|

시장보고서

상품코드

2038667

산업용 청소기 시장 : 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Vacuum Cleaner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

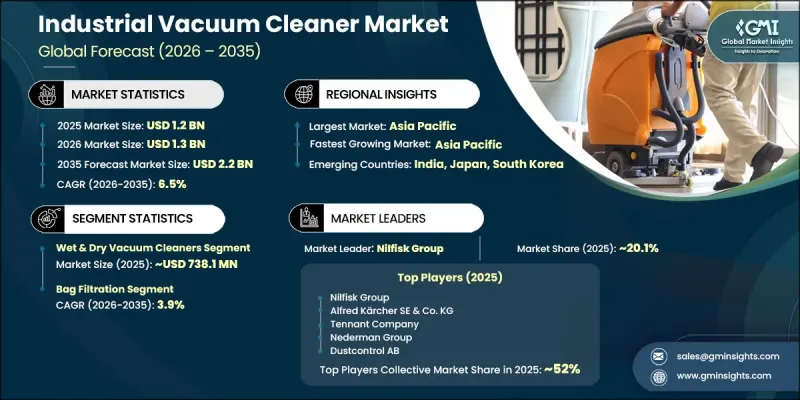

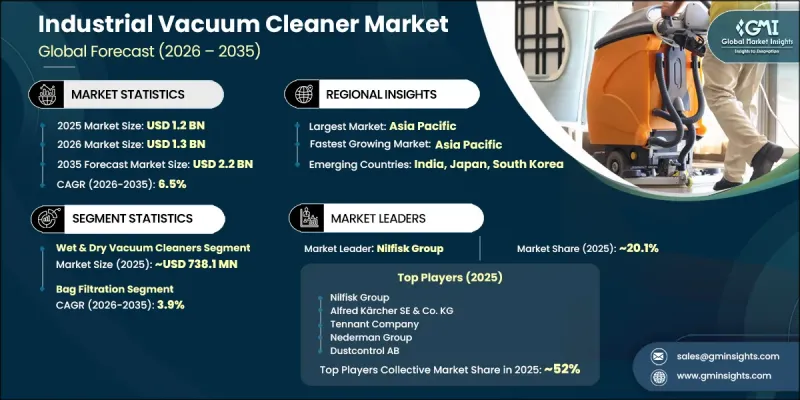

세계의 산업용 청소기 시장은 2025년에 12억 달러로 평가되었고, CAGR 6.5%로 성장할 전망이며, 2035년까지 22억 달러에 이를 것으로 예측됩니다.

이 시장은 산업의 급속한 확장과 다양한 분야의 제조 활동의 지속적인 증가에 힘입어 꾸준한 성장세를 보이고 있습니다. 자동차, 식음료, 제약, 금속 가공 등의 산업에서는 안전한 작업 환경을 유지하고 제품 품질을 보장하기 위해 고성능 분진 및 미립자 흡입 시스템에 대한 의존도가 높아지고 있습니다. 생산시설의 규모와 복잡성이 증가함에 따라 대용량, 연속 가동이 가능한 청소 장비에 대한 수요가 증가하고 있습니다. 동시에 환경 및 산업안전보건 규정의 강화로 인해 첨단 산업용 진공 솔루션으로의 전환이 가속화되고 있습니다. 기업들은 전통적인 청소 방법에서 벗어나 효율성과 규정 준수를 위해 설계된 전문 시스템을 채택하고 있습니다. 산업보건 기준에 대한 관심이 높아진 것도 강력한 성장의 촉매제가 되고 있습니다. 북미, 유럽, 아시아태평양을 포함한 주요 지역의 규제 프레임워크는 먼지 노출과 대기 질에 대한 엄격한 제한을 부과하고 있습니다. 미국 OSHA 요건 및 유럽 ATEX 가이드라인과 같은 기준은 HEPA 등급 여과 기능 및 고급 봉쇄 기술을 갖춘 인증된 진공 시스템의 도입을 촉진하고 있습니다. 이러한 요인들이 결합되어 안전성, 효율성, 규제 준수 중심 시장 환경이 형성되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 12억 달러 |

| 예측 시장 규모 | 22억 달러 |

| CAGR | 6.5% |

습식 및 건식 진공 청소기 부문은 2025년에 7억 3,810만 달러 시장 규모를 기록했으며, 2026-2035년 연평균 1.7%의 성장률을 보일 것으로 예측됩니다. 이 부문은 단일 시스템 내에서 액체 및 고형 폐기물을 모두 처리할 수 있는 높은 운영 유연성으로 인해 시장을 주도하고 있습니다. 이 통합 기능은 여러 대의 기계를 필요로 할 필요성을 줄여 건설, 자동차 생산, 금속 가공, 식품 제조 등 다양한 분야의 산업 청소 업무를 효율화합니다. 다양한 어태치먼트, 여과 옵션, 보관 구성이 가능하여 다양한 작업 환경에 대한 적응성이 향상됩니다. 이러한 시스템은 이동식 및 고정식 모두 제공되며, 산업 사용자는 운영 요구 사항 및 시설 규모에 따라 도입할 수 있습니다.

