|

시장보고서

상품코드

2038647

하이퍼카 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Hyper Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

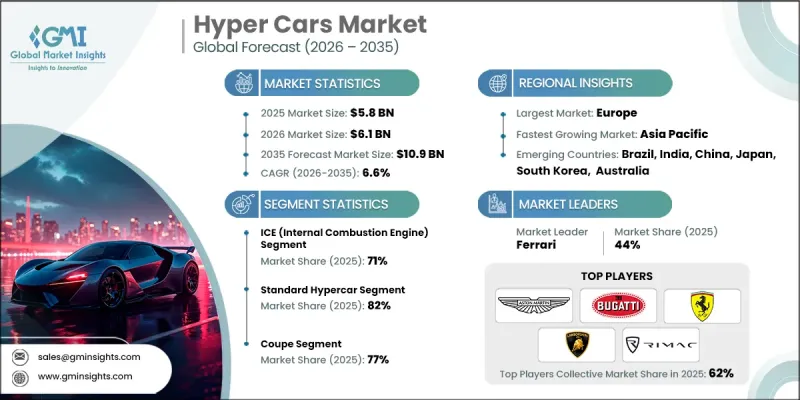

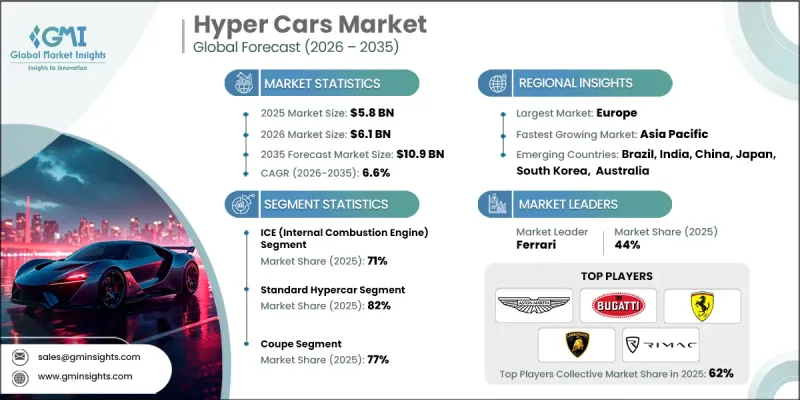

세계의 하이퍼카 시장은 2025년에 58억 달러로 평가되었고, CAGR 6.6%로 성장할 전망이며, 2035년까지 109억 달러에 이를 것으로 예측됩니다.

이 시장은 극한의 속도와 고도의 엔지니어링, 그리고 희소성을 겸비한 초고급 및 고성능 차량에 대한 수요 증가로 인해 성장하고 있습니다. 하이퍼카는 엘리트 고객 및 수집가들을 위해 디자인된 한정 생산 자동차로서, 최첨단 공기역학적 성능, 경량 구조 및 첨단 추진 기술을 제공합니다. 각 제조업체들은 진화하는 성능과 규제에 대한 기대에 부응하기 위해 고출력 내연기관과 더불어 하이브리드 및 완전 전기 파워트레인을 통합하는 움직임을 강화하고 있습니다. 첨단 디지털 시스템, 지능형 운전 보조 기능, 그리고 고급스러움을 강조한 인테리어가 이 차량의 매력을 한층 더 높여줍니다. 개인화, 독점성, 그리고 고급 자동차 경험에 대한 소비자의 선호도가 높아지면서 시장 확대에 힘을 보태고 있습니다. 탄소섬유, 고강도 합금 등 경량 소재의 지속적인 발전으로 속도, 핸들링, 효율성이 향상되고 있습니다. 또한, 액티브 에어로다이내믹스, 어댑티브 서스펜션 시스템, 성능 중심의 전자장치의 혁신은 드라이빙 다이내믹스를 재정의하고 있습니다. 전통적인 장인정신과 현대의 뛰어난 엔지니어링의 융합은 세계 하이퍼카 산업 경쟁 구도를 계속 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 58억 달러 |

| 예측 기간 시장 규모 | 109억 달러 |

| CAGR | 6.6% |

내연기관 부문은 2025년 71%의 점유율을 차지한 것으로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 6.5%를 나타낼 것으로 예측됩니다. 이 부문은 고성능 특성, 독특한 엔진 사운드, 세련된 드라이빙 경험으로 인해 지속적으로 높은 관심을 받고 있습니다. 기존의 파워트레인 기술은 뛰어난 응답성, 기술적 성숙도, 가혹한 주행 조건에서도 안정적인 성능을 발휘할 수 있는 능력으로 여전히 널리 평가받고 있습니다.

