

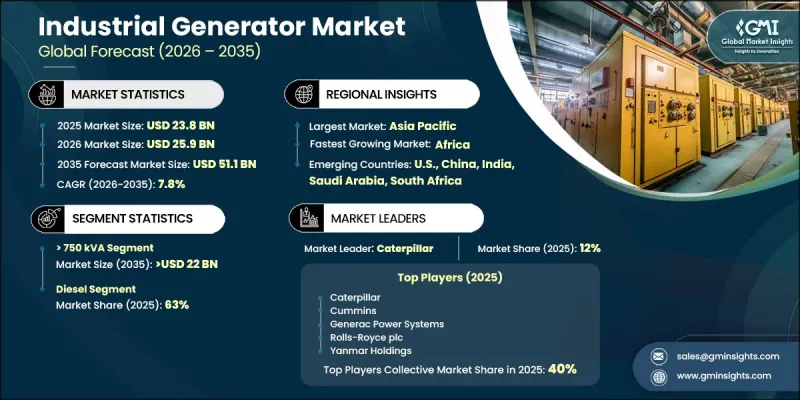

세계의 산업용 발전기 시장은 2025년에 238억 달러로 평가되었고, CAGR 7.8%로 성장할 전망이며, 2035년까지 511억 달러에 이를 것으로 예측됩니다.

신흥국의 강력한 산업 확장과 대규모 인프라 개발로 인해 안정적인 백업 전원 공급 장치 및 연속 공급 시스템에 대한 수요가 증가하고 있습니다. 제조, 건설, 석유 및 가스, 광업 등 각 분야에서 끊김 없는 전력 공급에 대한 수요가 증가하면서 시장 성장을 더욱 촉진하고 있습니다. 급속한 도시화와 산업 역량에 대한 투자 확대도 지속적인 수요 요인으로 작용하고 있습니다. 동시에, 기술의 발전은 진화하는 환경 기준에 부합하는 보다 연료 효율적이고 배출량이 적은 발전 시스템을 가능하게 하고 있습니다. 이러한 발전은 다양한 최종 사용 분야에서 최신 산업용 발전 솔루션의 보급을 촉진하고 있습니다. 또한 비즈니스 연속성, 에너지 안보, 다운타임 감소에 대한 관심이 높아진 것도 구매 결정에 영향을 미치고 있습니다. 또한, 규제 프레임워크의 강화와 보다 깨끗하고 효율적인 에너지 솔루션으로의 점진적인 전환은 전체 시장 환경의 제품 혁신과 도입 전략에 영향을 미치고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 238억 달러 |

| 예측 시장 규모 | 511억 달러 |

| CAGR | 7.8% |

산업용 발전기는 전력망 정전 시 또는 지속적이고 안정적인 전력 공급이 필요한 경우 전력을 공급하도록 설계된 고내구성 엔지니어링 전력 시스템입니다. 산업시설 및 중요 인프라의 업무 연속성 확보에 있어 매우 중요한 역할을 하고 있습니다. 이들 시스템은 높은 부하 용량에 대응하고 일상적인 운영 환경과 비상시 운영 환경 모두에서 안정적인 성능을 유지할 수 있도록 구축되어 있습니다.

공급망 인프라 강화에 초점을 맞춘 산업 투자 증가와 정부 정책의 진화는 제조업의 확장을 뒷받침하고 있으며, 이는 신뢰할 수 있는 비상 전원 시스템에 대한 수요를 견인하고 있습니다. 또한, 에너지 효율과 청정 전력 솔루션에 대한 관심이 높아지고 있는 것도 업계의 방향성을 형성하고 있습니다. 건설, 광업, 석유 및 가스, 제조업을 포함한 다양한 분야에서 중단 없는 전력에 대한 의존도가 높아지면서 시장 확대가 더욱 가속화되고 있습니다. 에너지 성능 향상과 정전 감소를 위한 규제 압력도 각 최종 사용 산업에서 도입을 촉진하고 있습니다.