백 필터 시장 부문은 27.8%의 점유율을 차지했며, 2035년까지 연평균 복합 성장률(CAGR) 3.9%를 나타낼 것으로 예측됩니다. 이 제품의 강력한 시장 입지는 비용 효율성, 간단한 구조, 그리고 산업 청소 분야에서 폭넓게 사용되고 있기 때문입니다. 백필터 시스템은 일반적인 산업용 분진 포집에 매우 효과적이며, 교체가 용이하여 유지보수 및 다운타임을 줄일 수 있습니다. 저렴한 가격과 다양한 진공 시스템과의 호환성으로 인해 기존 제조 환경, 건설 현장 및 일반 산업 유지보수 작업에서 선호되는 선택이 되었습니다.

중국의 산업용 청소기 시장은 2025년에 1억 4,080만 달러에 달했으며, 2026-2035년 연평균 8.2%의 성장률을 보일 것으로 예측됩니다. 중국은 대규모로 빠르게 진화하는 제조 생태계를 배경으로 계속해서 주요 성장 거점이 되고 있습니다. 수요는 전자기기 조립, 자동차 제조, 금속 가공, 식품 가공 등의 분야에서 생산 활동의 확대에 의해 강하게 뒷받침되고 있습니다. 이러한 분야에서는 작업의 안전을 보장하기 위해 효율적인 분진 관리가 필수적입니다. 광범위한 산업 단지 및 제조 클러스터 네트워크는 휴대용 및 고정식 진공 시스템에 대한 지속적인 수요를 창출하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별(2022-2035년)

제6장 시장 추산 및 예측 : 여과 기술별(2022-2035년)

제7장 시장 추산 및 예측 : 동력원별(2022-2035년)

제8장 시장 추산 및 예측 : 시스템 유형별(2022-2035년)

제9장 시장 추산 및 예측 : 최종 사용자 산업별(2022-2035년)

제10장 시장 추산 및 예측 : 판매 채널별(2022-2035년)

제11장 시장 추산 및 예측 : 지역별(2022-2035년)

제12장 기업 개요

AJY 26.06.11The Global Industrial Vacuum Cleaner Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 2.2 billion by 2035.

The market is experiencing consistent growth driven by rapid industrial expansion and the continuous rise in manufacturing activities across multiple sectors. Industries such as automotive, food and beverage, pharmaceuticals, and metal fabrication are increasingly dependent on high-performance dust and particulate extraction systems to maintain safe working conditions and ensure product quality. The growing scale and complexity of production facilities are strengthening the demand for high-capacity, continuous-duty cleaning equipment. At the same time, stricter environmental and workplace safety regulations are accelerating the shift toward advanced industrial vacuum solutions. Organizations are moving away from traditional cleaning methods and adopting specialized systems designed for efficiency and compliance. Increasing focus on occupational health standards is also acting as a strong growth catalyst. Regulatory frameworks across major regions, including North America, Europe, and Asia Pacific, are enforcing strict limits on dust exposure and air quality. Standards such as OSHA requirements in the United States and ATEX guidelines in Europe are driving the adoption of certified vacuum systems equipped with HEPA-grade filtration and advanced containment technologies. These combined factors are shaping a market landscape centered on safety, efficiency, and regulatory compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 6.5% |

The wet and dry vacuum cleaners segment generated USD 738.1 million in 2025 and is projected to grow at a CAGR of 1.7% from 2026 to 2035. This segment continues to lead the market due to its high operational flexibility, allowing it to handle both liquid and dry waste within a single system. This integrated capability reduces the need for multiple machines and streamlines industrial cleaning operations across various sectors, including construction, automotive production, metal processing, and food manufacturing. The availability of different attachments, filtration options, and storage configurations enhances its adaptability across diverse working environments. These systems are offered in both mobile and fixed formats, enabling industrial users to deploy them based on operational requirements and facility scale.

The bag filtration segment held a 27.8% share and is expected to grow at a CAGR of 3.9% through 2035. Its strong market presence is attributed to its cost efficiency, simple structure, and wide usage across industrial cleaning applications. Bag filtration systems are highly effective in capturing standard industrial dust and are easy to replace, which reduces maintenance effort and downtime. Their affordability and compatibility with a wide range of vacuum systems make them a preferred choice across traditional manufacturing environments, construction activities, and general industrial maintenance operations.

China Industrial Vacuum Cleaner Market reached USD 140.8 million in 2025 and is projected to grow at a CAGR of 8.2% from 2026 to 2035. The country remains a key growth center due to its large-scale and rapidly evolving manufacturing ecosystem. Demand is strongly supported by expanding production activities in sectors such as electronics assembly, automotive manufacturing, metalworking, and food processing, where efficient dust management is essential for operational safety. The extensive network of industrial zones and manufacturing clusters continues to generate sustained demand for both portable and stationary vacuum systems.