표준 하이퍼카 부문은 2025년 82%의 점유율을 차지한 것으로 평가되었고, 2026-2035년 연평균 복합 성장률(CAGR) 6.5%로 확대될 것으로 전망됩니다. 이 카테고리에는 일상 주행의 실용성을 어느 정도 유지하면서 극한의 성능을 발휘하도록 설계된 차량이 포함됩니다. 이들 모델은 일반적으로 고속 주행 성능과 공조 시스템, 인포테인먼트 통합, 승하차 편의성 향상과 같은 편안함을 중시하는 기능과 균형을 이루며 고급 성능 부문에서 보다 실용적인 존재로 자리 잡고 있습니다.

이탈리아 하이퍼카 시장은 2035년까지 연평균 5.6%의 성장률을 보일 것으로 예측됩니다. 고급 자동차 엔지니어링과 성능 중심의 차량 개발에서 탄탄한 전통을 가지고 있는 것이 강점입니다. 하이브리드 기술, 탄소섬유 구조, 공기역학 설계의 지속적인 발전이 차세대 하이퍼카 생산을 뒷받침하고 있습니다. 이탈리아 제조업체들은 전동화와 전통적인 성능 엔지니어링을 점점 더 통합하여 진화하는 배기가스 규제를 충족시키면서 효율성과 운전 경험을 모두 향상시키고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 추진력별(2022-2035년)

제6장 시장 추산 및 예측 : 보디 유형별(2022-2035년)

제7장 시장 추산 및 예측 : 엔진 배기량별(2022-2035년)

제8장 시장 추산 및 예측 : 성능 구분별(2022-2035년)

제9장 시장 추산 및 예측 : 용도별(2022-2035년)

제10장 시장 추산 및 예측 : 지역별(2022-2035년)

제11장 기업 개요

AJYThe Global Hyper Cars Market was valued at USD 5.8 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 10.9 billion by 2035.

The market is witnessing growth due to rising demand for ultra-luxury, high-performance vehicles that combine extreme speed with advanced engineering and exclusivity. Hyper cars are limited-production automobiles designed for elite customers and collectors, offering cutting-edge aerodynamics, lightweight construction, and advanced propulsion technologies. Manufacturers are increasingly integrating hybrid and fully electric powertrains alongside high-output internal combustion engines to meet evolving performance and regulatory expectations. The incorporation of advanced digital systems, intelligent driving support features, and luxury-focused interiors is further enhancing the appeal of these vehicles. Growing consumer preference for personalization, exclusivity, and high-end automotive experiences is also supporting market expansion. Continuous advancements in lightweight materials such as carbon fiber and high-strength alloys are improving speed, handling, and efficiency. In addition, innovation in active aerodynamics, adaptive suspension systems, and performance-focused electronics is redefining driving dynamics. The combination of heritage craftsmanship and modern engineering excellence continues to shape the competitive landscape of the hyper cars industry globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.8 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 6.6% |

The internal combustion engine segment held a 71% share in 2025 and is expected to grow at a CAGR of 6.5% through 2035. This segment continues to attract strong interest due to its high-performance characteristics, distinctive engine acoustics, and refined driving experience. Traditional powertrain technologies remain widely valued for their responsiveness, engineering maturity, and ability to deliver consistent performance under extreme driving conditions.

The standard hypercar segment accounted for 82% share in 2025 and is projected to expand at a CAGR of 6.5% during 2026-2035. This category includes vehicles engineered for extreme performance while maintaining a degree of usability for regular driving. These models typically balance high-speed capability with comfort-oriented features such as climate control systems, infotainment integration, and improved cabin accessibility, making them more practical within the luxury performance segment.

Italy Hyper Cars Market is expected to grow at a CAGR of 5.6% through 2035. The country benefits from a strong heritage in luxury automotive engineering and performance-focused vehicle development. Continuous advancements in hybrid technologies, carbon-fiber construction, and aerodynamic design are supporting next-generation hypercar production. Italian manufacturers are increasingly combining electrification with traditional performance engineering, enhancing both efficiency and driving experience while meeting evolving emissions standards.

Key companies operating in the Global Hyper Cars Market include Ferrari, Bugatti, McLaren, Lamborghini, Aston Martin, Koenigsegg, Rimac, Pagani, Lotus, and Mercedes-AMG. Companies in the Hyper Cars Market are focusing on strengthening their competitive position through continuous innovation in powertrain technologies, lightweight materials, and aerodynamic engineering. Manufacturers are investing heavily in hybrid and electric performance systems to align with evolving emission standards while maintaining extreme performance levels. Strategic emphasis is being placed on exclusivity, limited production models, and highly personalized vehicle configurations to enhance brand value. Collaborations with advanced material suppliers and technology firms are enabling improvements in carbon fiber usage, battery systems, and vehicle intelligence platforms. Companies are also expanding their global presence through selective market entry strategies and exclusive dealership networks.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Body Style

- 2.2.4 Engine Size

- 2.2.5 Performance Tier

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising ultra-high-net-worth individual (UHNWI) population & luxury spending

- 3.2.1.2 Growing demand for exclusive, limited-edition performance vehicles

- 3.2.1.3 Shift toward electric powertrain technology & environmental consciousness