2025년 기준, 디젤 산업용 발전기 부문은 63%의 점유율을 차지했습니다. 이러한 시스템은 운영상의 신뢰성, 적응성 및 외부 기상 조건에 영향을 받지 않고 작동할 수 있는 능력으로 인해 여전히 널리 사용되고 있습니다. 비용 효율성과 안정적인 전력 공급은 산업 전반에 걸친 견고한 수요를 뒷받침하고 있습니다. 산업 활동의 확대는 신뢰할 수 있는 전력 공급 솔루션에 대한 요구를 더욱 강화하고 있습니다.

정격 출력 750kVA 이상의 산업용 발전기 시장은 2035년까지 220억 달러에 달할 것으로 예측됩니다. 광업 및 대규모 인프라 프로젝트 수요 증가가 이 부문의 성장에 크게 기여하고 있습니다. 이 대용량 발전기는 굴삭기, 크레인, 컨베이어 시스템 등 중장비에 전력을 공급하는 데 널리 이용되고 있습니다. 또한, 원격지 및 Off-grid 지역에서의 도입 확대도 시장 확대에 힘을 실어주고 있습니다.

미국의 산업용 발전기 시장은 2025년 39억 달러로 평가되었습니다. 제조업 수요 증가는 가동 중단 방지 및 예기치 않은 정전으로 인한 생산 손실 감소에 대한 요구에 힘입은 것입니다. 높은 내구성, 우수한 성능, 안정성 및 산업에서의 연속 사용 적합성이 제품의 채택을 뒷받침하는 주요 요인이 되었습니다. 산업 생산량 확대와 생산시설의 현대화도 시장 침투를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 출력별(2022-2035년)

제6장 시장 규모 및 예측 : 최종 용도별(2022-2035년)

제7장 시장 규모 및 예측 : 용도별(2022-2035년)

제8장 시장 규모 및 예측 : 연료별(2022-2035년)

제9장 시장 규모 및 예측 : 지역별(2022-2035년)

제10장 기업 개요

AJY 26.06.11The Global Industrial Generator Market was valued at USD 23.8 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 51.1 billion by 2035.

Strong industrial expansion and large-scale infrastructure development across emerging economies are reinforcing the demand for reliable backup and continuous power systems. The increasing requirement for uninterrupted electricity across manufacturing, construction, oil and gas, and mining operations is further strengthening market growth. Rapid urbanization and rising investments in industrial capacity are also contributing to sustained demand. At the same time, technological advancements are enabling more fuel-efficient, lower-emission generator systems that comply with evolving environmental standards. These developments are encouraging broader adoption of modern industrial generator solutions across diverse end-use sectors. Growing focus on operational resilience, energy security, and reduced downtime is also shaping purchasing decisions. In addition, stricter regulatory frameworks and a gradual shift toward cleaner and more efficient energy solutions are influencing product innovation and deployment strategies across the market landscape.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.8 Billion |

| Forecast Value | $51.1 Billion |

| CAGR | 7.8% |

An industrial generator is a heavy-duty, engineered power system designed to supply electricity during grid disruptions or when continuous and stable power is required. It plays a critical role in ensuring operational continuity across industrial facilities and essential infrastructure. These systems are built to handle high load capacities and maintain stable performance under both routine and emergency operating conditions.

Rising industrial investments and evolving government policies focused on strengthening supply chain infrastructure are supporting manufacturing expansion, which in turn is driving demand for reliable backup power systems. The growing emphasis on energy efficiency and cleaner power solutions is also shaping industry direction. Increased reliance on uninterrupted electricity across multiple sectors, including construction, mining, oil and gas, and manufacturing, is further supporting market expansion. Regulatory pressures aimed at improving energy performance and reducing outages are reinforcing adoption across end-use industries.

The diesel industrial generator segment accounted for 63% share in 2025. These systems remain widely used due to their operational reliability, adaptability, and ability to function independently of external weather conditions. Their cost-effectiveness and consistent power delivery continue to support strong demand across industrial applications. Expanding industrial activity is further reinforcing the need for dependable electricity supply solutions.

