|

시장보고서

상품코드

2038678

신선 채소 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Fresh Vegetable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

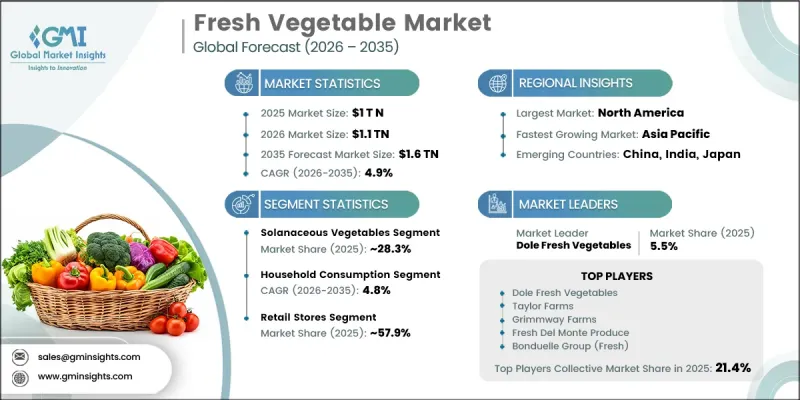

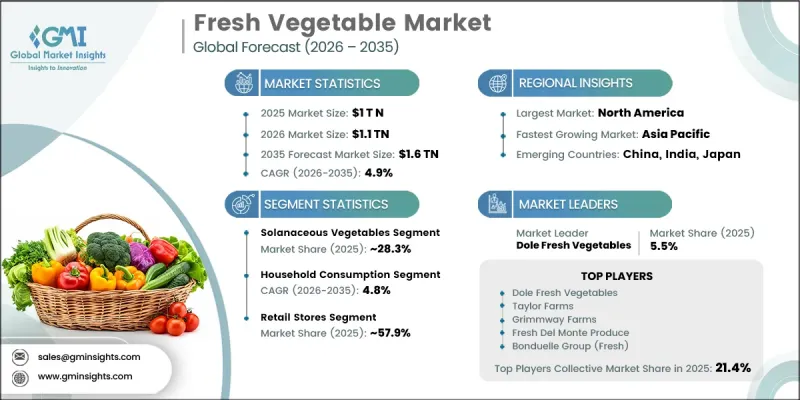

세계의 신선 채소 시장은 2025년에 1조 달러로 평가되었고 CAGR 4.9%로 성장하여 2035년까지 1조 6,000억 달러에 이를 것으로 추정되고 있습니다.

건강한 식품에 대한 소비자의 선호도 증가, 지속가능성에 대한 인식 향상, 농업 기술의 발전으로 시장 확대가 가속화되고 있습니다. 많은 사람들이 영양이 풍부한 식단에 초점을 맞추고 더 신선하고 화학물질이 없는 식품을 찾게 되면서 수요가 증가하고 있습니다. 지속 가능한 농업 관행과 친환경적인 구매 습관이 생산과 유통의 변화를 주도하고 있습니다. 농업 기술 및 저장 솔루션의 기술적 진보를 바탕으로 한 공급망 효율화를 통해 연중 안정적인 공급을 보장하고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 1조달러 |

| 예측 규모 | 1조 6,000억 달러 |

| CAGR | 4.9% |

용도별로 보면, 이 시장에는 가정 소비, 식품 가공, 외식 산업, 기타가 포함됩니다. 소비자들이 일상 식단에서 신선하고 가공도가 낮은 식품을 선호하는 경향이 있기 때문에 가정 소비가 여전히 주류이며, 전체 수요의 60.4%를 차지합니다. 영양학적 이점에 대한 인식 증가와 신선한 농산물을 권장하는 마케팅 캠페인이 결합되어 구매 패턴에 영향을 미치고 있습니다. 식물성 식습관으로의 전환이 진행되고 있는 것도 이러한 성장을 가속하고 있으며, 더 많은 소비자들이 영양가가 높고 가공도가 낮은 식품을 선택하게 되었습니다.