Key companies operating in the Global Industrial Vacuum Cleaner Market include Alfred Karcher SE & Co. KG, Nilfisk Group, Tennant Company, Nederman Group, Delfin Industrial Vacuums, Ruwac Industriesauger GmbH, Depureco Industrial Vacuums Srl, American Vacuum Company, Tiger-Vac International Inc., Vac-U-Max, Goodway Technologies, RGS Vacuum Systems (RGS Impianti), Dustcontrol, G-Winner Ltd., Pullman-Ermator AB, Waidr Vacuum Cleaner (Shanghai) Co., Ltd, Delfin Pharma Range, Ruwac Battery-Powered Series, Nilfisk Battery-Powered Industrial Line, Tiger-Vac Cleanroom Systems, and Dustless Technologies. Companies in the Industrial Vacuum Cleaner Market are strengthening their competitive position through continuous product innovation, technological upgrades, and expansion of application-specific solutions. Manufacturers are increasingly focusing on energy-efficient and high-capacity systems that meet evolving industrial cleaning requirements. The integration of advanced filtration technologies, including HEPA systems and improved dust containment mechanisms, is becoming a core development area. Many players are also investing in portable and battery-operated designs to enhance operational flexibility. Strategic partnerships with industrial end users are helping companies develop customized solutions tailored to specific operational environments. Expansion of distribution networks and regional manufacturing facilities is further supporting market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.3 Research approach

- 1.4 Data collection methods

- 1.5 Data mining sources

- 1.5.1 Global

- 1.5.2 Regional/Country

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.6.2 Key trends for market estimation

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.7.2 Forecast model

- 1.7.3 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Filtration Technology

- 2.2.4 Power Source

- 2.2.5 System Type

- 2.2.6 End User

- 2.2.7 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising industrialization and manufacturing activities across key end-use sectors

- 3.2.1.2 Strict occupational health & safety (OHS) and environmental regulations

- 3.2.1.3 Growing deployment in food & beverage and pharmaceutical manufacturing

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High initial investment and total cost of ownership for advanced systems

- 3.2.2.2 Availability of low-cost conventional cleaning substitutes

- 3.2.3 Opportunities

- 3.2.3.1 Integration of HEPA filtration and advanced dust containment technologies

- 3.2.3.2 Adoption of IoT-enabled smart monitoring and predictive maintenance features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Regional price variations

- 3.9.4 Impact of raw material costs on pricing

- 3.9.5 Pricing by product type and filtration technology

- 3.10 Trade data analysis (HS code 8508.60) (driven by paid database)

- 3.10.1 Import/export volume and value trends (driven by paid database)

- 3.10.2 Key trade corridors and tariff impact (driven by paid database)

- 3.10.3 Leading exporting countries

- 3.10.4 Leading importing countries

- 3.10.5 Trade policy changes and impact assessment

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Predictive maintenance optimization

- 3.11.4 Autonomous navigation and path planning

- 3.11.5 Smart filtration monitoring and alerts

- 3.11.6 AI-powered demand forecasting for service contractors

- 3.11.7 Risks, limitations and regulatory considerations

- 3.11.8 Investment trends in AI-enabled vacuum systems

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed capacity by region and key producer (driven by primary research)

- 3.12.2 Capacity utilization rates and expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Dry Vacuum Cleaners

- 5.3 Wet Vacuum Cleaners

- 5.4 Wet & Dry Vacuum Cleaners

Chapter 6 Market Estimates & Forecast, By Filtration Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Bag Filtration

- 6.3 Cartridge Filtration

- 6.4 Cyclonic Filtration

- 6.5 HEPA Filtration

- 6.6 Hybrid Filtration Systems

Chapter 7 Market Estimates & Forecast, By Power Source, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Electric

- 7.3 Pneumatic

- 7.4 Battery-Powered

- 7.5 Fuel-Powered

Chapter 8 Market Estimates & Forecast, By System Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Portable

- 8.3 Stationary

Chapter 9 Market Estimates & Forecast, By End User Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food & Beverage

- 9.3 Pharmaceutical

- 9.4 Metal Working

- 9.5 Automotive

- 9.6 Others (construction, manufacturing, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.3 Offline

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 Alfred Karcher SE & Co. KG

- 12.1.2 Nilfisk Group

- 12.1.3 Tennant Company

- 12.1.4 Ruwac Industriesauger GmbH

- 12.1.5 Delfin Industrial Vacuums

- 12.1.6 Nederman Group

- 12.1.7 Depureco Industrial Vacuums Srl

- 12.2 Regional Champions

- 12.2.1 American Vacuum Company

- 12.2.2 Tiger-Vac International Inc.

- 12.2.3 Vac-U-Max

- 12.2.4 Goodway Technologies

- 12.2.5 RGS Vacuum Systems (RGS Impianti)

- 12.2.6 Dustcontrol

- 12.2.7 G-Winner Ltd.

- 12.3 Emerging & Specialized Players

- 12.3.1 Pullman-Ermator AB

- 12.3.2 Waidr Vacuum Cleaner (Shanghai) Co., Ltd

- 12.3.3 Delfin Pharma Range

- 12.3.4 Ruwac Battery-Powered Series

- 12.3.5 Nilfisk Battery-Powered Industrial Line

- 12.3.6 Tiger-Vac Cleanroom Systems

- 12.3.7 Dustless Technologies