- 3.2.1.4 Technological advancements in lightweight materials & aerodynamics

- 3.2.1.5 Increasing investment in track-day experiences & motorsport heritage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Prohibitively high acquisition & ownership costs

- 3.2.2.2 Limited production volumes & extended waiting periods

- 3.2.2.3 Complex homologation & regulatory compliance requirements

- 3.2.2.4 Customer resistance to electric powertrains among traditional enthusiasts

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging electric hypercar segment attracting new entrants

- 3.2.3.2 Growing appetite in Asia Pacific & Middle East ultra-luxury markets

- 3.2.3.3 Digitalization & connectivity integration in performance vehicles

- 3.2.3.4 Expansion of hypercar-focused events, rallies & brand experiences

- 3.2.3.5 Strategic partnerships between boutique manufacturers & established OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. EPA Emission Standards (CAA & Tier 3 Regulations)

- 3.4.1.2 California Advanced Clean Cars II Regulation

- 3.4.1.3 NHTSA Low Volume Manufacturer Regulations

- 3.4.2 Europe

- 3.4.2.1 EU CO2 Emission Standards (Euro 6/7 Regulations)

- 3.4.2.2 EU Small Series Type Approval (SSTA)

- 3.4.2.3 United Kingdom Zero Emission Vehicle (ZEV) Mandate

- 3.4.2.4 France Bonus-Malus CO2 Tax System

- 3.4.3 Asia Pacific

- 3.4.3.1 China New Energy Vehicle (NEV) Policy

- 3.4.3.2 Japan Green Growth Strategy (Carbon Neutrality 2050)

- 3.4.3.3 South Korea Eco-Friendly Vehicle Policy

- 3.4.3.4 Singapore Vehicular Emissions Scheme (VES)

- 3.4.4 Latin America

- 3.4.4.1 Brazil PROCONVE Emission Standards

- 3.4.4.2 Mexico NOM Emission Regulations

- 3.4.4.3 Chile Electromobility Strategy

- 3.4.5 MEA

- 3.4.5.1 UAE Green Mobility Strategy 2030

- 3.4.5.2 Saudi Arabia Vision 2030 (Transport Electrification)

- 3.4.5.3 South Africa Automotive Masterplan (SAAM 2035)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electric powertrain technology evolution

- 3.7.1.2 Hybrid propulsion systems architecture

- 3.7.1.3 Advanced aerodynamic design innovations

- 3.7.2 Emerging technologies

- 3.7.2.1 Lightweight material technologies (carbon fiber, titanium)

- 3.7.2.2 Active suspension & chassis control systems

- 3.7.1 Current technological trends

- 3.8 Patent analysis (Driven by primary research)

- 3.9 Pricing analysis (Driven by primary research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium, value, cost-plus)

- 3.10 Trade data analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.10.3 Cross-border e-commerce flows

- 3.11 Capacity & production landscape (Driven by primary research)

- 3.11.1 Installed capacity by region & key producer

- 3.11.2 Capacity utilization rates & expansion pipelines

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Sustainability and environmental impact analysis

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates and Forecast, By Propulsion, 2022 - 2035 ($ Million, Units)

- 5.1 Key trends

- 5.2 ICE (Internal Combustion Engine)

- 5.3 Battery electric

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Body Style, 2022 - 2035 ($ Million, Units)

- 6.1 Key trends

- 6.2 Coupe

- 6.3 Convertible

- 6.4 Roadster

Chapter 7 Market Estimates and Forecast, By Engine Size, 2022 - 2035 ($ Million, Units)

- 7.1 Key trends

- 7.2 Below 1499 cc (Compact)

- 7.3 1500-2499 cc (Mid-size)

- 7.4 Above 2500 cc (Full-size)

Chapter 8 Market Estimates and Forecast, By Performance Tier, 2022 - 2035 ($ Million, Units)

- 8.1 Key trends

- 8.2 Standard hypercar

- 8.3 Mega car/ultra-performance

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million, Units)

- 9.1 Key trends

- 9.2 Private ownership

- 9.3 Track / racing use

- 9.4 Automotive events & exhibitions

- 9.5 Rental & experiential services

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aston Martin Lagonda

- 11.1.2 Bugatti Automobiles

- 11.1.3 Ferrari

- 11.1.4 Koenigsegg Automotive

- 11.1.5 Lamborghini

- 11.1.6 Lotus Cars

- 11.1.7 McLaren Automotive

- 11.1.8 Pagani Automobili

- 11.1.9 Porsche

- 11.2 Regional Players

- 11.2.1 Hennessey Performance Engineering

- 11.2.2 Rimac Automobili

- 11.2.3 SSC North America

- 11.2.4 W Motors

- 11.3 Emerging Players

- 11.3.1 Apollo Automobil

- 11.3.2 Aspark

- 11.3.3 Czinger Vehicles

- 11.3.4 Devel Motors

- 11.3.5 Gordon Murray Automotive

- 11.3.6 Pininfarina Automobili

- 11.3.7 Zenvo Automotive