소매점 부문은 57.9%의 점유율을 차지하고 있으며, 2035년까지 연평균 복합 성장률(CAGR) 4.9%를 나타낼 것으로 예측됩니다. 소비자들이 편의성, 투명한 제품 정보, 일관된 품질 기준을 점점 더 중요시함에 따라 유통 채널은 빠르게 진화하고 있습니다. 슈퍼마켓이나 대형마트와 같은 전통적인 소매 형태는 다양한 제품군, 경쟁력 있는 가격, 그리고 한 매장에서 완성되는 종합적인 쇼핑 경험을 제공함으로써 여전히 중심적인 역할을 하고 있습니다. 한편, 온라인 소매업은 특히 COVID-19 이후 디지털 구매 행동으로의 전환과 택배 서비스 및 타겟팅된 디지털 프로모션에 대한 선호도 증가에 힘입어 크게 성장하고 있습니다. 전자상거래 플랫폼은 상세한 상품 정보를 제공하고, 유기농 채소 및 특산품에 대한 접근을 가능하게 함으로써 기업이 더 많은 소비자층에게 다가갈 수 있도록 돕습니다. 이와 함께, 신선하고 현지 생산 농산물과 투명한 농업 관행을 중시하고 지역 농업 경제를 지원하는 건강 지향적인 소비자층 사이에서 파머스 마켓의 인기가 높아지고 있습니다.

2025년 기준 북미 신선 채소 시장은 13.8%의 점유율을 차지했습니다. 이 지역 수요는 지속 가능한 현지 농법으로 생산된 유기농 채소에 대한 선호도 증가에 큰 영향을 받고 있습니다. 미국과 캐나다의 소비자들은 식물성 식품을 포함한 건강한 식습관으로 점점 더 많이 이동하고 있습니다. 슈퍼마켓, 소매점, 온라인 플랫폼 등의 유통망은 제품의 가용성을 확대하는 한편, 표시 및 인증 기준을 통해 투명성을 높이고 있습니다. 또한, 외식업계에서는 영양가와 전체 식품의 품질을 향상시키기 위해 신선한 채소를 점점 더 많이 채택하고 있습니다. 식품 안전, 환경적 지속가능성, 책임감 있는 농업 관행에 대한 인식이 높아지면서 장기적인 시장 성장에 더욱 박차를 가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 채소 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제7장 시장 추산 및 예측 : 유통 채널별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.05.29The Global Fresh Vegetable Market was valued at USD 1 trillion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 1.6 trillion by 2035.

Rising consumer preference for healthier food options, increasing sustainability awareness, and advancements in agricultural technology are fueling market expansion. There is an increasing demand as many people focus on nutrient-rich diets and seek out fresher, chemical-free options. Sustainable farming practices and eco-conscious purchasing habits are driving shifts in production and distribution. Enhanced supply chain efficiency, supported by technological improvements in farming techniques and storage solutions, ensures year-round availability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Trillion |

| Forecast Value | $1.6 Trillion |

| CAGR | 4.9% |

Segmented by application, the market includes household consumption, food processing, food service, and others. Household consumption remains dominant, contributing 60.4% of total demand as consumers prioritize fresh, whole foods in their daily meals. Increased awareness of nutritional benefits, combined with marketing campaigns promoting fresh produce, is influencing purchasing patterns. The ongoing shift toward plant-based eating habits reinforces this growth, as more consumers opt for minimally processed foods with high nutrient content.

The retail stores segment held a 57.9% share and is projected to grow at a CAGR of 4.9% through 2035. Distribution channels are evolving quickly as consumers increasingly prioritize easy access, transparent product information, and consistent quality standards. Conventional retail formats such as supermarkets and hypermarkets continue to play a central role by offering a wide assortment of products, competitive pricing, and a comprehensive shopping experience under one roof. At the same time, online retailing has expanded significantly, supported by the shift toward digital purchasing behavior, especially following the pandemic, along with growing preference for doorstep delivery and targeted digital promotions. E-commerce platforms also enable access to organic and specialty vegetables while providing detailed product insights, allowing companies to reach broader consumer segments. In parallel, farmers markets are gaining popularity among health-conscious consumers who value fresh, locally sourced produce and transparent farming practices, while also supporting regional agricultural economies.