The > 750 kVA rated industrial generator market is expected to reach USD 22 billion by 2035. Increasing demand from mining operations and large-scale infrastructure projects is significantly contributing to segment growth. These high-capacity generators are extensively used to power heavy machinery such as excavators, cranes, and conveyor systems. Their growing deployment in remote, off-grid locations is also strengthening market expansion.

U.S. Industrial Generator Market was valued at USD 3.9 billion in 2025. Rising demand from manufacturing sectors is driven by the need for uninterrupted operations and reduced production losses caused by unexpected outages. High durability, strong performance, stability, and suitability for continuous industrial use are key factors supporting product adoption. Expanding industrial output and modernization of production facilities are further strengthening market penetration.

Key industry participants operating in the Industrial Generator Market include Cummins, Caterpillar, Generac Power Systems, Atlas Copco, Mitsubishi Heavy Industries, Wartsila, Rolls-Royce, FG Wilson, HIMOINSA, Yanmar Holdings, JC Bamford Excavators, Kirloskar, Ashok Leyland, MAHINDRA POWEROL, Powerica, Deere & Company, Greaves Cotton, Rehlko, Supernova Genset, and Sudhir Power. Companies in the Industrial Generator Market are focusing on expanding product efficiency through advanced engine technologies and fuel optimization systems. Strategic investments in low-emission and hybrid power solutions are helping firms align with tightening environmental regulations. Manufacturers are also strengthening global distribution networks and establishing regional service hubs to improve after-sales support and operational reliability. Partnerships with industrial end users are being used to secure long-term supply contracts and enhance market stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 End use trends

- 2.1.4 Fuel trends

- 2.1.5 Application trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of industrial generator

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.9.1 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.11.1 By region (Driven by Primary Research)

- 3.11.2 By power rating (Driven by Primary Research)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 ≤ 75 kVA

- 5.3 > 75 kVA - 375 kVA

- 5.4 > 375 KVA - 750 kVA

- 5.5 > 750 kVA

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Oil & gas

- 6.3 Manufacturing

- 6.4 Construction

- 6.5 Electric utilities

- 6.6 Mining

- 6.7 Transport & logistics

- 6.8 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Standby

- 7.3 Peak shaving

- 7.4 Prime/continuous

Chapter 8 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 Diesel

- 8.3 Gas

- 8.4 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & ‘000 Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Russia

- 9.3.2 UK

- 9.3.3 Germany

- 9.3.4 France

- 9.3.5 Spain

- 9.3.6 Austria

- 9.3.7 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.4.8 Thailand

- 9.4.9 Vietnam

- 9.4.10 Philippines

- 9.4.11 Myanmar

- 9.5 Middle East

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Turkey

- 9.5.5 Iran

- 9.5.6 Oman

- 9.6 Africa

- 9.6.1 Egypt

- 9.6.2 Nigeria

- 9.6.3 Algeria

- 9.6.4 South Africa

- 9.6.5 Angola

- 9.6.6 Kenya

- 9.7 Latin America

- 9.7.1 Brazil

- 9.7.2 Mexico

- 9.7.3 Argentina

- 9.7.4 Chile

Chapter 10 Company Profiles

- 10.1 Ashok Leyland

- 10.2 Atlas Copco

- 10.3 Caterpillar

- 10.4 Cummins

- 10.5 Deere & Company

- 10.6 FG Wilson

- 10.7 Generac Power Systems

- 10.8 Greaves Cotton

- 10.9 HIMOINSA

- 10.10 JC Bamford Excavators Ltd.

- 10.11 Kirloskar

- 10.12 MAHINDRA POWEROL

- 10.13 Mitsubishi Heavy Industries

- 10.14 Powerica

- 10.15 Rehlko

- 10.16 Rolls Royce plc

- 10.17 Sudhir Power

- 10.18 Supernova Genset

- 10.19 Wartsila

- 10.20 Yanmar Holdings