North America Fresh Vegetable Market accounted for 13.8% share in 2025. Demand in the region is strongly influenced by the growing preference for organically produced vegetables sourced through sustainable and local farming practices. Consumers in both the United States and Canada are increasingly shifting toward healthier diets, including plant-based food choices. Distribution networks such as supermarkets, retail outlets, and online platforms are ensuring wider product availability while improving transparency through labeling and certification standards. Additionally, the foodservice sector is increasingly incorporating fresh vegetables to enhance nutritional value and overall food quality. Rising awareness regarding food safety, environmental sustainability, and responsible agricultural practices is further supporting long-term market growth.

Major companies operating in the Global Fresh Vegetable Market include Fresh Del Monte Produce, Taylor Farms, Dole Fresh Vegetables, Bonduelle Group, Grimmway Farms, BrightFarms, Earthbound Farm, Tanimura & Antle, Mann Packing Company, Mastronardi Produce (SUNSET Grown), Church Brothers Farms, Baloian Farms, Ocean Mist Farms, Lipman Family Farms, and SunFed. Key strategies to strengthen growth in the fresh vegetable market include expanding contract farming and direct sourcing partnerships to ensure consistent supply and quality control. Companies are investing in cold chain logistics and advanced storage systems to reduce post-harvest losses and maintain freshness across long distribution routes. Strengthening organic certification and transparent labeling practices is helping build consumer trust and brand loyalty. Market players are also focusing on digital transformation through e-commerce platforms and mobile applications to improve accessibility and customer engagement. Product diversification, including ready-to-eat and pre-cut vegetable offerings, is supporting convenience-driven demand. Additionally, investments in sustainable farming techniques and water-efficient cultivation methods are enhancing long-term productivity while aligning with environmental expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vegetable type

- 2.2.3 End use

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Vegetable Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Leafy Greens

- 5.2.1 Lettuce

- 5.2.2 Spinach

- 5.2.3 Kale

- 5.2.4 Swiss Chard

- 5.2.5 Others

- 5.3 Cruciferous Vegetables

- 5.3.1 Broccoli

- 5.3.2 Cauliflower

- 5.3.3 Cabbage

- 5.3.4 Brussels Sprouts

- 5.3.5 Others

- 5.4 Root Vegetables

- 5.4.1 Carrots

- 5.4.2 Potatoes

- 5.4.3 Beets

- 5.4.4 Radishes

- 5.4.5 Others

- 5.5 Allium Vegetables

- 5.5.1 Onions

- 5.5.2 Garlic

- 5.5.3 Leeks

- 5.5.4 Shallots

- 5.5.5 Others

- 5.6 Solanaceous Vegetables

- 5.6.1 Tomatoes

- 5.6.2 Peppers

- 5.6.3 Eggplants

- 5.6.4 Others

- 5.7 Legumes

- 5.7.1 Peas

- 5.7.2 Beans

- 5.7.3 Lentils

- 5.7.4 Others

- 5.8 Cucurbitaceous Vegetables

- 5.8.1 Cucumbers

- 5.8.2 Zucchinis

- 5.8.3 Pumpkins

- 5.8.4 Melons

- 5.8.5 Others

- 5.9 Other

- 5.9.1 Corn

- 5.9.2 Asparagus

- 5.9.3 Artichokes

- 5.9.4 Others

Chapter 6 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Household consumption

- 6.3 Food processing

- 6.4 Foodservice

- 6.5 Other end-uses

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Retail stores

- 7.3 Online retailing

- 7.4 Farmers' markets

- 7.5 Specialty stores

- 7.6 Foodservice providers

- 7.7 Wholesale markets

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Baloian Farms

- 9.2 Bonduelle Group

- 9.3 BrightFarms

- 9.4 Church Brothers Farms

- 9.5 Dole Fresh Vegetables

- 9.6 Earthbound Farm

- 9.7 Fresh Del Monte Produce

- 9.8 Grimmway Farms

- 9.9 Lipman Family Farms

- 9.10 Mann Packing Company

- 9.11 Mastronardi Produce (SUNSET Grown)

- 9.12 Ocean Mist Farms

- 9.13 SunFed

- 9.14 Tanimura & Antle

- 9.15 Taylor Farms